Nexelia Academy · Official Revision Notes

Complete A-Level revision notes · 37 chapters

This chapter introduces the core concepts of business activity, including the purpose of businesses, the factors of production, and the crucial concept of adding value. It also explores the economic problem of scarcity and opportunity cost, and highlights the vital roles of entrepreneurs and intrapreneurs in driving economic development.

Business — A business is an organisation that uses resources to meet the needs of customers by providing a product or service that they demand.

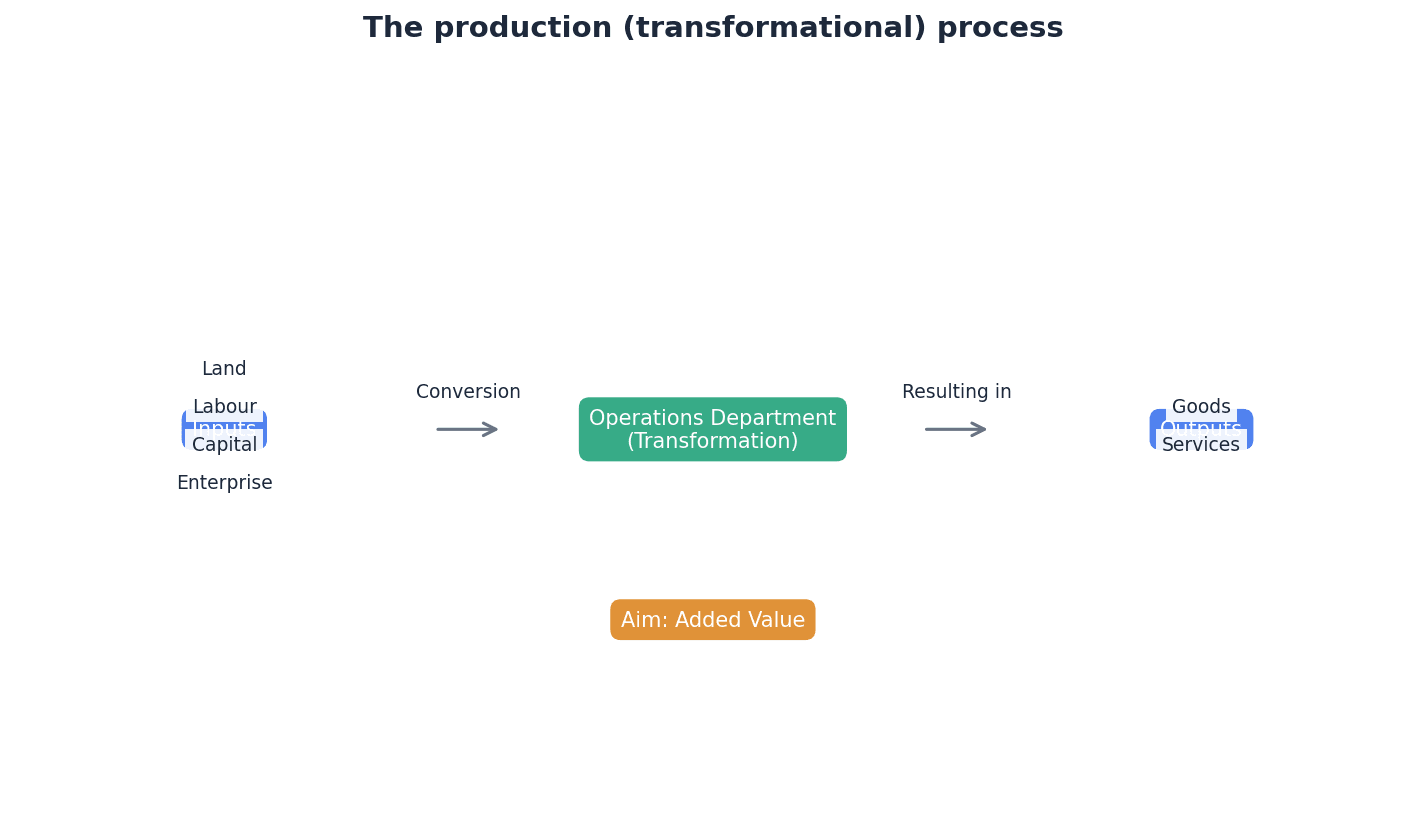

Businesses are fundamental to economic activity, transforming scarce resources into goods and services that satisfy consumer needs. Their primary aim is often to add value and make a profit, contributing to a higher standard of living. Think of a baker: they take flour, water, and yeast (resources) and turn them into bread (a product) that customers want, adding value through their skill and effort.

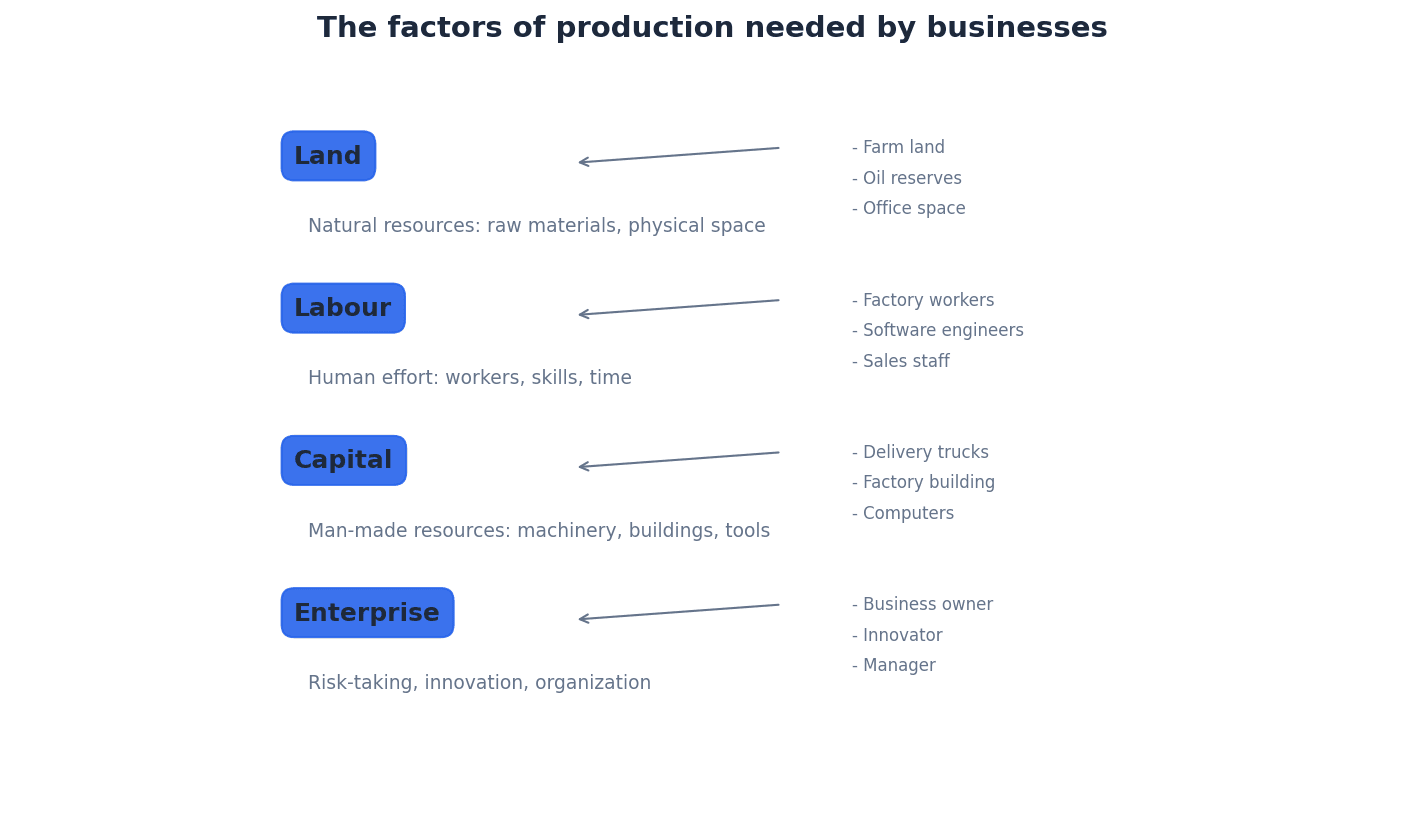

Factors of production — Factors of production are the resources needed by businesses to be able to operate and produce goods or services.

These four categories – land, labour, capital, and enterprise – are the fundamental building blocks for any economic activity. Their availability and efficient combination determine a business's capacity to produce. Imagine building a house: the land is where it stands, the builders are the labour, the tools and machinery are the capital, and the architect/project manager is the enterprise bringing it all together.

Be prepared to define and give examples for each of the four factors of production, as this is a common definitional question.

Land — Land is a general term that includes not only land itself but all the renewable and non-renewable resources of nature, such as coal, crude oil and timber.

This factor encompasses all natural resources, whether they are directly used as raw materials or provide the physical space for operations. Its scarcity is a core aspect of the economic problem. For a farmer, the land is the soil for crops, the water for irrigation, and even the sunlight that helps plants grow.

Students often think 'land' only refers to real estate, but actually it includes all natural resources, both above and below the surface.

Labour — Labour refers to the manual and skilled labour that make up the workforce of the business.

This factor represents the human effort, both physical and mental, applied in the production process. The quality and quantity of labour significantly impact a business's productivity and output. In a restaurant, the chefs, waiters, and cleaners all represent labour, each contributing their skills to the service.

Capital — Capital is not just the finance needed to set up a business and pay for its continuing operations, but also all the manufactured resources used in production, including capital goods such as computers, machines, factories, offices and vehicles.

Capital is crucial for enabling production, providing the tools and infrastructure necessary for businesses to operate efficiently. It represents accumulated wealth used to create more wealth. For a taxi company, the cars are capital goods, and the money used to buy them and pay for fuel is finance capital.

Students often think 'capital' only means money, but actually it also includes manufactured resources like machines and factories used in production.

Distinguish clearly between financial capital (money) and physical capital (capital goods) when discussing this factor of production.

Enterprise — Enterprise is the initiative and coordination provided by risk-taking individuals called entrepreneurs, who combine the other factors of production into a unit capable of producing goods and services.

Enterprise is the driving force behind business creation and innovation, involving the vision, risk-taking, and organisational skills needed to bring a business idea to fruition. It provides the managing, decision-making, and coordinating roles. The conductor of an orchestra is like enterprise, bringing together the musicians (labour), instruments (capital), and sheet music (land/resources) to create a performance.

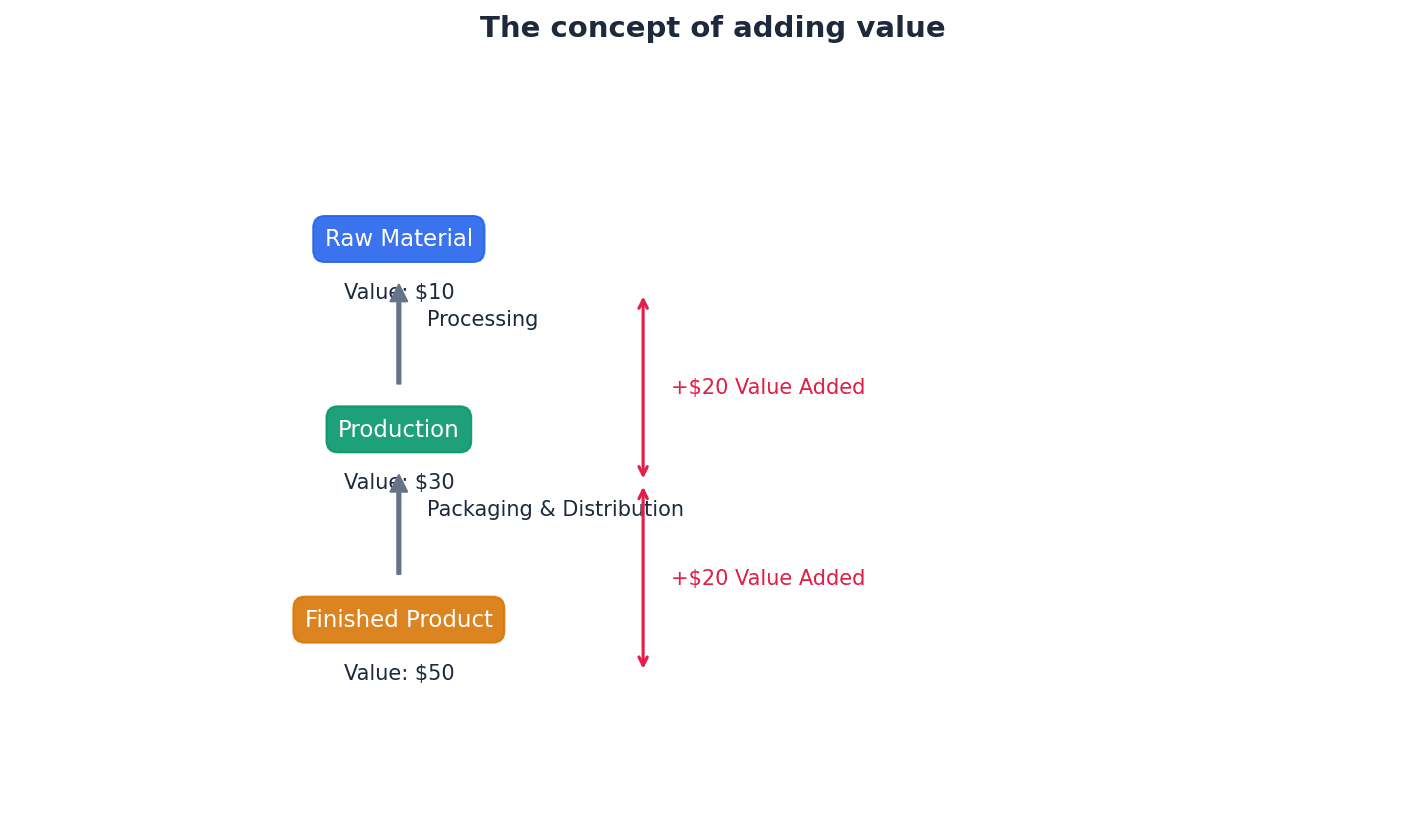

Added value — Added value is the difference between the selling price of the products sold by a business and the cost of the materials that it bought in.

Adding value is essential for a business's survival and profitability, as it allows the business to cover other costs (like labour and rent) and provide a return to investors. It reflects the perceived worth customers place on the transformed product or service. A coffee shop buys raw coffee beans for a low price, but after roasting, grinding, brewing, and serving it in a pleasant environment, the selling price of a cup of coffee is much higher, representing the added value.

Students often think added value is the same as profit, but actually profit is what remains after all costs, including labour and overheads, have been deducted from added value.

When asked to explain 'adding value', clearly state it's the difference between selling price and bought-in material costs, and explain its importance for covering other expenses and generating profit.

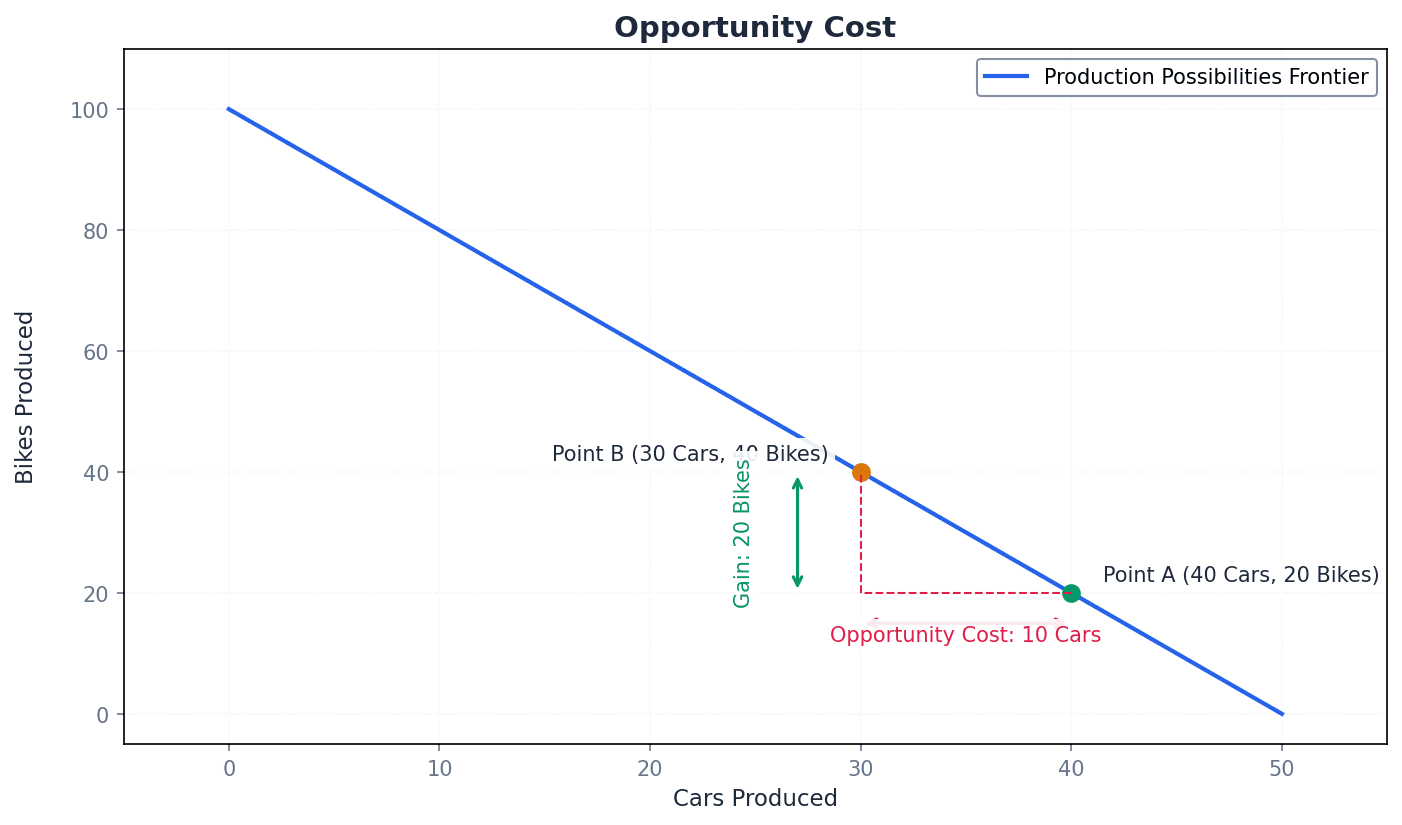

Economic problem — The economic problem is the situation where there are insufficient goods to satisfy all of our needs and wants at any one time.

This fundamental problem arises from the scarcity of resources relative to unlimited human wants. It forces individuals, businesses, and governments to make choices about how to allocate resources. Imagine having a limited budget for groceries but wanting to buy everything in the supermarket; you can't, so you have to choose what's most important.

Ensure your explanation of the economic problem links scarcity of resources to the inability to satisfy all needs and wants, leading to the necessity of choice.

Opportunity cost — Opportunity cost is the next most desired product which is given up when deciding to purchase or obtain one item over others.

This concept highlights the trade-offs inherent in all economic decisions. Every choice made means foregoing the benefits of the next best alternative, which is the true cost of that decision. If you choose to spend your Saturday studying for an exam, the opportunity cost might be going to a concert with friends, which was your next best alternative.

Students often think opportunity cost is all the things given up, but actually it is only the single next best alternative that is foregone.

When explaining opportunity cost, clearly identify the choice made and the single best alternative that was sacrificed as a direct result of that choice.

Entrepreneur — An entrepreneur is a risk-taking individual who combines the other factors of production into a unit capable of producing goods and services, providing the managing, decision-making and coordinating roles.

Entrepreneurs are central to economic development, identifying market gaps, innovating, and taking personal and financial risks to create new businesses. Their qualities include innovation, commitment, multi-skilling, leadership, self-confidence, and risk-taking. A chef who decides to open their own restaurant, investing their savings, hiring staff, designing the menu, and managing daily operations, is an entrepreneur.

When analysing entrepreneurs, focus on their personal qualities (e.g., risk-taking, innovation) and their role in combining factors of production and managing the business.

Entrepreneurs and their enterprise are vital for a country's economic development. They drive innovation, create new businesses, generate employment opportunities, and contribute to tax revenues. This leads to increased competition, a wider variety of goods and services, and ultimately a higher standard of living for the population. However, entrepreneurs often face barriers such as obtaining sufficient capital, finding good locations, intense competition, and managing business risk and uncertainty.

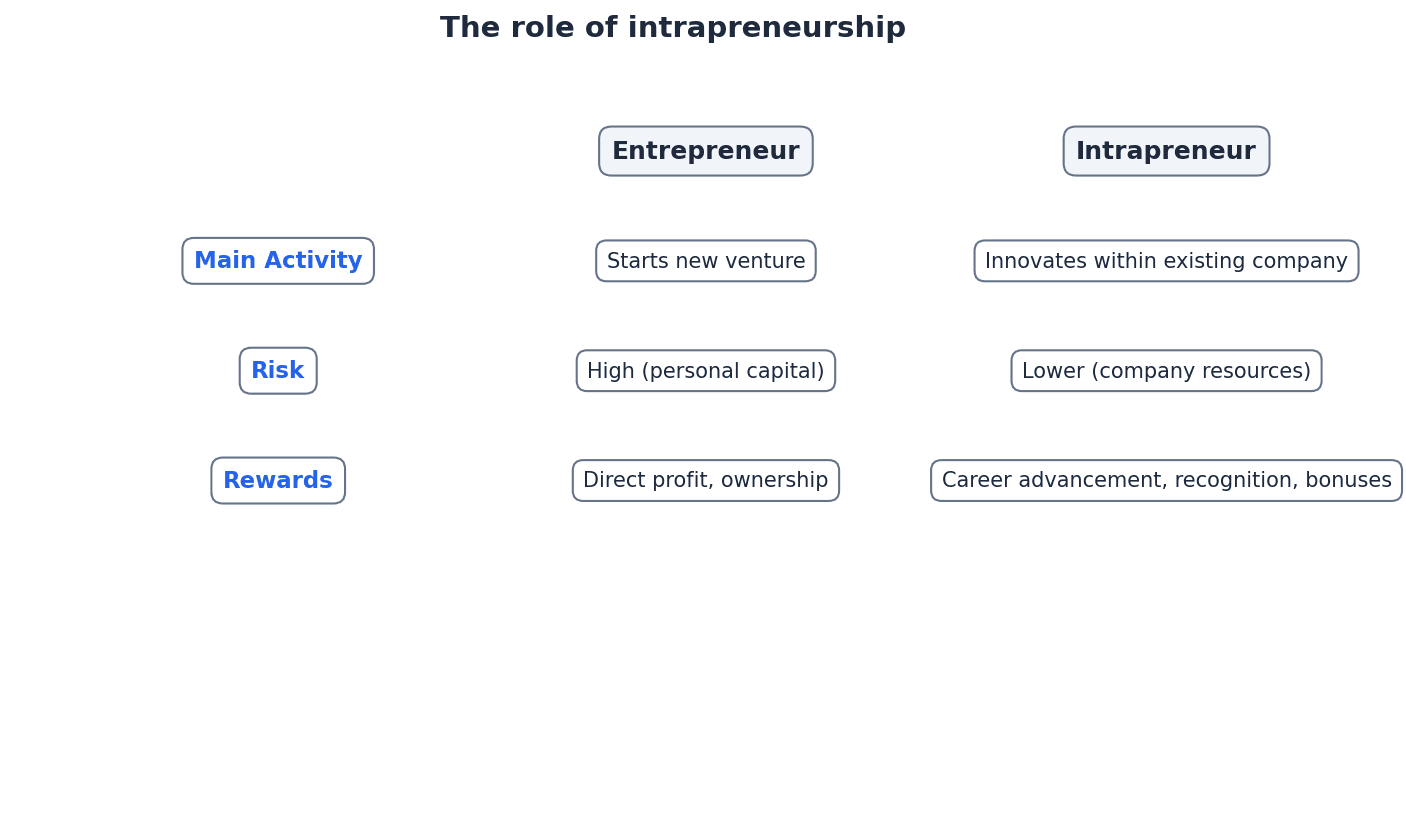

Intrapreneur — An intrapreneur is a person who has the same qualities as entrepreneurs and is encouraged to demonstrate the same skills as entrepreneurs within an existing business.

Intrapreneurs drive innovation and change from within established organisations, helping businesses adapt to dynamic environments and retain creative talent. They take risks on behalf of the company, not personally. An employee at a large tech company who develops a new product feature or service idea, champions it, and brings it to market using company resources, is an intrapreneur.

Distinguish intrapreneurs from entrepreneurs by highlighting that intrapreneurs operate within an existing business, with the business taking the risk and receiving the rewards.

Business plan — A business plan is a detailed document outlining a new business's strategies, operations, marketing, management team, and financial forecasts.

It serves as a roadmap for the business and a crucial tool for attracting finance from investors and lenders. While beneficial for planning, it can also create a false sense of certainty or lead to inflexibility if not adapted to a dynamic environment. Think of a business plan as a detailed blueprint for building a house; it shows what you intend to build, how you'll build it, who will help, and how much it will cost, to convince a bank to lend you money.

Students often think a business plan guarantees success, but actually it's a forecast and a guide, and external factors can still lead to failure if the plan isn't flexible.

When evaluating business plans, discuss both their benefits (e.g., securing finance, clear direction) and limitations (e.g., inflexibility, based on forecasts).

Always evaluate. When asked about business plans, discuss both their benefits (e.g., securing finance) and limitations (e.g., can be rigid).

Advantages & Disadvantages

Business Plans

Entrepreneurship for Economic Development

Evaluation Starters

Essay Structure Guide

Introduction

Start by defining key terms relevant to the question (e.g., entrepreneur, economic development, business plan). Briefly outline the main arguments you will present.

Conclusion

Summarise your main arguments and provide a final, reasoned judgment that directly answers the question. Avoid introducing new information. Emphasise the overall significance of enterprise and planning while acknowledging their complexities.

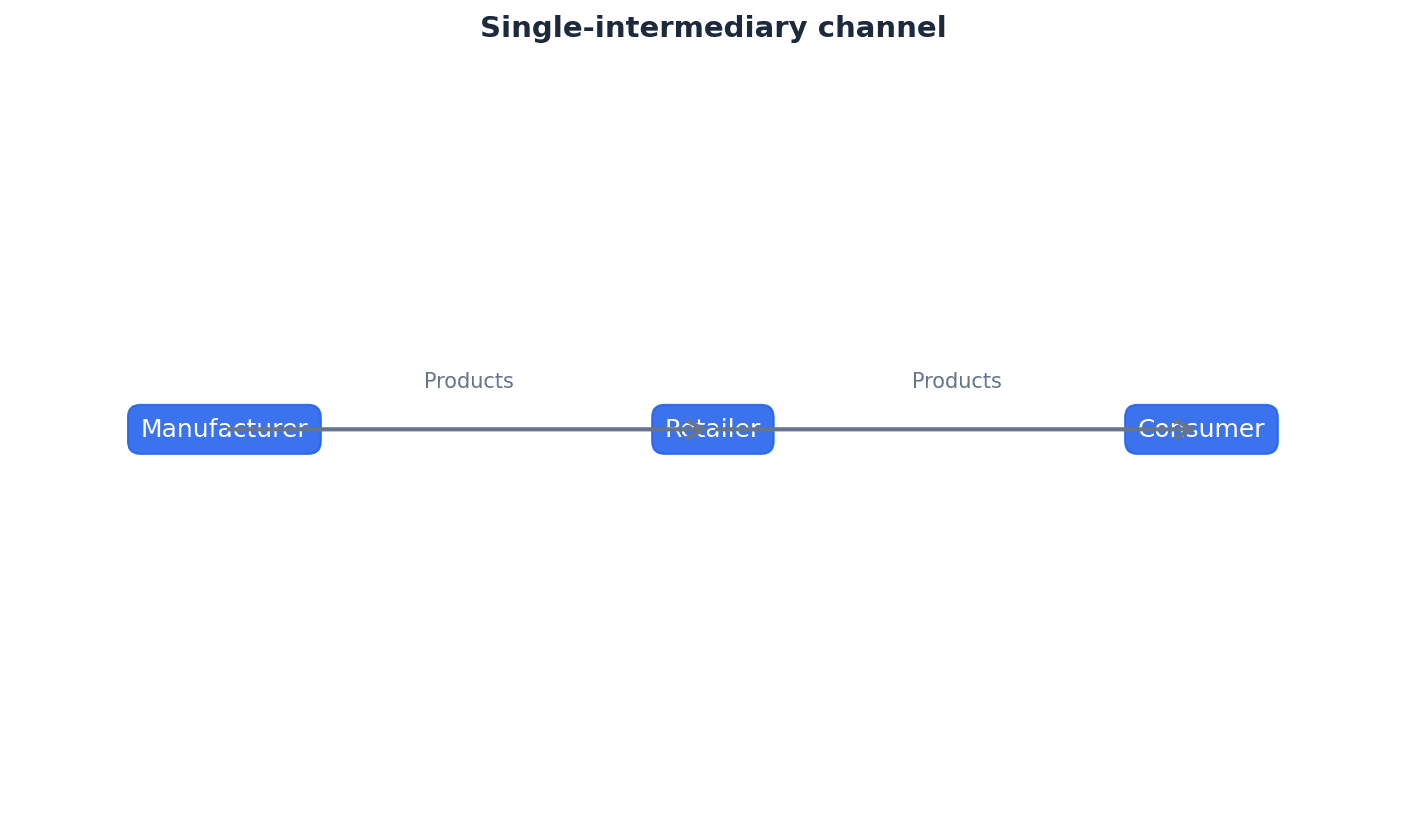

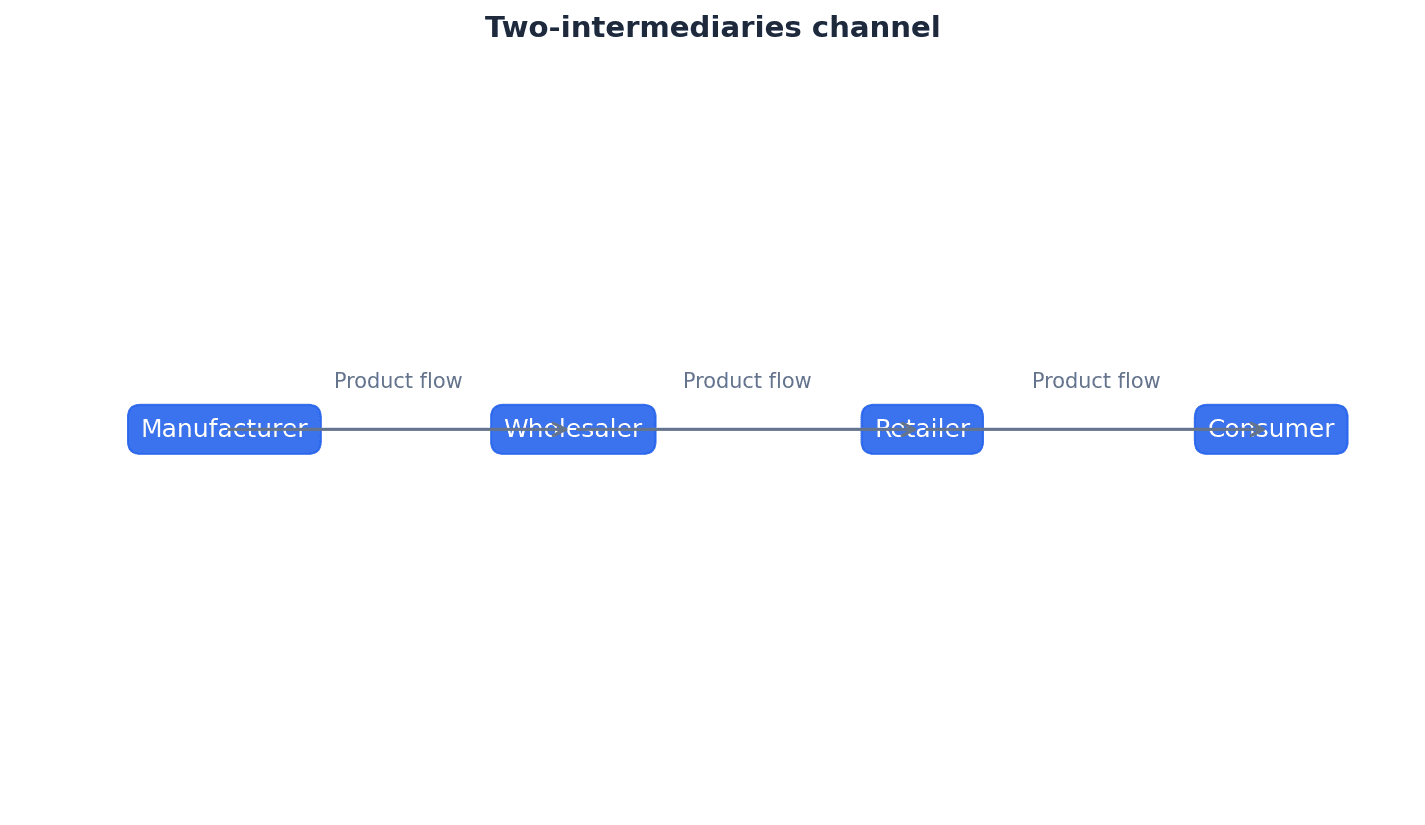

This chapter explores how business activities are categorised into economic sectors and the shifts between them, such as industrialisation and deindustrialisation. It then differentiates between private and public sector organisations, detailing various private sector legal structures like sole traders, partnerships, and companies, evaluating their advantages and disadvantages.

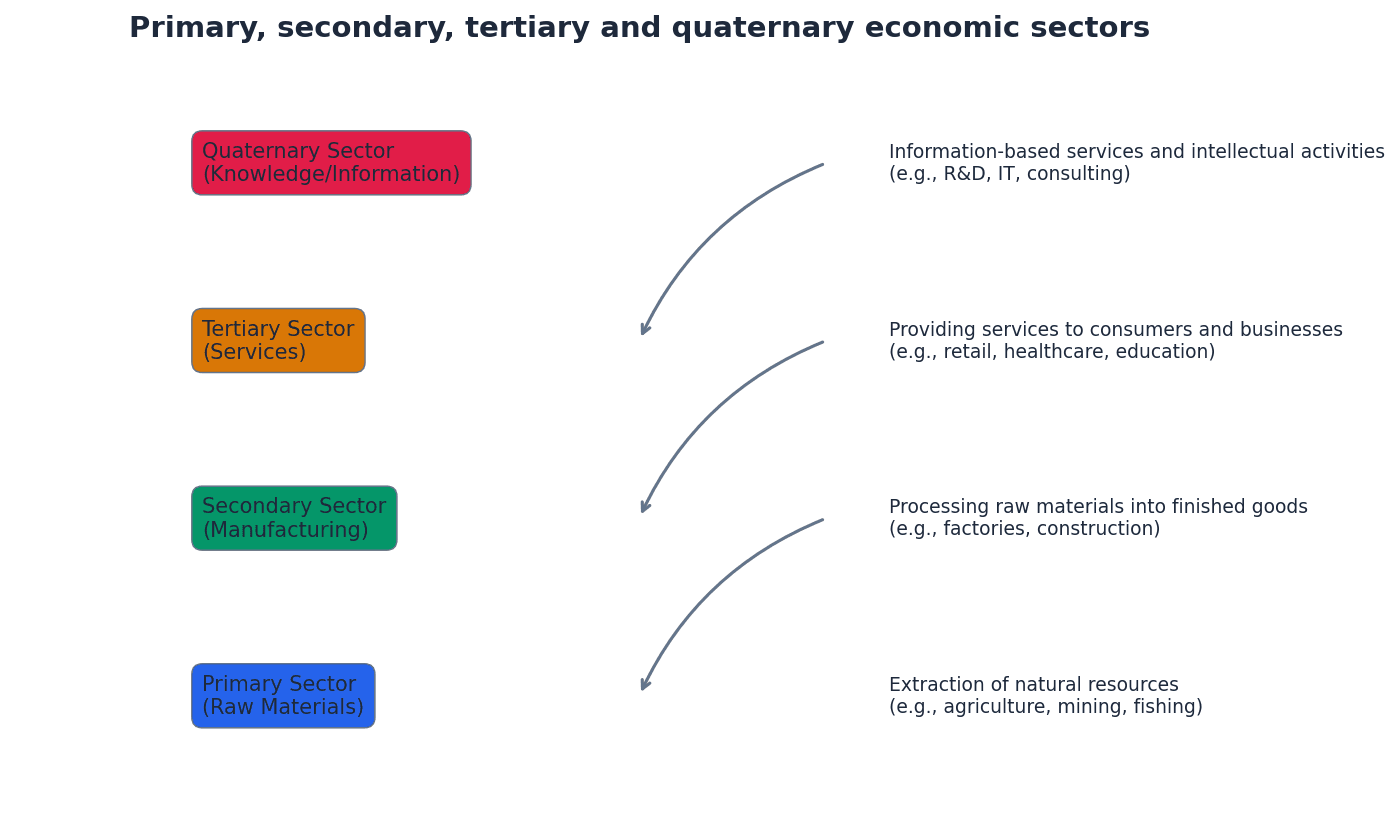

Industrialisation — The growing importance of secondary sector manufacturing industries in developing countries.

This process involves a shift in economic activity from primary to secondary sectors, leading to increased national output and job creation. For example, a country that primarily farms crops (primary sector) starting to build factories to turn those crops into processed foods (secondary sector) is undergoing industrialisation. It often results in higher standards of living but can also cause social problems due to rural-to-urban migration.

Students often think industrialisation only refers to historical events, but actually it is an ongoing process in many developing economies today.

Deindustrialisation — The decline in the importance of secondary sector activity and an increase in the tertiary sector in developed economies.

This occurs as economies mature, with rising incomes leading to increased demand for services over goods, and manufacturing facing global competition. For instance, a country that used to make a lot of cars and steel (secondary sector) now focusing more on tourism, banking, and technology services (tertiary sector) is experiencing deindustrialisation. It results in job losses in manufacturing but creates opportunities in service industries.

Students often think deindustrialisation means a country stops manufacturing entirely, but actually it means the manufacturing sector's relative importance to the economy declines.

When analysing industrialisation, ensure you discuss both benefits (e.g., GDP increase, job creation) and problems (e.g., urbanisation issues, import costs) to achieve higher marks.

Business activity is classified into primary (extraction of raw materials), secondary (manufacturing), tertiary (services), and quaternary (knowledge-based) economic sectors. The relative importance of these sectors changes over time, particularly as economies develop. Industrialisation signifies a shift towards the secondary sector in developing nations, while deindustrialisation marks a decline in the secondary sector and a rise in the tertiary sector in developed economies. These shifts have significant consequences for national output, employment, and living standards.

Public-sector enterprises — Organisations that are government-owned or state-run, providing important goods and services.

These enterprises often operate with social objectives rather than solely profit motives, providing essential services like health, education, or strategic industries. A national healthcare system or a state-owned railway company are examples, aiming to serve the public rather than maximise shareholder profit. They are financed mainly by the government and can be prone to inefficiency or political interference.

Public goods — Goods and services that cannot be charged for, making it impossible for a private-sector business to make a profit from producing them.

These goods are non-excludable and non-rivalrous, meaning individuals cannot be prevented from using them, and one person's use does not diminish another's. Street lighting is a classic example: once installed, everyone benefits, and you can't charge individuals for their specific use, so the government provides it. They are typically provided by the public sector and funded through taxes.

Students often think public-sector enterprises are the same as public limited companies, but actually public-sector enterprises are government-owned, while public limited companies are private sector businesses whose shares are traded publicly.

Distinguish clearly between public-sector enterprises and public limited companies in your answers, as confusing them is a common error. Focus on ownership and primary objectives.

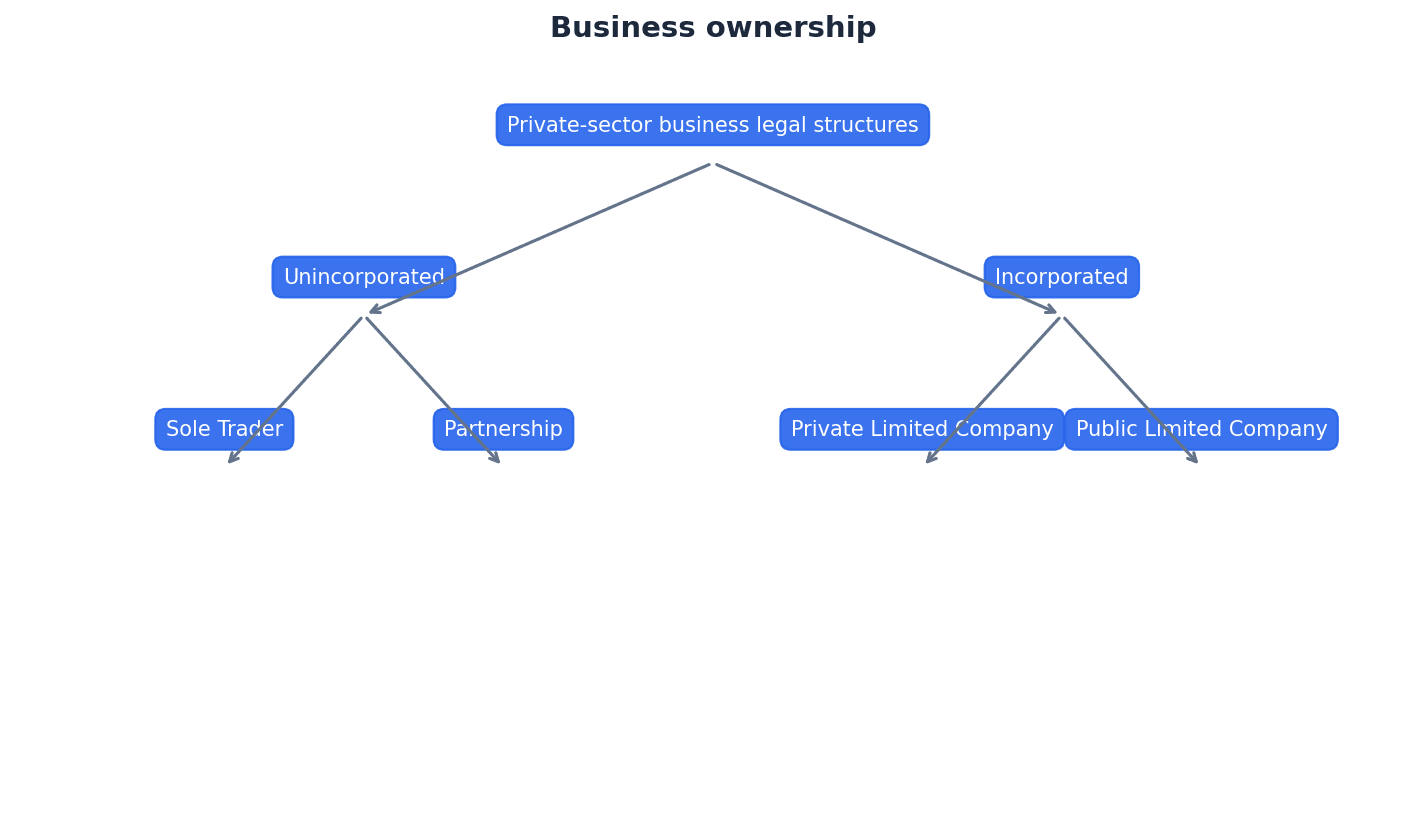

The economy is broadly divided into the private sector and the public sector. The private sector comprises businesses owned and controlled by individuals or groups, aiming to generate profit. In contrast, the public sector consists of organisations that are government-owned or state-run, known as public-sector enterprises. These entities typically provide essential goods and services, often with social objectives rather than purely profit motives, and are funded primarily by the government.

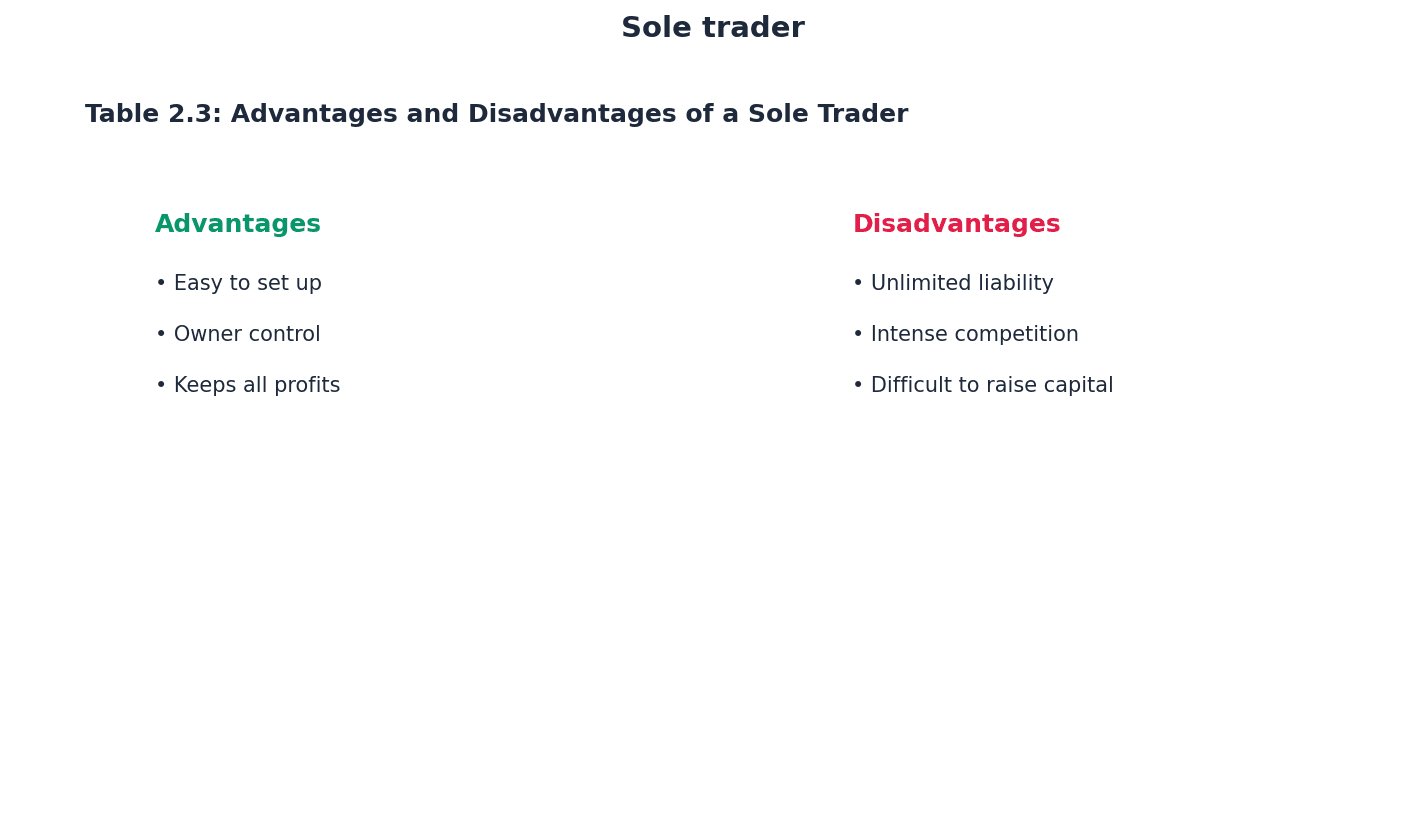

Sole trader — A business organisation with a single owner, who may employ others but retains complete control.

This is the most common form of business ownership, easy to set up, and the owner keeps all profits. A freelance graphic designer working from home, managing all aspects of their business and keeping all profits, is a sole trader. However, the owner faces unlimited liability, making personal assets vulnerable to business debts, and often struggles to raise additional capital for expansion.

Students often think a sole trader cannot employ anyone, but actually they can employ others; the key is that there is only one owner.

Unlimited liability — A legal status where the owner’s personal possessions and property can be taken to pay off the debts of the business, should it fail.

This applies to sole traders and most partnerships, meaning there is no legal distinction between the owner's personal assets and the business's assets. If a business goes bankrupt and has unlimited liability, it's like the business's debts are also the owner's personal debts, and creditors can claim their house or car. It increases the financial risk for the owner and can deter entrepreneurship.

When evaluating sole traders, always discuss unlimited liability as a significant drawback and its implications for the owner's personal finances.

Partnerships — Businesses formed by two or more people to overcome some drawbacks of being a sole trader, often with a formal Deed of Partnership.

Partners share decision-making, inject additional capital, and share business losses. Two lawyers deciding to open a law firm together, sharing clients, responsibilities, and profits, would typically form a partnership. While offering greater privacy than companies, most partners still face unlimited liability, and the partnership lacks continuity if a partner dies.

Students often think all partnerships have limited liability, but actually most partnerships have unlimited liability for all partners, unless it's a specific 'limited partnership' type.

Highlight the shared decision-making and additional capital as advantages of partnerships, but always balance this with the significant disadvantage of unlimited liability for partners.

Limited liability — A legal status where shareholders are only liable for the amount they have invested in the company, protecting their personal assets.

This is a key feature of companies, encouraging investment as individuals are prepared to provide finance without risking their entire personal wealth. If you buy shares in a company with limited liability, the most you can lose is the money you paid for those shares, even if the company goes bankrupt. It transfers the risk of business failure from investors to creditors.

Emphasise that limited liability is a major reason why companies can raise substantial capital, as it reduces the risk for investors.

Shareholders — Part-owners of a company who buy small units of ownership called shares.

Shareholders provide finance to the company and benefit from limited liability. If a company is like a pie, shareholders are people who buy slices of that pie, becoming part-owners. They can influence the company through voting rights, especially those with large blocks of shares who may become directors.

Legal personality — A company is recognised in law as having a legal identity separate from that of its owners.

This means the company itself can enter into contracts, own assets, sue, and be sued, rather than the individual owners. Think of a company as having its own 'birth certificate' and 'identity' in the eyes of the law, separate from the people who own or run it. It provides a layer of protection for owners and allows the business to operate as a distinct entity.

Continuity — In a company, the death of an owner or director does not lead to its break-up or dissolution.

Ownership continues through the inheritance or transfer of shares, ensuring the business can operate indefinitely regardless of changes in personnel. A company is like a river that keeps flowing even if some water molecules (owners) leave or new ones join; the river itself continues. This provides stability and long-term planning capability.

Limited companies offer significant advantages over sole traders and partnerships, primarily limited liability for their owners (shareholders). They also possess a separate legal personality, meaning the company is a distinct legal entity from its owners, and continuity, ensuring the business's existence is not tied to the lifespan of its owners. These features make them attractive for growth and investment, though they involve more legal formalities.

Private limited company — A small firm where owner(s) create a company with limited liability, and shares are sold to family, friends, and employees, not the general public.

This structure offers limited liability, legal personality, and continuity, while often allowing original owners to retain control. It's like a family business that has grown and wants the protection of limited liability, but still wants to keep ownership within a close circle. However, there are legal formalities, and raising capital from the general public is not possible.

Students often think 'private' in private limited company means no one knows about the company, but actually their end-of-year accounts must be sent to a government office and are publicly available.

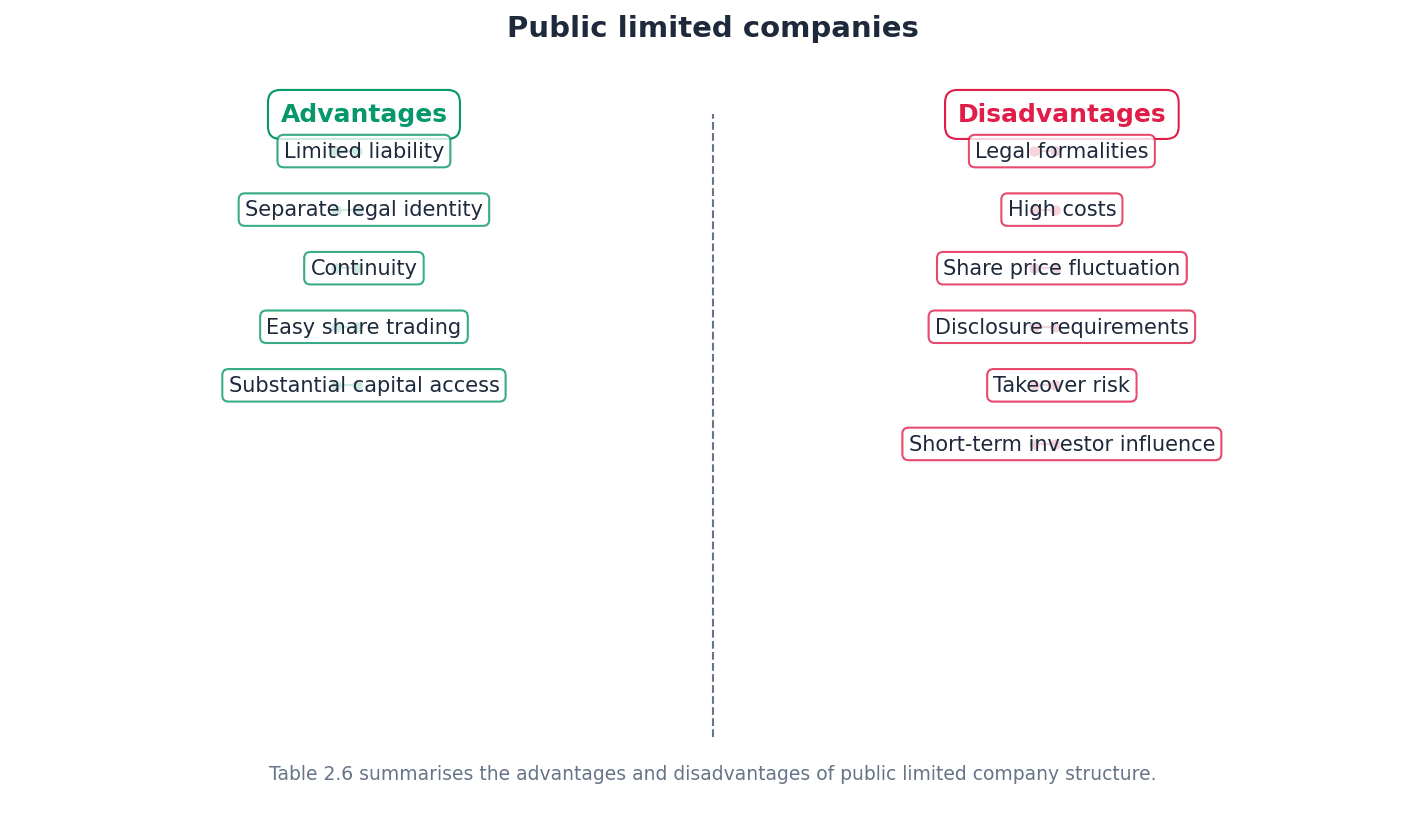

Public limited company (plc) — A legal organisation, usually for very large businesses, that has access to substantial funds for expansion by advertising and selling shares to the general public on a stock exchange.

Plcs benefit from all private company advantages, plus the ability to raise vast capital and allow easy share trading. Think of a very large company like Apple or Coca-Cola; their shares are bought and sold by millions of people on the stock market, allowing them to raise huge amounts of money. However, they face extensive legal formalities, high costs, public scrutiny, and a separation of ownership and control that can lead to conflicts.

Students often think public limited companies are in the public sector, but actually they are private sector businesses; 'public' refers to their ability to sell shares to the general public.

Initial public offering (IPO) — The first sale of shares by a private company to the general public, converting it into a public limited company.

An IPO allows a company to raise significant capital from a wide range of investors. It's like a private club opening its doors for the first time to anyone who wants to join, by buying a membership (shares). It also provides liquidity for existing shareholders, enabling them to sell their shares easily.

When explaining IPOs, link it directly to the conversion of a private limited company to a public limited company and the primary purpose of raising substantial capital.

Cooperatives — A form of business organisation where all members contribute to running the business, share workload, responsibilities, decision-making, and profits equally.

Cooperatives can be producer/worker or consumer/retail focused. Imagine a group of farmers who pool their resources to buy seeds and equipment together, and then collectively sell their produce to get better prices; this is an agricultural cooperative. They benefit from bulk buying and shared motivation but can suffer from poor management skills, capital shortages, and slow decision-making due to member consultation.

Franchise — A legal contract allowing a franchisee to use the name, logo, and marketing methods of a franchiser.

The franchisee operates a business under the established brand of the franchiser, benefiting from brand recognition, advice, and national advertising, which reduces the risk of failure. Buying a McDonald's franchise means you get to open a McDonald's restaurant, use their famous name and recipes, and get their support, but you have to follow their rules and pay them a fee. In return, the franchisee pays an initial fee and a share of profits/revenue, and must adhere to strict rules.

Students often think a franchise is a type of legal structure, but actually it's a business agreement; the franchisee still chooses a legal structure (e.g., sole trader, private limited company) for their own operation.

Joint venture — When two or more businesses work closely together on a project, sharing costs, risks, and potentially different strengths and experiences.

Joint ventures allow companies to combine resources for new ventures, exploit new markets, and reduce individual risk. Two different construction companies partnering to build a very large bridge, combining their expertise and sharing the massive costs and risks, is a joint venture. However, they can face challenges due to differing management styles, blame for errors, and the risk of one partner's failure jeopardising the whole project.

Social enterprises — Businesses that aim to make profit in socially responsible ways, using much of any profit to benefit society.

Social enterprises directly produce goods or provide services with social aims, using ethical methods. A coffee shop that uses its profits to fund education programs for disadvantaged youth, rather than just paying dividends to shareholders, is a social enterprise. Unlike charities, they rely on making a profit to survive and do not depend on donations, competing with other businesses in the market.

When discussing social enterprises, highlight the dual objective of making a profit AND achieving social aims, and how this differentiates them from purely profit-focused businesses and charities.

When asked to recommend a change in ownership (e.g., sole trader to Ltd), always discuss the pros and cons of BOTH structures before giving a justified conclusion.

When comparing structures, focus on key differences: liability (limited/unlimited), sources of finance, control, and legal formalities.

Advantages & Disadvantages

Sole Trader

Partnerships

Evaluation Starters

Essay Structure Guide

Introduction

Start by defining the key terms in the question (e.g., sole trader, private limited company, industrialisation). Briefly outline the scope of your essay, stating what aspects of business structure or sectoral change you will discuss.

Conclusion

Summarise your main arguments without introducing new information. Provide a justified conclusion that directly answers the question, weighing the pros and cons discussed and making a clear recommendation or judgment based on your evaluation.

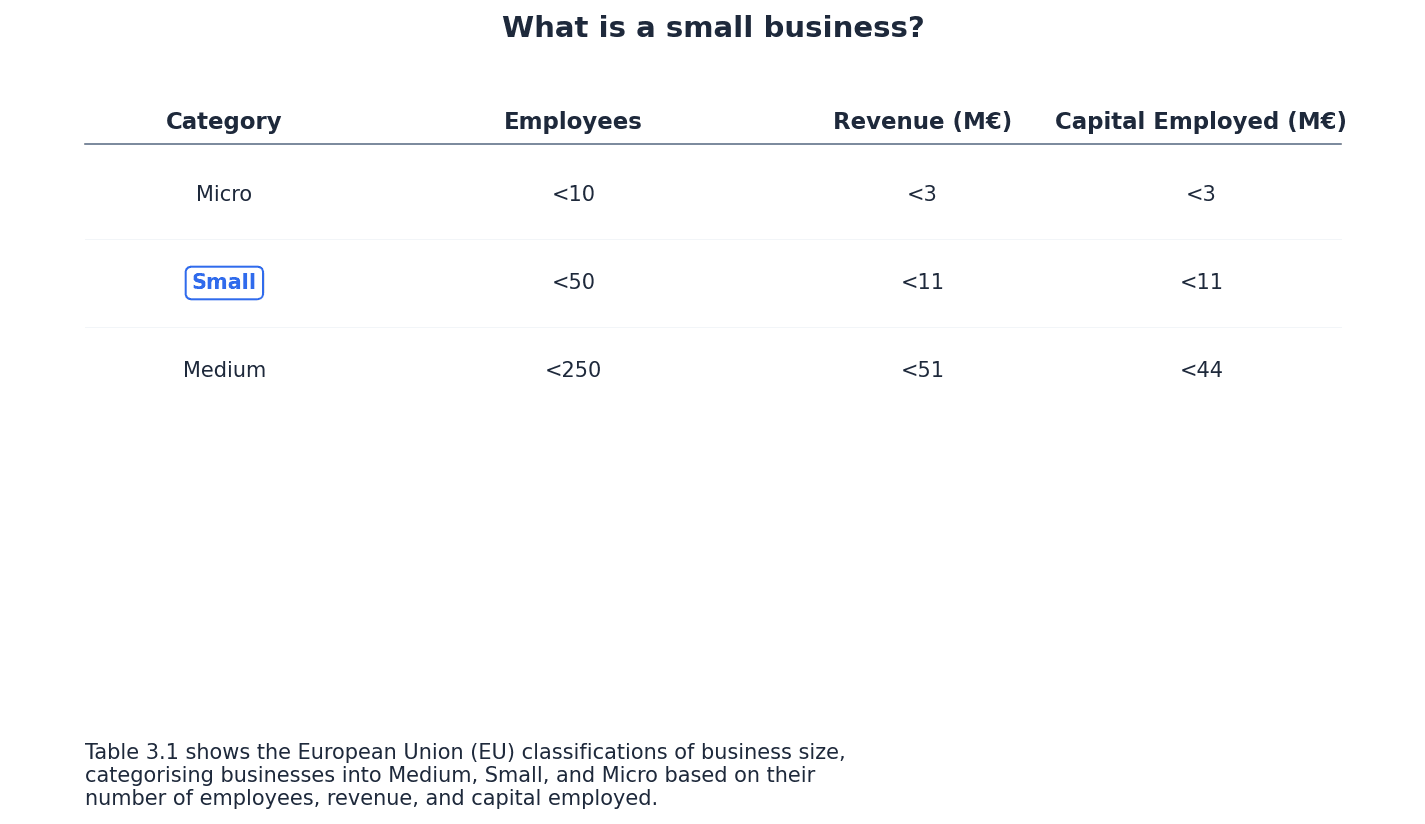

This chapter explores various methods for measuring business size, including employees, revenue, and market share, and discusses their respective strengths and limitations. It also examines the crucial role of small and family businesses within economies and industries, alongside their unique advantages and disadvantages. Finally, the chapter differentiates between organic and external growth strategies, detailing various forms of integration and evaluating their impact on stakeholders, while also considering reasons for the failure of mergers and takeovers.

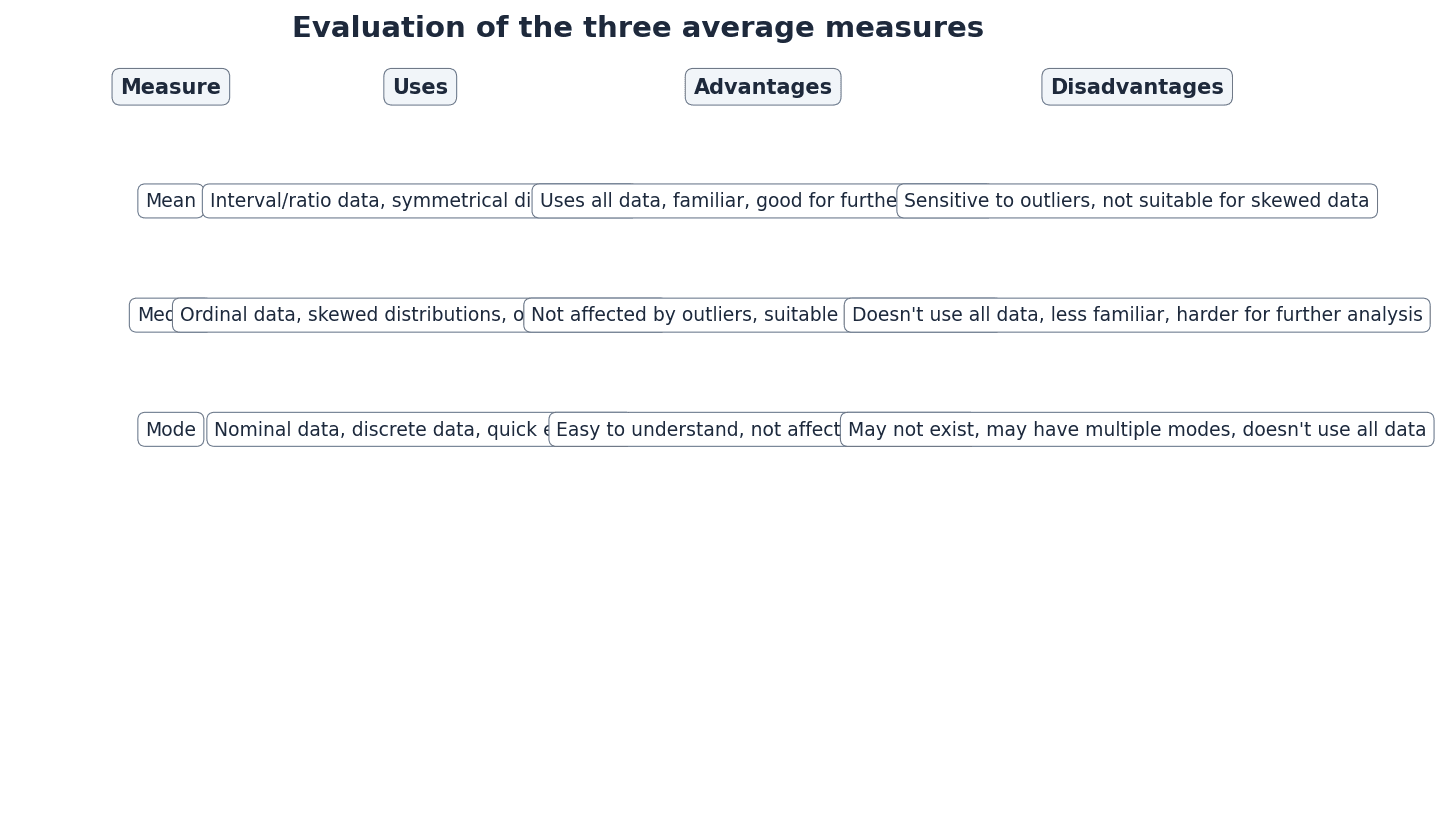

Revenue — Revenue (or sales turnover) is the total value of sales made by a business over a given period.

Revenue represents the total money a business collects from selling its goods or services, similar to the total cash a lemonade stand takes in before deducting costs. It is often used to compare business size, especially within the same industry, but can be misleading across different sectors due to varying production values.

Students often think revenue is the same as profit, but actually revenue is the total income from sales before any costs are deducted, while profit is what remains after all costs are paid. Profit assesses business performance, not size.

When asked to compare business size using revenue, ensure you state that it is more effective for businesses in the same industry. Do not confuse it with profit.

Capital employed — Capital employed is the total value of long-term investment in a business.

This measure reflects the value of assets a business uses to generate revenue, such as machinery and buildings. For example, an optician requires expensive diagnostic machines, leading to higher capital employed than a hairdresser, even with the same number of employees. While larger businesses generally require more capital, comparisons between different industries can be misleading due to varying capital intensity.

Students often think capital employed only refers to money, but actually it includes all long-term assets like machinery, buildings, and equipment, not just cash.

When using capital employed as a measure, acknowledge its limitations, especially when comparing businesses in different sectors, as capital intensity varies greatly.

Market capitalisation — Market capitalisation is the total value of a company's issued shares.

This is calculated by multiplying the current share price by the total number of shares issued, representing the total 'price tag' of a company on the stock market. For instance, a company with 100 shares at 500. This measure is only applicable to public limited companies and can fluctuate daily with share prices, making it less stable for long-term comparisons.

Students often think market capitalisation reflects the company's internal value, but actually it's a market-driven valuation that can be influenced by investor sentiment and external factors, not just the company's assets or profits.

Remember that market capitalisation is only for public limited companies and is highly volatile. Explain how changes in share price can significantly alter this measure without affecting other aspects of the business.

Market Capitalisation

Used only for public limited companies; value fluctuates daily with share prices.

Market share — Market share is the proportion of total market sales held by one business.

This is a relative measure indicating a firm's dominance within its industry. For example, if your pizza shop sells 20 out of 100 pizzas in a town, your market share is 20%. A high market share suggests a large firm, but this is relative to the total market size; a high share in a small market does not necessarily mean a very large firm.

Students often think a high market share always means a large business, but actually it depends on the overall size of the market. A high share in a niche market might still represent a small absolute business size.

When discussing market share, always consider the total market size. A high market share is a good indicator of leadership within an industry, but not necessarily of absolute business size.

Market Share

Calculated for a given time period; a relative measure of business size within an industry.

Beyond revenue, capital employed, market capitalisation, and market share, the number of employees is another common way to measure business size. However, no single measure is universally 'best'; the most appropriate measure depends on the purpose of the comparison and the industry context. For instance, comparing a capital-intensive manufacturing firm with a labour-intensive service provider requires careful consideration of the chosen metric.

Students often think there is one 'best' measure of business size, but actually the most appropriate measure depends on the purpose of the comparison.

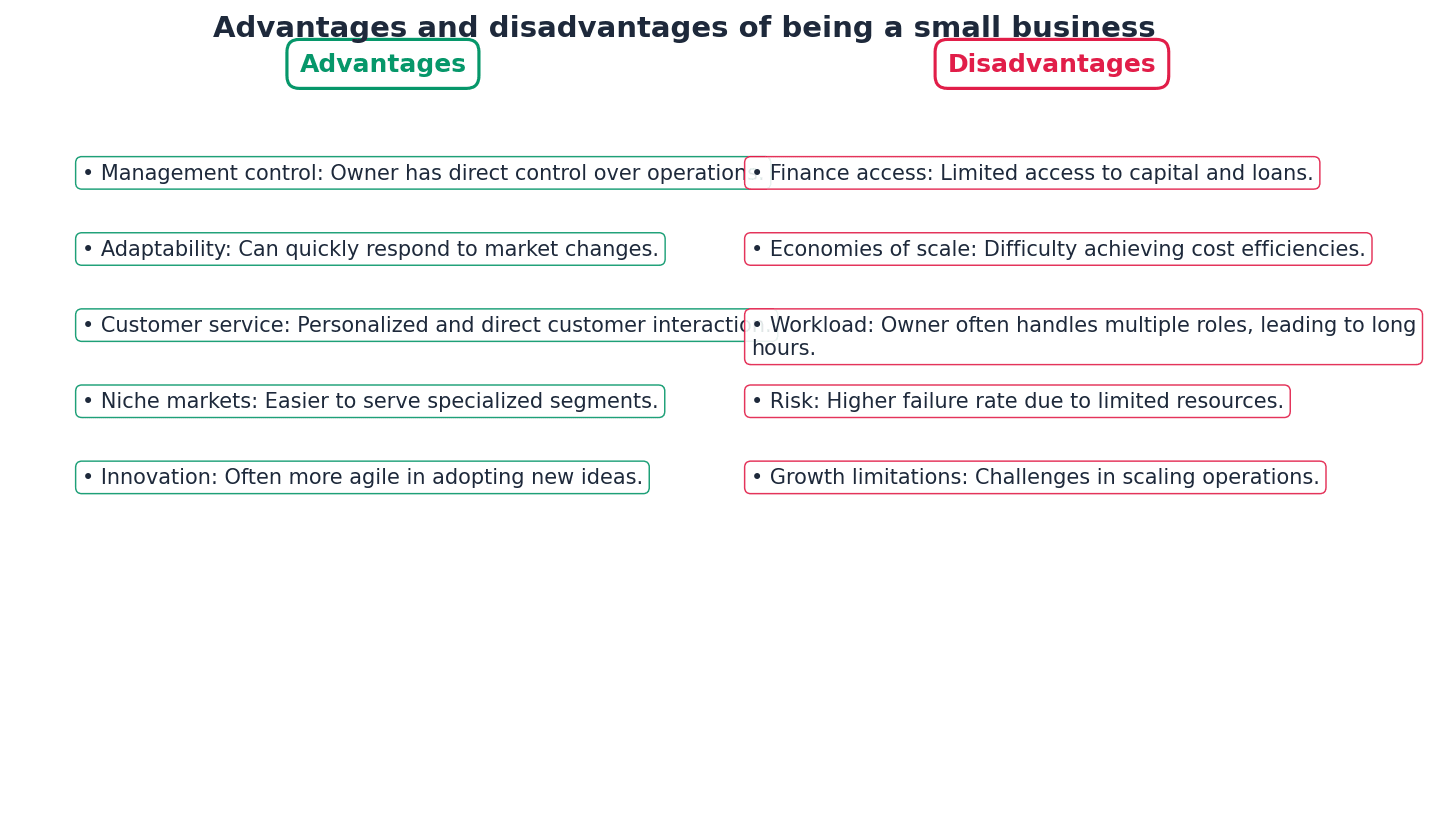

Small businesses play a crucial role in economies and industries. They are vital for employment, innovation, and competition, often acting as suppliers to larger firms. Family businesses, which can range from small enterprises to large public limited companies with controlling family interests, also contribute significantly, bringing unique strengths and weaknesses.

Students often think small businesses are insignificant, but actually they are crucial for employment, innovation, competition, and as suppliers to larger firms.

Students often think family businesses are always small, but actually many large public limited companies are family-owned with controlling interests.

Organic (internal) growth — Organic (internal) growth occurs when a business expands its operations by increasing its own output, sales, or opening new branches.

This form of growth involves expanding from within, such as a bakery opening new shops or increasing cake sales, using its own resources and reinvesting profits. It is typically slower but helps avoid problems associated with rapid expansion, like inadequate capital or management issues from integrating different business cultures.

Students often think organic growth is only about increasing sales, but actually it also includes expanding production capacity, developing new products, or entering new markets using existing resources.

When evaluating organic growth, discuss its slower pace but highlight benefits like maintaining control, avoiding culture clashes, and using retained earnings. Contrast it with the speed and risks of external growth.

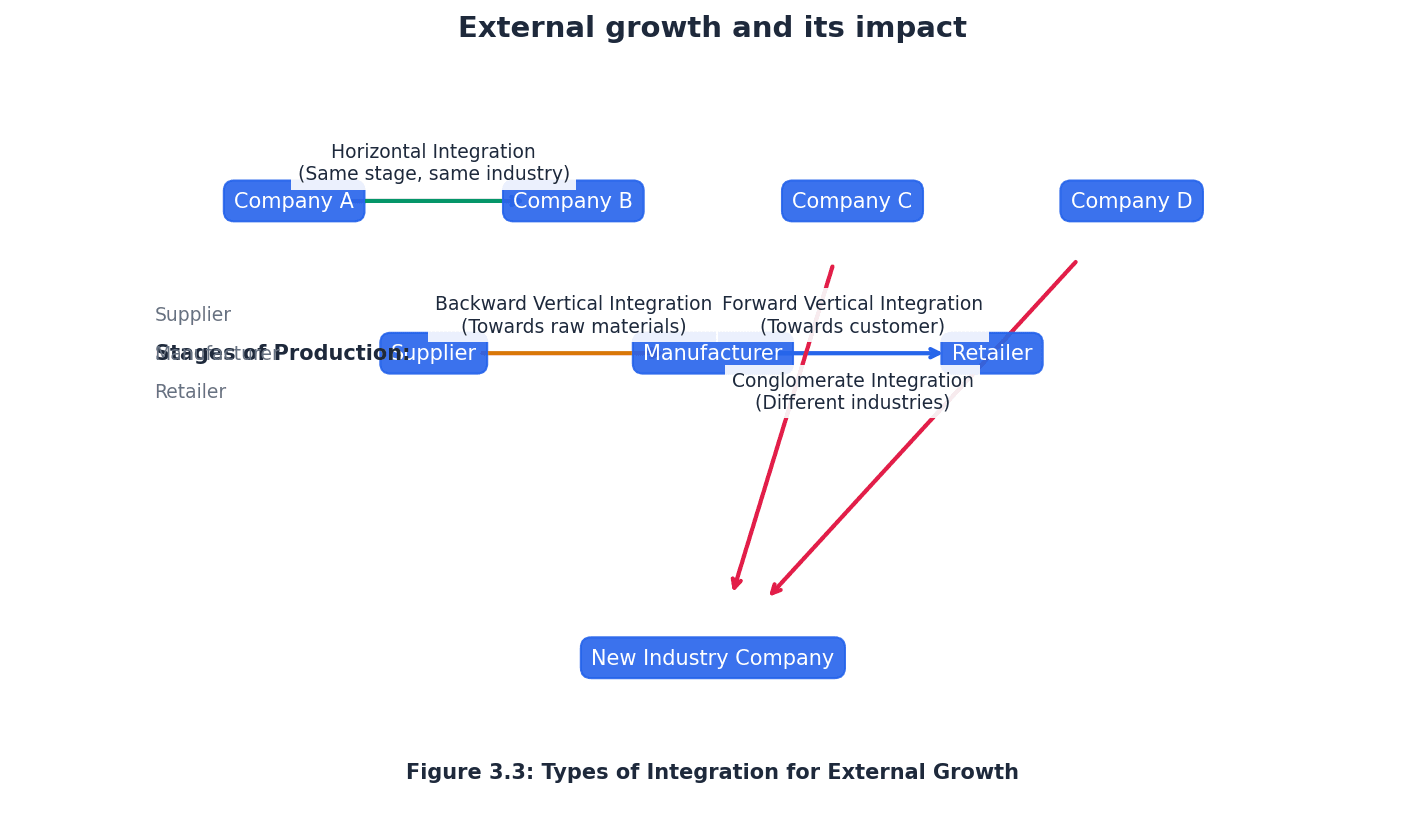

External growth — External growth, also known as integration, involves bringing together two or more businesses through mergers or takeovers.

This method allows for rapid expansion, like two puzzle pieces fitting together to form a larger picture. However, it can lead to significant management problems due to the need to combine different systems, resolve conflicts between management teams, and address cultural differences.

Students often think external growth is always successful, but actually it frequently fails to achieve its objectives due to integration challenges, culture clashes, and diseconomies of scale.

When analysing external growth, always consider the potential for management problems, culture clashes, and diseconomies of scale, as these are common reasons for failure. Evaluate its impact on various stakeholders.

Horizontal integration — Horizontal integration is the merger or takeover of a business at the same stage of production in the same industry.

This strategy eliminates a competitor and increases market share, such as McDonald's buying Burger King. It can lead to economies of scale but may also result in redundancies, reduced customer choice, and potential monopoly investigations.

Students often think horizontal integration only benefits the acquiring company, but actually it can also lead to negative impacts like job losses for workers and reduced choice for consumers.

When discussing horizontal integration, focus on market power, economies of scale, and the impact on competition. Remember to analyse both advantages and disadvantages for stakeholders like consumers and workers.

Forward vertical integration — Forward vertical integration is the merger or takeover of a business at a later stage of production in the same industry.

This allows a business to control the promotion and pricing of its products and secures an outlet, like a car manufacturer buying dealerships to move closer to the final customer. However, the business may lack experience in the new sector, and consumers might react negatively to reduced competition.

Students often think forward vertical integration guarantees success in the new stage, but actually the business may lack the specific expertise needed to manage operations effectively in that sector.

For forward vertical integration, emphasise control over distribution and marketing. Evaluate the risks of lacking experience in the new stage and the potential for consumer backlash due to reduced competition.

Backward vertical integration — Backward vertical integration is the merger or takeover of a business at an earlier stage of production in the same industry.

This strategy provides control over the quality, price, and delivery times of supplies, such as a bakery buying a wheat farm to acquire a raw material supplier. It encourages joint research and development and can limit competitors' access to materials. Risks include lack of experience in managing a supplying company and potential complacency of the acquired business.

Students often think backward vertical integration always improves supply quality, but actually the acquired supplier might become complacent due to having a guaranteed customer, potentially reducing innovation.

When analysing backward vertical integration, highlight benefits like supply chain control and quality assurance. Also, consider the potential for the acquiring firm to lack expertise in the supplying sector and the impact on competition.

Conglomerate integration — Conglomerate integration is the merger or takeover of a business in a completely different industry.

This diversifies the business, spreading risk across different markets and potentially moving into faster-growing sectors, like a shoe company buying a hotel chain. However, it can lead to a lack of management experience in the acquired sector and a lack of clear focus for the overall business.

Students often think conglomerate integration always reduces risk, but actually it can introduce new risks due to a lack of management expertise in unfamiliar industries.

For conglomerate integration, focus on diversification and risk spreading. Be sure to discuss the significant challenge of managing businesses in unrelated sectors and the potential for loss of strategic focus.

Strategic alliance — A strategic alliance is a form of external growth that involves an agreement between businesses or organisations to cooperate on a specific project or objective without complete integration or changes in ownership.

In a strategic alliance, parties remain independent, sharing resources and expertise to achieve mutual benefits, such as developing new products or entering new markets. It's like two sports teams practicing together for a tournament without merging. Alliances are often temporary and end once objectives are met.

Students often think strategic alliances involve a change of ownership, but actually the parties remain independent, cooperating on specific objectives.

Distinguish strategic alliances from mergers/takeovers by emphasising independence and the specific, often temporary, nature of the cooperation. Focus on shared resources and mutual benefits for the partners.

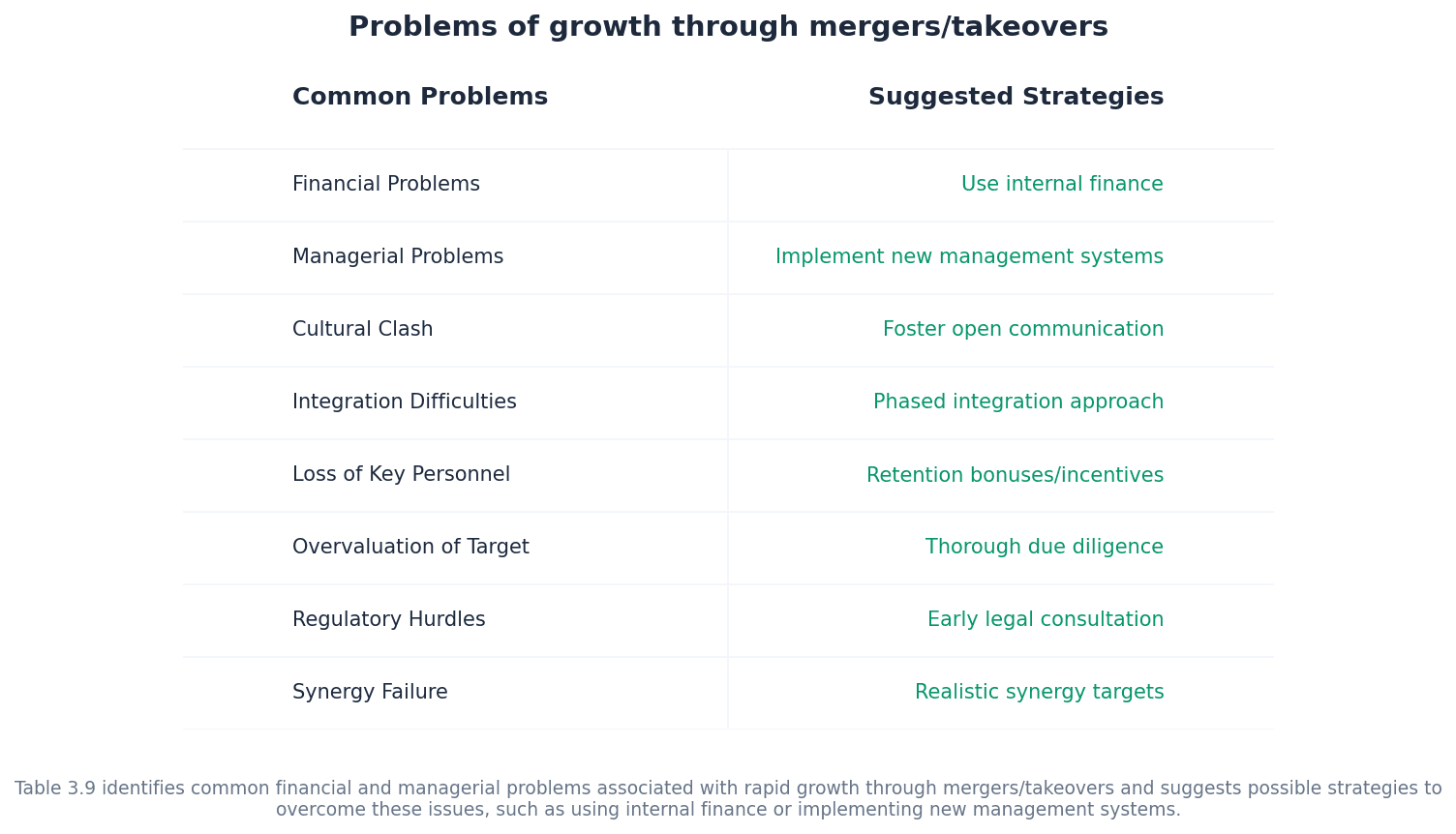

Despite the potential benefits of external growth, many mergers and takeovers fail to achieve their objectives. Common problems include significant management challenges, culture clashes between the integrating businesses, and the emergence of diseconomies of scale. These issues can lead to reduced efficiency, demotivated staff, and ultimately, a failure to realise the anticipated synergies or profitability.

Students often think external growth (mergers/takeovers) always leads to increased efficiency and profitability, but actually many fail due to management problems, culture clashes, and diseconomies of scale.

For questions on growth, evaluate the pros and cons. Don't just list the types of integration; analyse the potential for synergy vs. the risk of failure.

Provide a balanced argument. When discussing small businesses, analyse both their advantages (e.g., flexibility) and disadvantages (e.g., limited finance).

Be precise with terminology. Clearly distinguish between 'organic' and 'external' growth, and between 'horizontal', 'vertical', and 'conglomerate' integration.

Advantages & Disadvantages

Small Businesses

Organic (Internal) Growth

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the key terms from the question (e.g., 'external growth' and 'stakeholders'). Briefly outline the scope of your essay, stating that you will evaluate the impact of different forms of external growth on various stakeholders and consider reasons for potential failure.

Conclusion

Summarise your main arguments, reiterating the varied impacts of external growth on stakeholders and the significant challenges that can lead to failure. Provide a final, reasoned judgment on whether external growth is generally beneficial or detrimental, acknowledging the complexities and conditional nature of its success.

This chapter explores the crucial role of setting clear business objectives for private, public, and social enterprises, emphasizing the importance of SMART criteria. It analyzes the links between mission statements, aims, objectives, strategies, and tactics, and their role in effective decision-making. The chapter also discusses the growing significance of corporate social responsibility, the triple bottom line, and how ethical considerations can influence business objectives and activities over time.

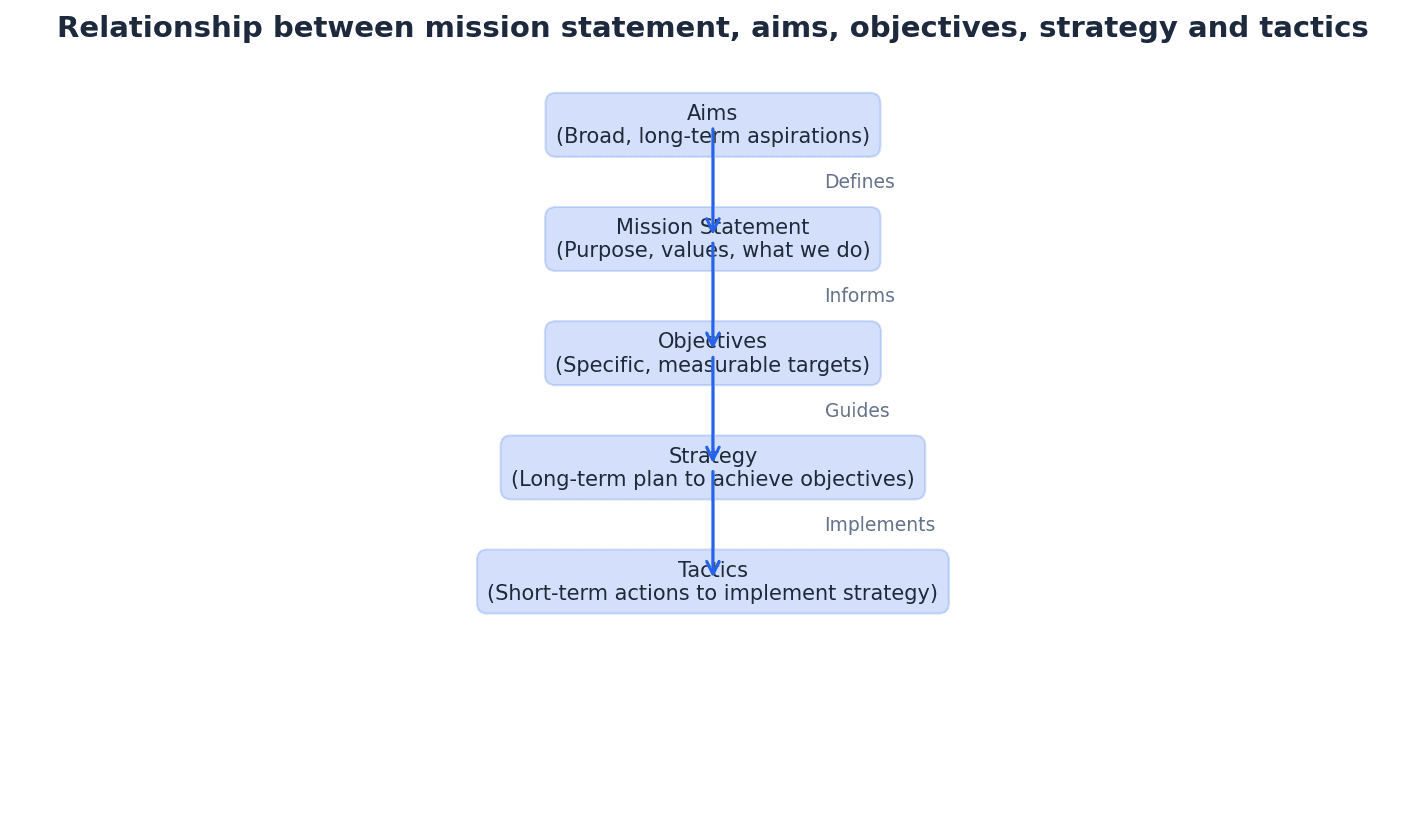

Business aims — The core central purpose of a business’s activity, expressed as broad indications of what a business hopes to achieve in future.

Aims are general, long-term statements of intent that are not expressed in SMART terms. They provide the overall direction for the business and must be converted into specific objectives to be actionable. For example, a country's aim might be 'to improve the quality of life for its citizens', which is broad and aspirational.

Mission statements — An attempt to condense the central purpose of a business’s existence into one statement, summing up the business aim in a motivating and appealing way.

Mission statements are not concerned with specific, quantifiable goals but provide a vision and overall sense of purpose. They inform external groups, motivate employees, and guide behaviour, though they can be vague. A school's mission statement might be 'To foster a love of learning and prepare students for global citizenship', which is an overarching philosophy.

Students often confuse aims with objectives, but actually aims are broad, qualitative statements of purpose, while objectives are specific, measurable, and time-bound targets derived from those aims.

Students often think mission statements are the same as objectives, but actually mission statements are broad, qualitative declarations of purpose, whereas objectives are specific, measurable targets.

Distinguish clearly between aims and objectives in your answers. Aims provide the overall vision, while objectives are the concrete steps to achieve that vision.

SMART objectives — Business objectives that are Specific, Measurable, Achievable, Realistic and relevant, and Time-limited.

This acronym provides a framework for setting effective objectives that are clear, quantifiable, attainable, pertinent to the business's resources, and have a defined deadline. General objectives are often meaningless without these criteria. For instance, instead of saying 'I want to get fit', a SMART objective would be 'I will run 5km in under 30 minutes by the end of three months'.

Students often think 'Achievable' and 'Realistic' are the same, but actually 'Achievable' refers to the possibility of reaching the target, while 'Realistic' considers the company's resources and current market conditions.

When asked to analyse SMART objectives, break down an example objective and explain how it meets each of the five criteria. Also, discuss the benefits of using SMART objectives for decision-making and motivation.

Setting clear business objectives is critical for private, public, and social enterprises. Objectives provide direction, enable effective decision-making, and allow for the measurement of progress. They help to translate broad aims into actionable targets, ensuring that all activities within the business contribute towards a common purpose.

Business strategies — The long-term plans of action of a business, providing the focus for how aims and objectives will be achieved.

Strategies are developed based on clear objectives and guide important decisions for the business as a whole or for individual departments. They address how a business will compete, grow, and achieve its goals over an extended period. For example, if an objective is to 'increase market share by 20%', a strategy might be 'to enter new international markets'.

Tactical decisions — Small-scale, short-term decisions taken to implement a broader business strategy.

Once a strategy has been decided, tactical decisions are the operational choices made to execute that strategy. They are more detailed and immediate than strategic decisions. If the strategy is 'to enter new international markets', a tactical decision might be 'to launch a specific advertising campaign in India next month'.

Students often confuse strategies with tactics, but actually strategies are the overarching long-term plans, while tactics are the specific, short-term actions taken to implement those strategies.

When analysing strategies, ensure you link them directly to the business's objectives. Explain how a particular strategy helps achieve a specific objective, rather than just describing the strategy itself.

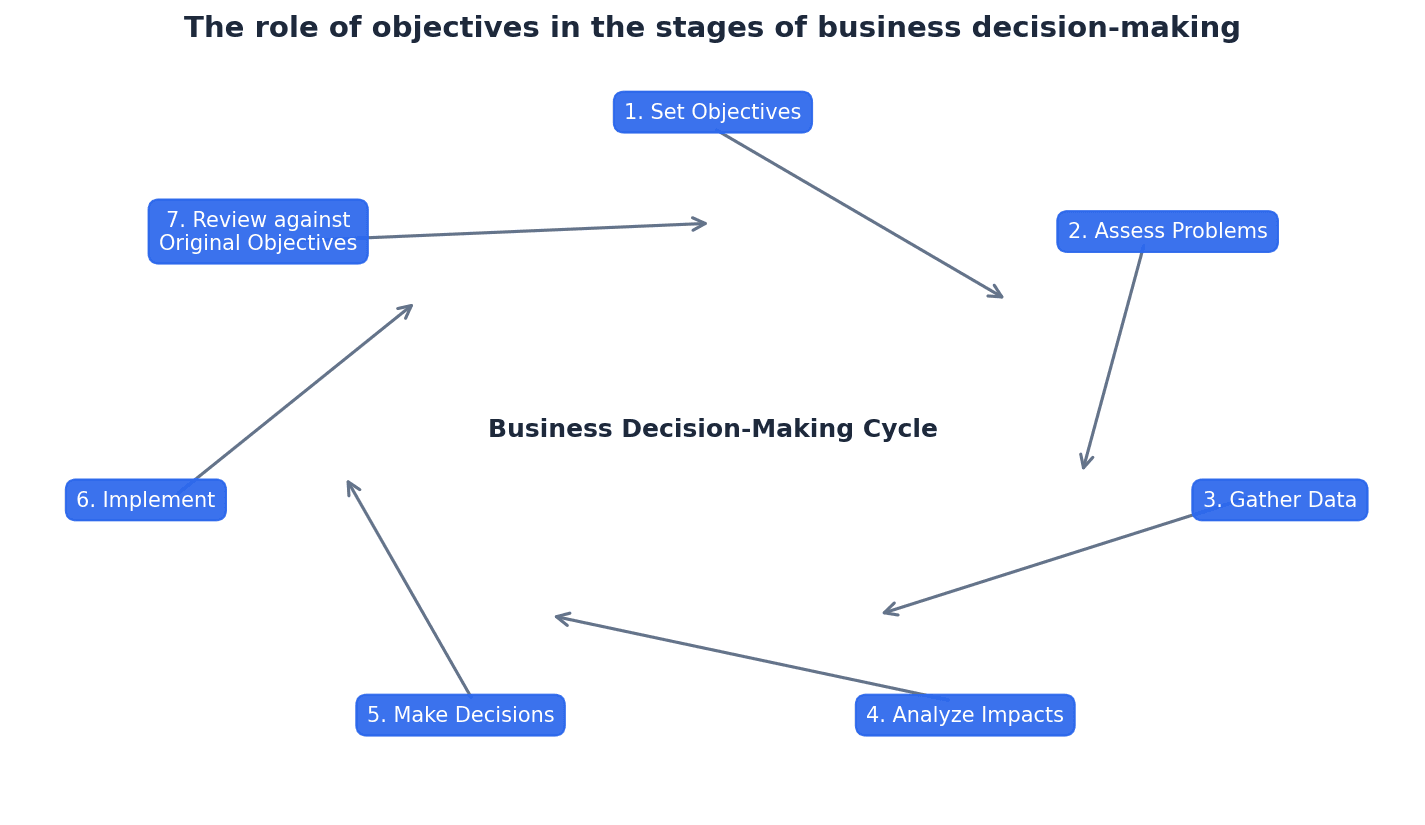

Objectives play a crucial role in business decision-making by providing a clear framework for choices. They guide the allocation of resources, the development of strategies, and the evaluation of outcomes. Without clear objectives, decisions can become arbitrary and lack coherence, potentially leading to inefficient operations and missed opportunities.

Private sector businesses typically focus on financial objectives. Common objectives include profit maximisation, growth, increasing market share, survival, maximising short-term revenue, and increasing shareholder value. These objectives are driven by the need to generate returns for owners and investors, and to ensure the long-term viability of the business in a competitive environment.

Profit maximisation — Producing at the level of output where the greatest positive difference between total revenue and total costs is achieved.

This objective aims to achieve the highest possible profit. While it rewards investors and finances growth, it can attract competitors, lead to short-term focus, and may conflict with other stakeholder interests like job security or environmental protection. Imagine a lemonade stand owner who constantly adjusts the price and number of cups sold to find the exact combination that brings in the most money after all costs are paid.

Students often think profit maximisation means selling as much as possible, but actually it means finding the optimal balance between revenue and costs to achieve the highest absolute profit.

When asked to evaluate profit maximisation, consider both its benefits (e.g., shareholder returns, reinvestment) and its limitations (e.g., short-term focus, stakeholder conflicts, difficulty in measurement).

Profit satisficing — Aiming to achieve enough profit to keep the owners satisfied, rather than earning as much profit as possible.

This is a common aim for small business owners who prioritise a comfortable lifestyle, leisure time, or work-life balance over working longer hours to maximise profits. Once a satisfactory profit level is reached, other aims take priority. A freelance graphic designer might aim to earn enough to cover their living expenses and save a bit, then decline extra work to enjoy their weekends.

Students often think profit satisficing means making minimal profit, but actually it means achieving a 'sufficient' or 'acceptable' level of profit that meets the owners' needs and allows for other non-financial objectives.

When discussing profit satisficing, link it to the objectives of small business owners and their desire for work-life balance or independence, contrasting it with the pure financial drive of larger corporations.

Social enterprises have a distinct set of objectives, often balancing financial viability with social and environmental impact. Public sector businesses, on the other hand, typically focus on providing essential services, improving public welfare, and operating within budgetary constraints, rather than profit generation. Their objectives are often driven by government policy and public need.

Triple bottom line — The three main aims of social enterprises: economic (financial), social, and environmental.

This concept suggests that businesses, especially social enterprises, should measure their success not just by profit, but also by their positive impact on people (social) and the planet (environmental). It signifies that profit is not the sole objective. Imagine a coffee shop that not only makes a profit, but also employs homeless individuals and uses compostable cups while sourcing fair-trade beans.

Students often think the triple bottom line only applies to charities, but actually it's a framework for social enterprises and increasingly for other businesses committed to CSR, to measure performance across profit, people, and planet.

When discussing the triple bottom line, ensure you explicitly mention and explain each of the three components (profit, people, planet) and how they contribute to a holistic view of business success, especially for social enterprises.

Corporate social responsibility (CSR) — The concept that businesses should consider the interests of society by taking responsibility for the impact of their decisions and activities on customers, employees, communities and the environment.

CSR involves businesses adopting a wider perspective than just profit, incorporating social, environmental, and ethical issues into their objectives. This can be driven by public pressure, legal changes, or a genuine concern for 'public responsibility'. A clothing company that ensures its factories pay fair wages, use sustainable materials, and avoid child labor, even if it costs more, is demonstrating CSR.

Students often think CSR is just about donating to charity, but actually it encompasses a broader commitment to ethical practices, environmental sustainability, and positive social impact throughout all business operations.

When analysing CSR, evaluate both the potential benefits (e.g., improved reputation, increased sales, employee motivation) and the potential drawbacks (e.g., increased costs, reduced short-term profits) and consider whether it's a genuine commitment or a PR exercise.

Ethical code of conduct — A document detailing a company's rules and guidelines on how employees should behave and make decisions in situations with an ethical or moral dimension.

This code helps guide employees through ethical dilemmas, ensuring consistency in behaviour and decision-making that aligns with the company's values. It covers issues beyond legal requirements. Think of a school's student handbook that outlines rules on academic honesty, respect for others, and appropriate online behaviour.

Students often think an ethical code is just about following the law, but actually it goes beyond legal requirements to define what the company considers morally right or wrong, even if not legally mandated.

When analysing ethical codes, discuss how they can influence both business objectives (e.g., setting CSR goals) and activities (e.g., supplier choice, advertising practices), and evaluate the short-term costs versus long-term benefits.

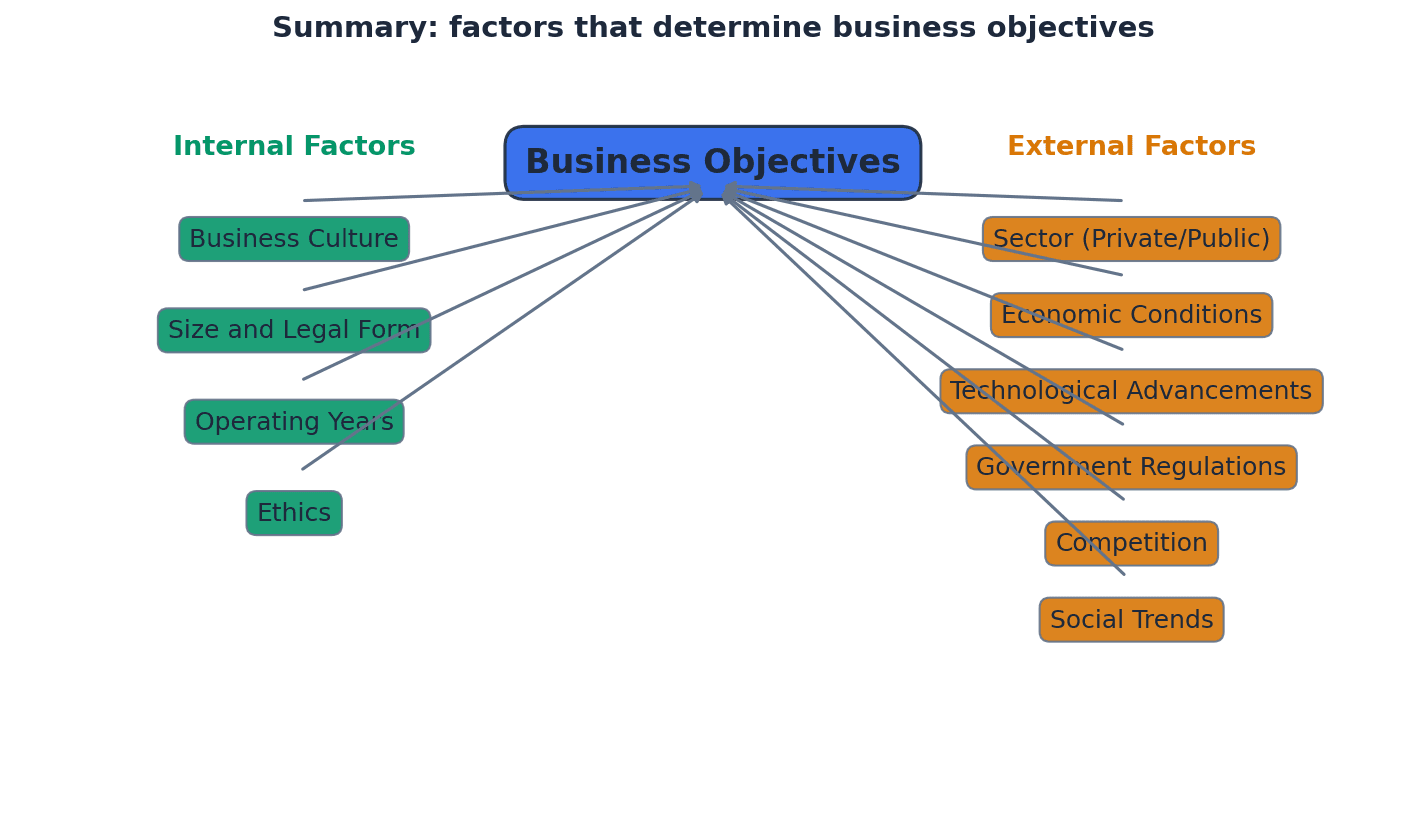

Business objectives are not static; they evolve over time due to various internal and external factors. These include the business's age, size, legal form, and whether it operates in the private or public sector. The competitive environment, economic conditions, and changes in business culture or ethical considerations can also significantly influence a business's priorities and objectives.

Demonstrate higher-level understanding by explaining how a business's objectives might need to change over time in response to internal or external factors.

In case studies, always link a business's objectives to its type (e.g., private, public, social enterprise) to explain its priorities.

Advantages & Disadvantages

Profit maximisation

Corporate Social Responsibility (CSR)

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining key terms such as 'business objectives' and 'CSR' (if relevant to the question). Briefly state the importance of objectives and outline the main arguments you will present regarding their influence or evolution.

Conclusion

Summarise your main arguments, reiterating the dynamic nature and critical role of objectives in business success. Provide a final, balanced judgement on the extent to which objectives are influenced by various factors or the overall effectiveness of specific objective-setting approaches.

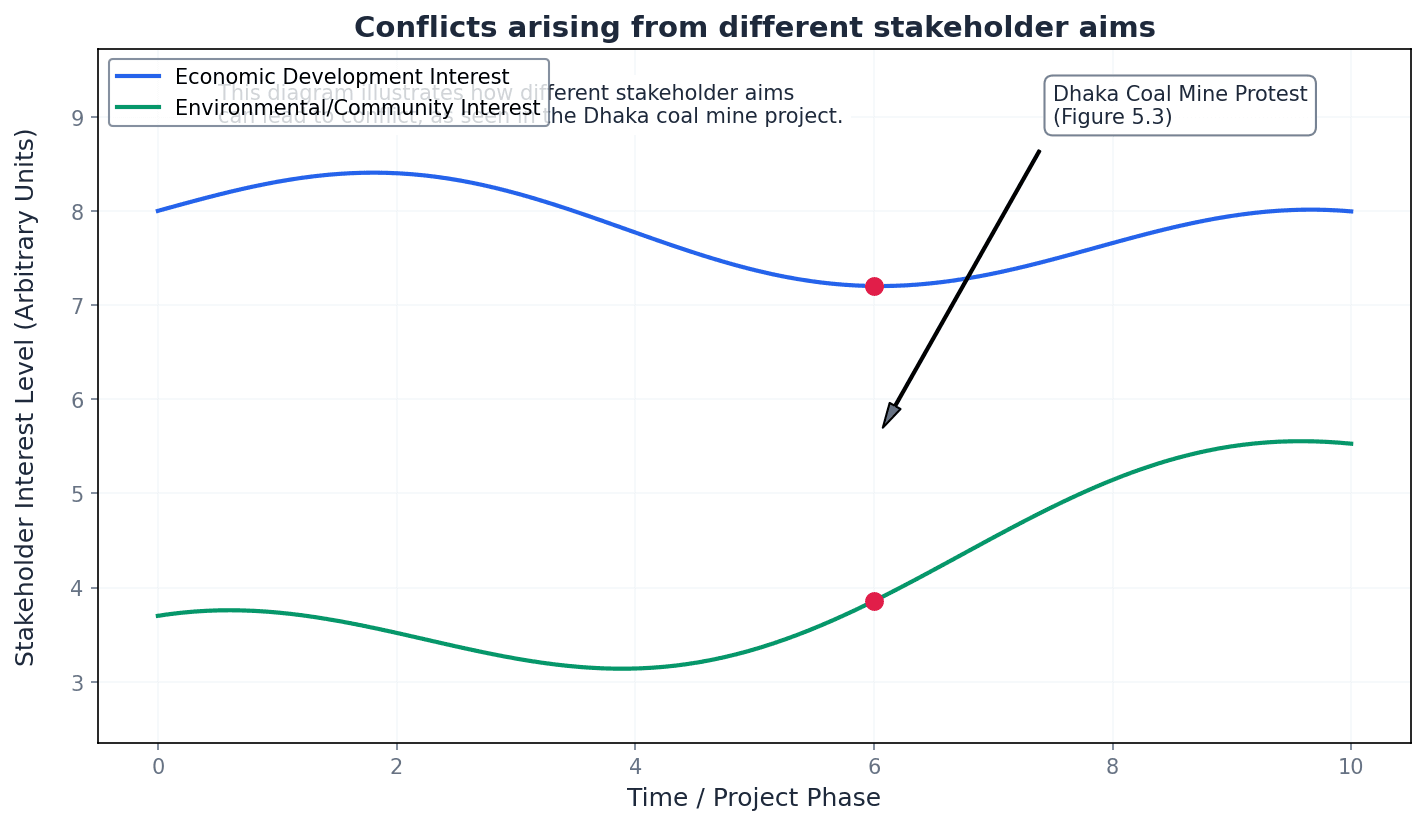

This chapter explores the concept of stakeholders, defining them as any group or individual with an interest in a business, and distinguishes between internal and external types. It examines their roles, rights, and responsibilities, and assesses how business decisions impact them, highlighting the importance of accountability. The chapter also addresses how stakeholder aims influence business decisions, identifies potential conflicts, and evaluates strategies for resolution.

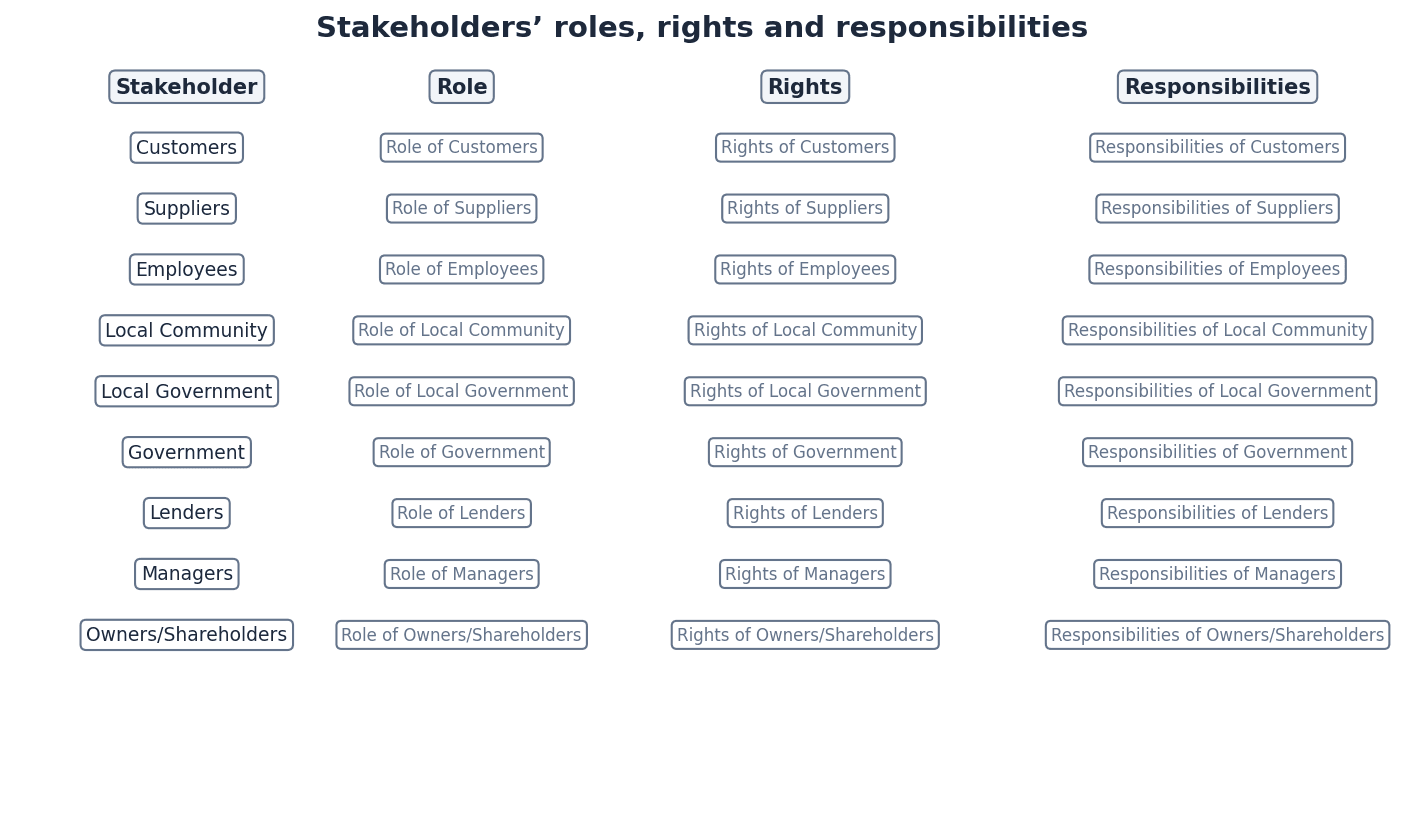

Stakeholder — A stakeholder is any individual or group with an interest in the activities of a business.

This broad term includes both internal groups, such as employees and owners, and external groups like customers, suppliers, and the government. Their interests can be directly or indirectly affected by business decisions, much like how actors, directors, parents, and the audience all have an interest in a school play's success.

Students often confuse 'stakeholder' with 'shareholder'. Remember that a stakeholder is a much broader term covering anyone affected by or affecting the business, while a shareholder is just one type of stakeholder.

Shareholder concept — The traditional view that the primary duty of a company is to its shareholders, focusing on increasing shareholder value.

This concept implies that directors and managers are legally bound to prioritise the financial interests of the owners, making decisions with the goal of maximising profits and returns for shareholders. This is similar to a sports team focusing solely on winning the championship for its owner, potentially neglecting fan experience.

When evaluating business decisions, consider how they align with or diverge from the shareholder concept. Use terms like 'legally binding duty' to demonstrate understanding of its significance.

Stakeholder concept — The view that businesses should consider the interests of all parties involved in and affected by business activity, not just the owners.

This broader perspective acknowledges that various groups, including local communities, the public, government, and environmental groups, have legitimate interests that should influence business decision-making. Ignoring these can lead to negative reactions, much like a community garden project considering local residents and environmental groups, not just the gardeners.

Students often think the shareholder concept is outdated and no longer relevant. However, it remains a legally binding duty for companies in many jurisdictions, though often balanced with stakeholder considerations.

Students often think the stakeholder concept means ignoring shareholder interests. In reality, it means balancing shareholder interests with those of other groups, which can often lead to long-term benefits for shareholders too.

Accountability — The responsibility of a business to justify its actions and decisions to its stakeholders.

This involves being transparent about operations and demonstrating how decisions consider the aims and impacts on various stakeholder groups. Increased corporate social responsibility often leads to greater accountability, much like a student being accountable to their teacher for homework.

Students often think accountability is just about legal compliance. However, it extends to ethical and social responsibilities beyond what is legally mandated.

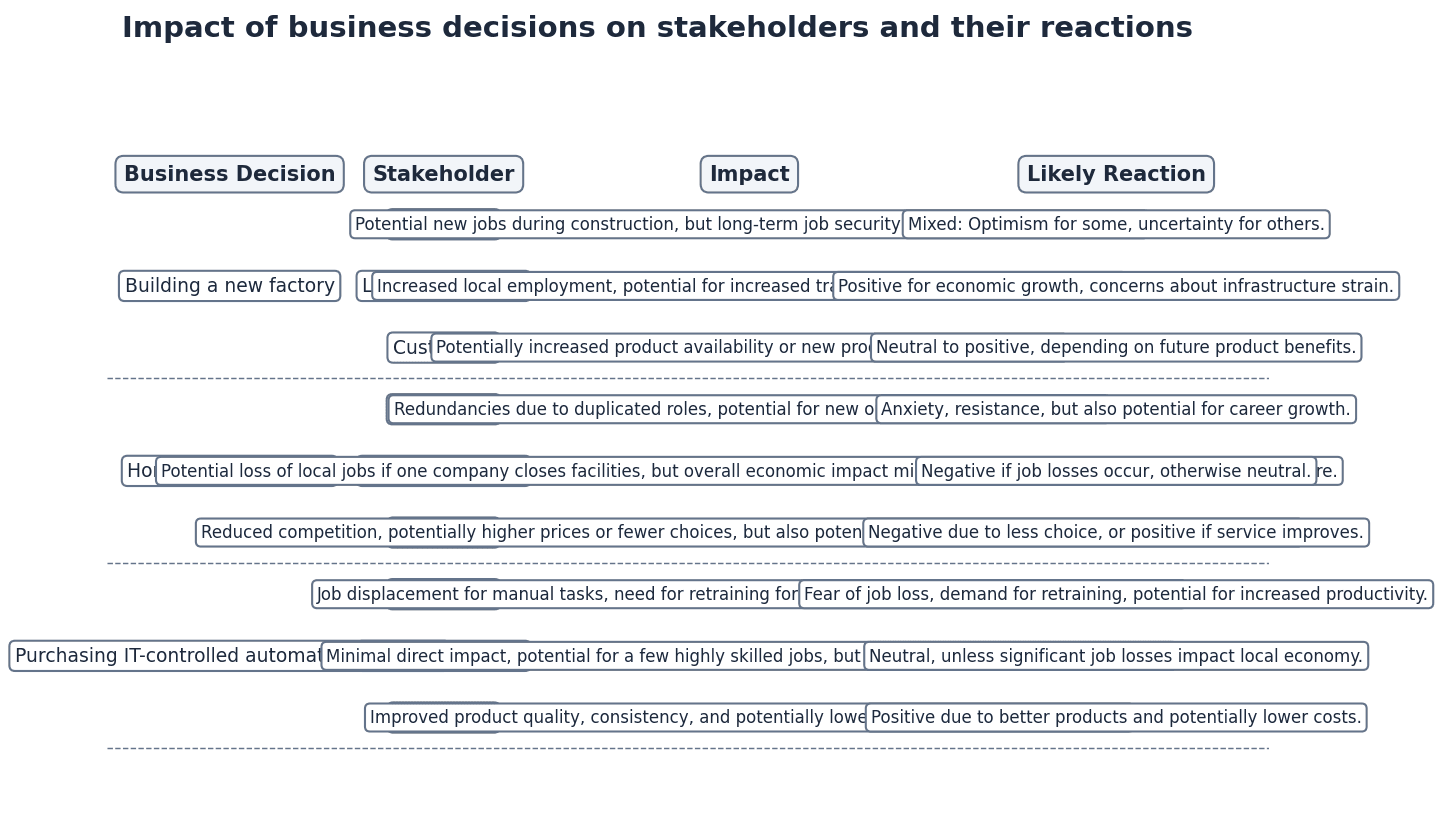

Stakeholders are individuals or groups with an interest in a business's activities. They can be categorised as either internal, such as employees and managers, or external, including customers, suppliers, the local community, and the government. Understanding this distinction is crucial for analysing their varying interests and influence.

Key business stakeholders have distinct roles, rights, and responsibilities. For instance, employees have a right to fair pay and safe working conditions, while customers have a right to safe products. Businesses, in turn, have responsibilities to these groups, such as providing fair pay for employees and prompt payment to suppliers. These responsibilities extend beyond legal obligations to include ethical and social considerations.

Business decisions inevitably impact various stakeholder groups, often leading to different reactions. For example, a decision to cut costs might lead to job losses, negatively affecting employees and the local community. Conversely, investing in new technology could benefit shareholders through increased profits and customers through improved products. Businesses must be accountable for these impacts, justifying their actions and demonstrating transparency.

When analysing accountability, link it to specific business actions or policies, such as publishing Corporate Social Responsibility (CSR) reports or engaging in community consultations. Explain how this can build trust and reputation.

Stakeholder aims and objectives often conflict. For example, shareholders may desire higher profits, which could clash with employees wanting higher wages or customers demanding lower prices. Businesses must assess these conflicting aims and evaluate strategies to respond, which might involve compromise, prioritisation, or seeking long-term benefits that satisfy multiple groups. Changing business objectives will also impact different stakeholder groups in varying ways, often creating new conflicts.

Students often believe that all stakeholder aims can be met simultaneously. However, conflicts are common and require compromise or prioritisation by the business.

Students may think that meeting stakeholder aims always reduces profits. In reality, it can lead to long-term benefits, such as improved reputation, increased customer loyalty, and higher profits.

When asked to 'analyse' stakeholders, ensure you discuss both their interest in the business and how business decisions impact them, and vice versa. Distinguish between internal and external stakeholders.

When discussing the stakeholder concept, provide specific examples of how different stakeholder groups' interests might be considered. Use command words like 'assess' or 'evaluate' to discuss the implications of adopting this approach.

In evaluation questions, justify which stakeholder group a business might prioritise and why, linking your reasoning to the business's objectives or its adoption of the stakeholder/shareholder concept.

When analysing a business decision, always consider the impact on at least two different stakeholder groups to show balance and identify potential conflict.

Advantages & Disadvantages

Adopting the Shareholder Concept

Adopting the Stakeholder Concept

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining 'stakeholder' and briefly outlining the distinction between internal and external stakeholders. State the main argument or approach your essay will take regarding the impact of stakeholders or the resolution of conflicts.

Conclusion

Summarise your main arguments, reiterating the complexity of managing stakeholder relationships. Provide a final, justified judgment on how businesses should approach stakeholder management, perhaps linking it to the concept of accountability and long-term sustainability.

This chapter explores the diverse external influences on business activity, encompassing political, legal, social, demographic, technological, competitive, international, and environmental factors. It examines how government interventions, legal controls, societal shifts, and technological advancements impact business decisions, alongside the growing importance of sustainability and corporate social responsibility.

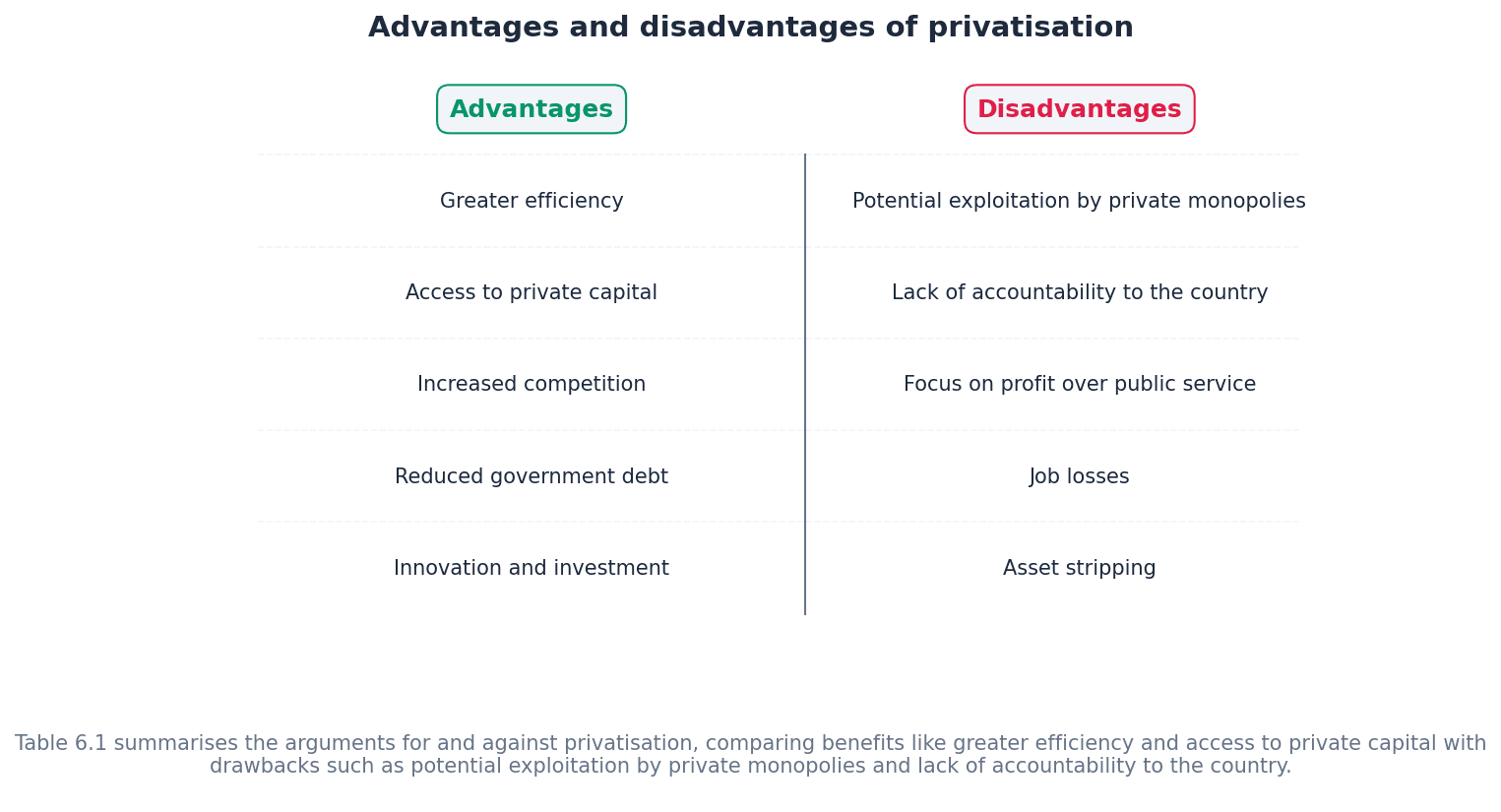

Privatisation — The transfer of ownership of state-owned industries into the private sector by creating public limited companies.

Shares in these newly formed public limited companies are sold through the stock exchange. This is like selling a public library system to a private company, which would then run it for profit, potentially charging for services that were once free.

Students often think privatisation always leads to better services, but actually it can lead to higher prices or reduced access for some consumers if profit becomes the sole driver.

When evaluating privatisation, ensure you discuss both the claimed advantages (e.g., efficiency, investment) and disadvantages (e.g., public interest, monopolies) and justify your conclusion with specific examples.

Nationalisation — The process of the state buying privately owned businesses to bring them under government control.

This is often done to ensure essential services are provided based on societal needs rather than just profit, or to save struggling industries. If a country's main railway system is privately owned and facing bankruptcy, nationalisation would be the government buying it to keep it running, potentially prioritising public service over profit.

Students often think nationalisation means the business will always be inefficient, but actually it can allow for integrated policy and economies of scale, though it may lack profit incentives.

When analysing nationalisation, consider the trade-offs between social objectives (e.g., public service, preventing exploitation) and economic efficiency, using examples to illustrate the impact on stakeholders.

Governments intervene in business ownership through privatisation and nationalisation, impacting market structure and service provision. Beyond ownership, legal controls are used to regulate business activity, influencing decisions related to employment, consumer rights, and competition. These interventions aim to balance economic efficiency with social welfare.

Minimum wage — A legally binding lowest hourly rate that employers can pay their workers.

The two main aims are to prevent exploitation of poorly organised workers and reduce income inequalities. This is like a price floor for labour, ensuring workers earn at least a certain amount per hour.

Students often think a minimum wage always benefits all low-paid workers, but actually some businesses might respond by reducing staff numbers or slowing hiring, leading to job losses for some.

When discussing minimum wage, evaluate both the positive impacts (e.g., increased living standards, work incentive) and negative impacts (e.g., uncompetitiveness, job losses, inflation) on businesses and the economy.

Governments use legal controls to regulate employment practices, including recruitment, contracts, termination, and health and safety at work. Consumer protection laws ensure product safety and fair marketing, while competition laws prevent monopolies and anti-competitive practices. Businesses must adapt their strategies to comply with these evolving legal frameworks.

Corporate social responsibility (CSR) — When a business accepts its legal and moral obligations to all stakeholders, not just investors.

This involves considering the impact of business decisions on society and the environment, going beyond just making a profit. It's like a company that not only makes good products but also ensures its factories are safe, its workers are paid fairly, and it doesn't pollute the local river.

Students often think CSR is just about charity, but actually it encompasses a much broader range of ethical and environmental practices integrated into core business operations.

When evaluating CSR, consider the benefits (e.g., improved public image, attracting talent) and costs (e.g., higher expenses, potential for greenwashing) and how it impacts different stakeholder groups.

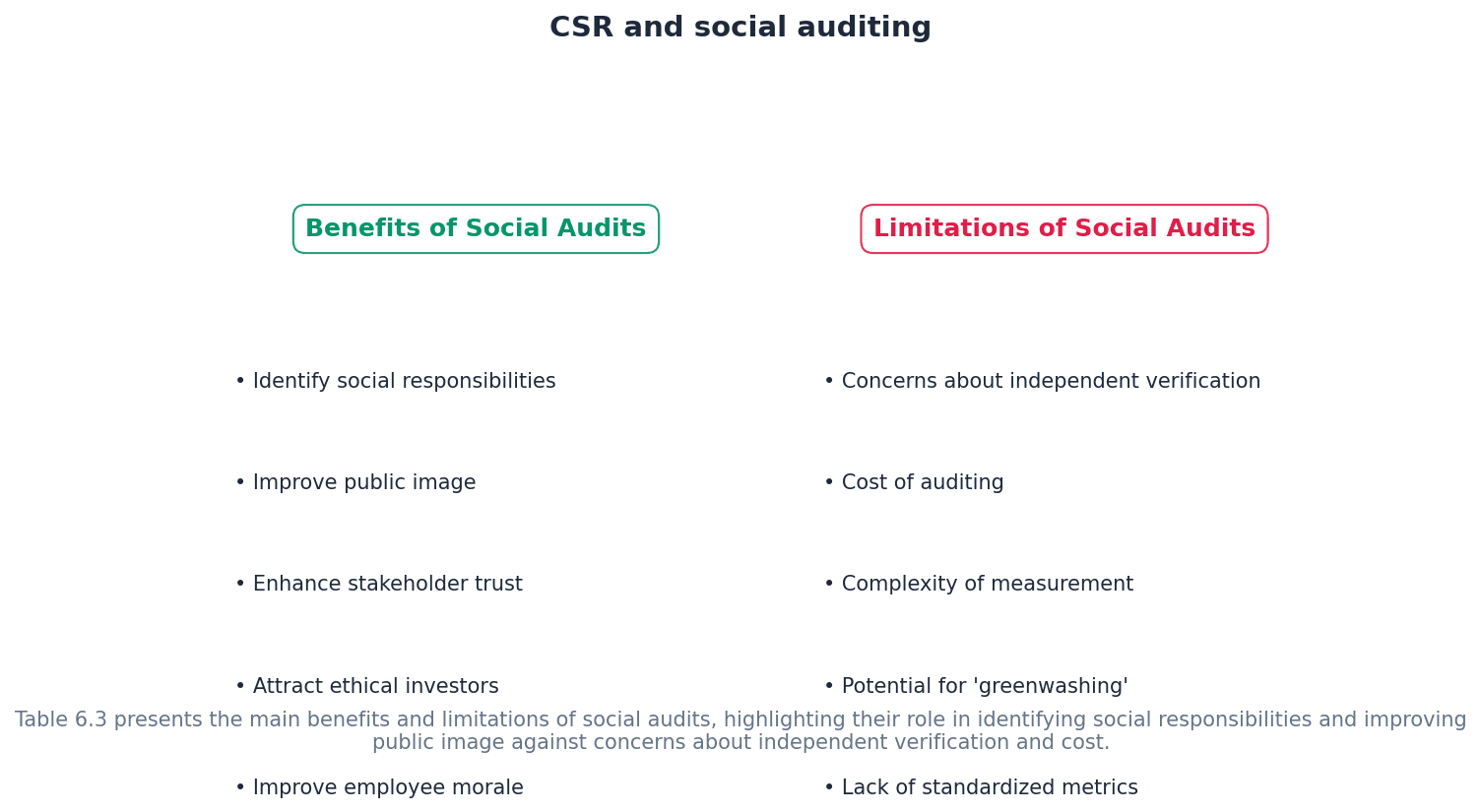

Social audits — Annual reports that indicate the social impact of a business over a period, showing efforts to meet social responsibilities.

These audits typically include health and safety records, pollution levels, community contributions, and ethical sourcing. Just as a financial audit checks a company's money, a social audit checks a company's 'goodness' – how it treats its employees, the environment, and the community.

Students often think social audits are legally binding and always accurate, but actually they are often voluntary and may not be independently checked, leading to concerns about their credibility.

When assessing social audits, discuss their benefits (e.g., identifying areas for improvement, marketing tool) and limitations (e.g., lack of independent verification, cost, potential for 'smokescreen') to provide a balanced evaluation.

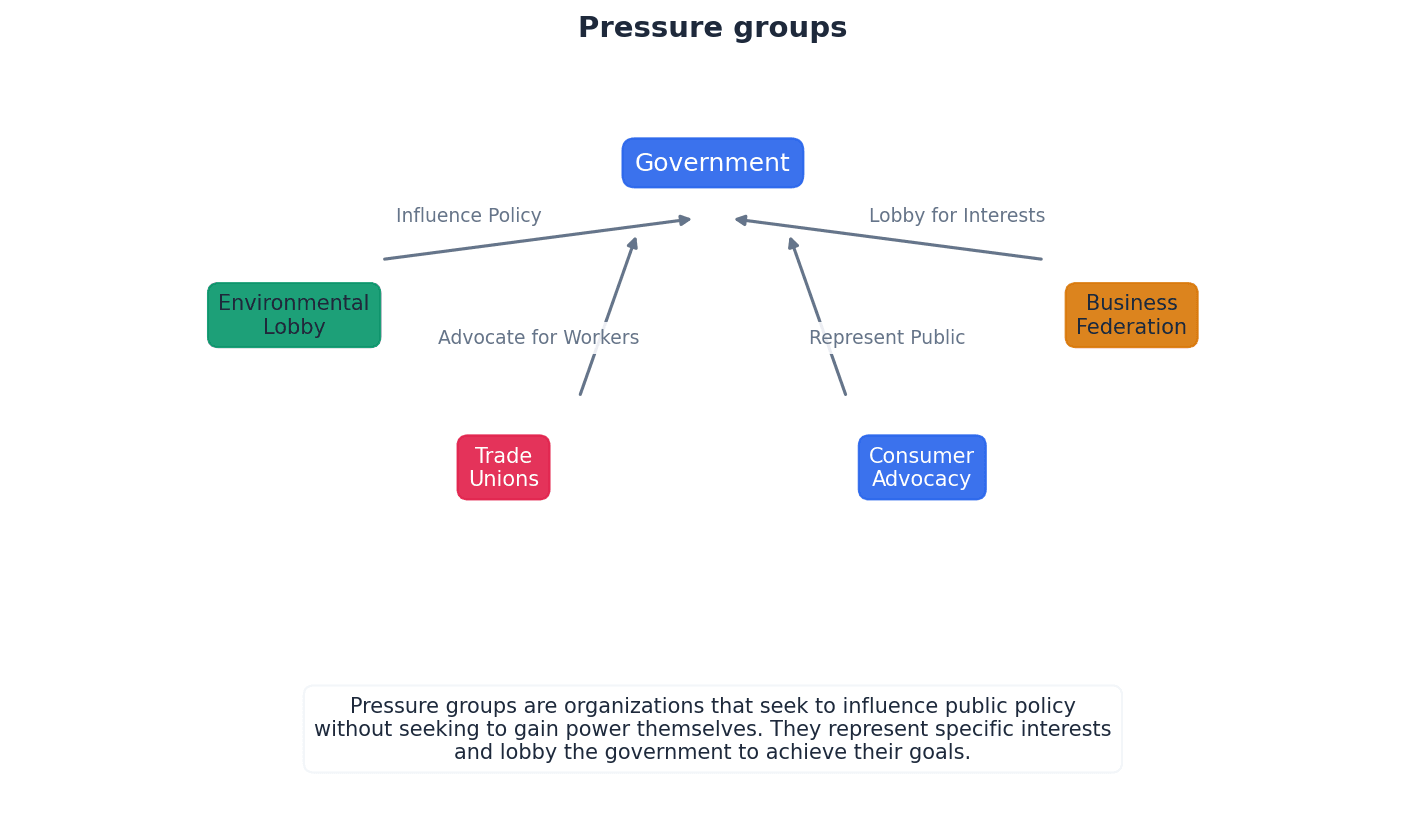

Pressure groups — Organisations that seek to influence business and government decisions to achieve specific aims, often related to social or environmental issues.

They achieve their goals through publicity, influencing consumer behaviour (e.g., boycotts), and lobbying governments to change laws. They act as a collective voice for a cause, mobilising people to force change.

Students often think pressure groups only target businesses, but actually they also lobby governments to introduce new laws or change existing policies.

When evaluating the impact of pressure groups, analyse their methods (e.g., media, boycotts, lobbying) and how these can create both threats (e.g., bad publicity, reduced sales) and opportunities (e.g., improved reputation by responding) for businesses.

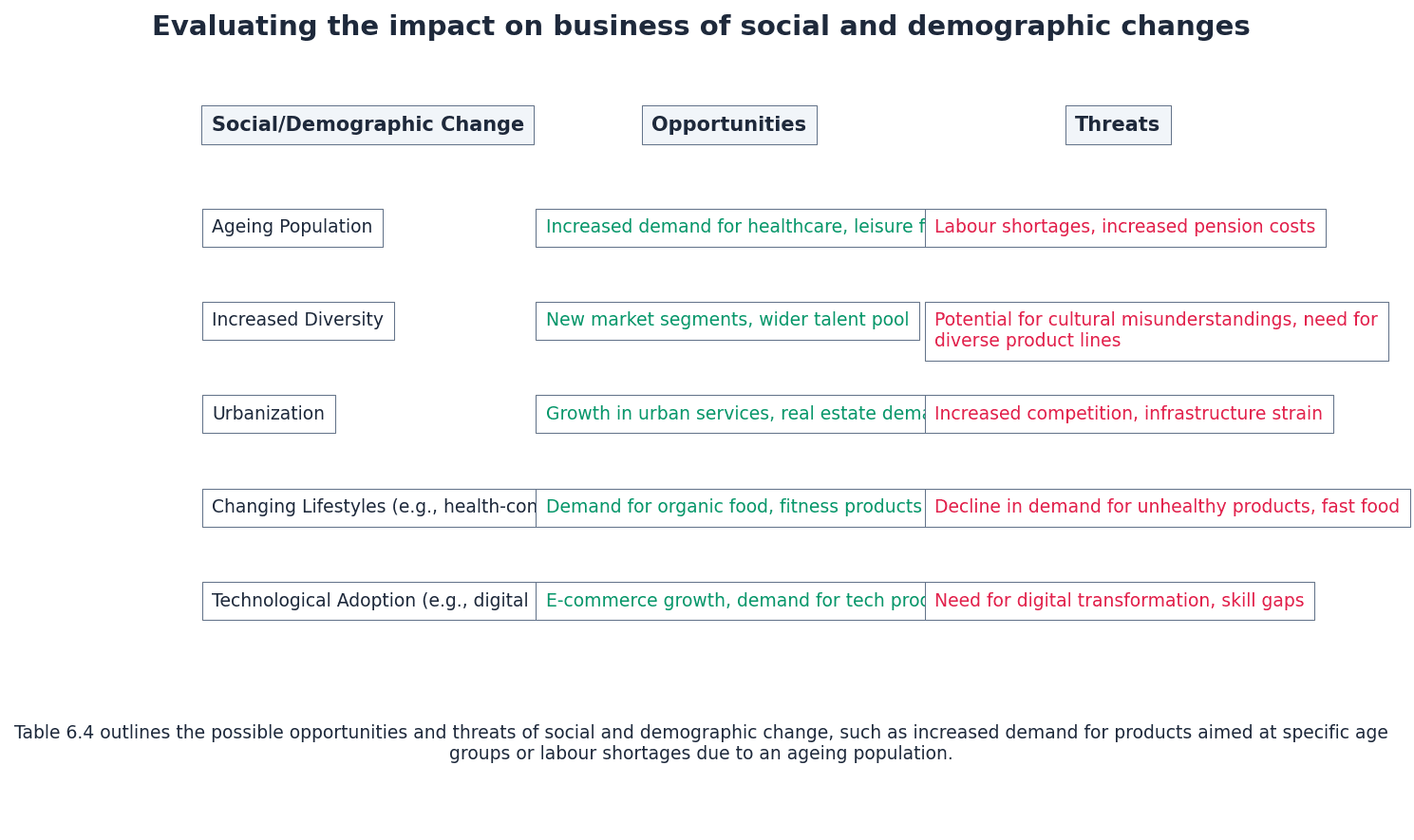

Changes in society, such as an ageing population or evolving employment patterns, significantly impact business strategy. Businesses must adapt to new consumer needs, workforce demographics, and societal expectations regarding ethical conduct and community engagement. Understanding these shifts is crucial for identifying new market opportunities and managing human resources effectively.

Technological advancements present both opportunities and threats to businesses. They can disrupt existing markets, but also provide valuable data for decision-making, enhance efficiency, and foster innovation. Businesses must effectively introduce and manage new technologies to remain competitive and meet evolving customer demands.

Multinational business — A business that has its headquarters in one country but owns operations that produce goods and services in more than one country.

Multinationals expand globally to be closer to markets, access lower production costs, avoid import restrictions, and gain access to natural resources. An example is a fast-food chain with headquarters in one country but owning and operating restaurants in many others.

Students often think a multinational is just a company that sells products in more than one country, but actually it must also own and operate production facilities in multiple countries.

When discussing multinationals, ensure you distinguish between simply exporting/importing and owning operations abroad. Evaluate both the benefits (e.g., jobs, investment) and drawbacks (e.g., exploitation, profit repatriation) for host countries.

International trade and multinational corporations play a significant role in shaping the business environment. International trade agreements can open new markets or impose restrictions, while technology facilitates global operations. Multinationals bring benefits like employment and foreign currency to host countries but also pose risks such as exploitation and cultural imposition.

Sustainability — The ability of our global community to continue to enjoy current standards of living by making business decisions that help protect the environment for future generations.

Sustainable business decisions involve practices like replanting forests, avoiding over-exploitation of resources, and responsible waste disposal. It's like not picking all the fruit from a tree at once, but leaving enough for it to continue producing year after year.

Students often think sustainability is only about environmental protection, but actually it also encompasses social and economic aspects to ensure long-term well-being for all.

When discussing sustainability, link business decisions to their long-term impact on resources and future generations, considering both environmental and economic implications.

Greenwashing — Making misleading or untrue claims about a business's environmental practices or benefits.

This practice aims to create a false impression of environmental responsibility but can backfire badly if discovered, leading to bad publicity and damage to brand image. It's like painting a rusty, polluting car green and calling it 'eco-friendly' without actually changing its engine or emissions.

When evaluating environmental claims, consider the potential for greenwashing and its long-term negative impact on brand image and consumer loyalty, contrasting it with genuine sustainability efforts.

Environmental audits — Independent checks that evaluate a business's environmental performance, reporting on factors like pollution, waste, energy use, and recycling rates.

These audits compare current performance with previous years and targets, and are used by stakeholders to assess a company's environmental impact. Similar to how a doctor checks your health, an environmental audit checks the 'health' of a company's impact on the planet.

Students often think environmental audits are legally required and always objective, but actually they are often voluntary and can be used as a publicity stunt if not independently verified.

When assessing environmental audits, discuss their purpose (e.g., setting targets, influencing consumers) and limitations (e.g., voluntary nature, cost, potential for bias) and how their effectiveness depends on independent verification.

The growing importance of sustainability means businesses must consider their environmental impact. This includes managing pollution, waste, energy use, and resource depletion. Environmental audits provide a way to assess performance, though their voluntary nature can limit credibility. Stakeholders increasingly demand corporate social responsibility and genuine efforts towards protecting the environment for future generations.

When asked to 'evaluate' an external influence, always present a balanced argument. Discuss both the opportunities AND the threats it creates for the business.

Use a framework like PESTLE-C (Political, Economic, Social, Technological, Legal, Environmental, Competitive) to structure your analysis of the external environment, ensuring you don't miss key factors.

Always apply the influence to the specific business in the case study. For example, how does a new consumer protection law affect a car manufacturer differently from a software company?

For questions on multinationals, analyse the impact on the 'host country' by considering different stakeholders: local businesses, employees, the government, and the community.

When discussing CSR or environmental issues, move beyond simple descriptions. Analyse the potential conflict between ethical behaviour and the pursuit of profit for shareholders.

In your conclusion, make a justified judgement. For example, which external factor is the *most* significant threat and why? This demonstrates higher-level evaluation skills.

Advantages & Disadvantages

Privatisation

Nationalisation

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the key external influence in question and briefly outlining its relevance to business activity. State your overall argument or the main areas you will explore.

Conclusion

Summarise your main arguments without introducing new information. Make a clear, justified judgement about the overall impact or significance of the external influence, directly answering the question posed. Reinforce your evaluation by explaining *why* certain factors are more important than others.

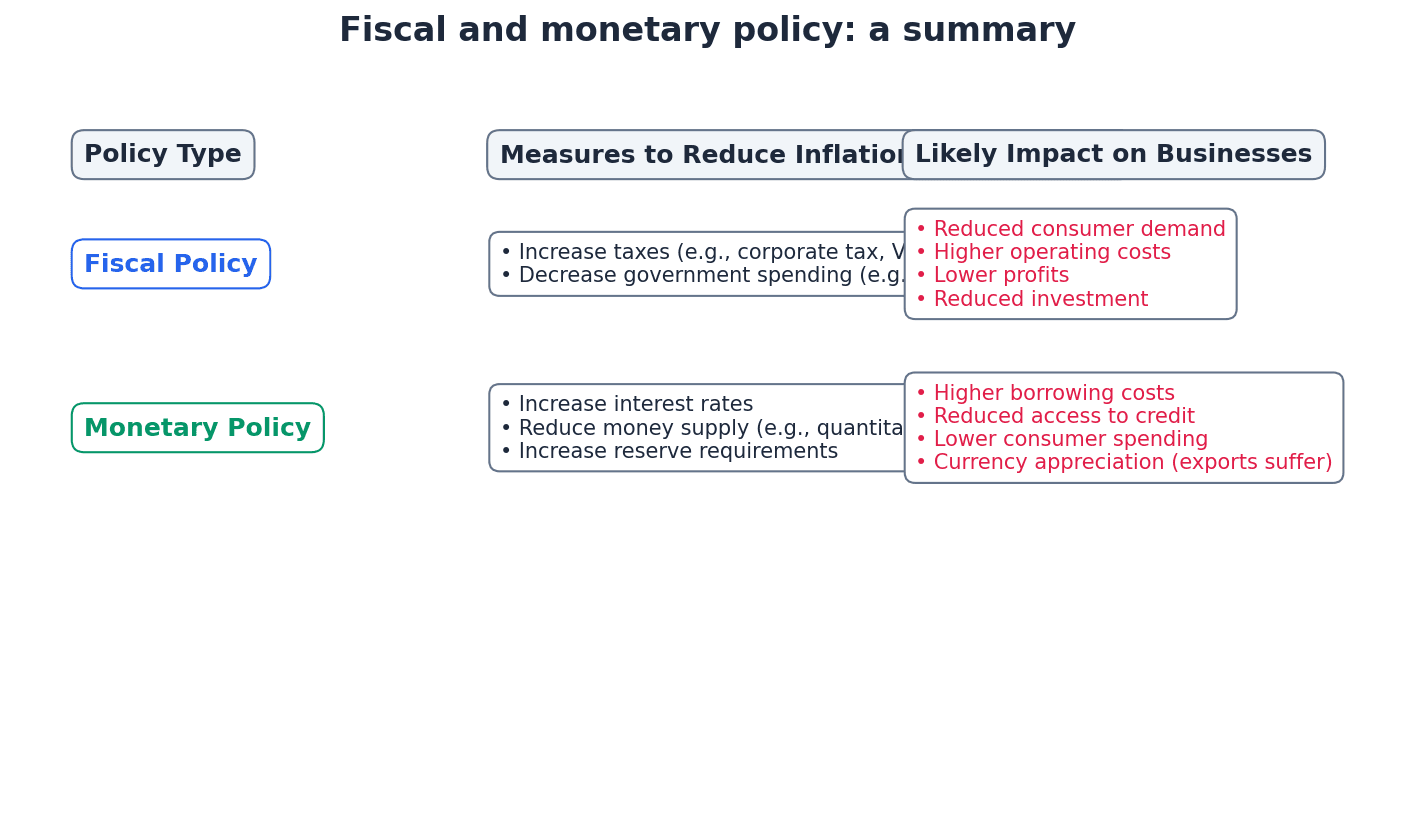

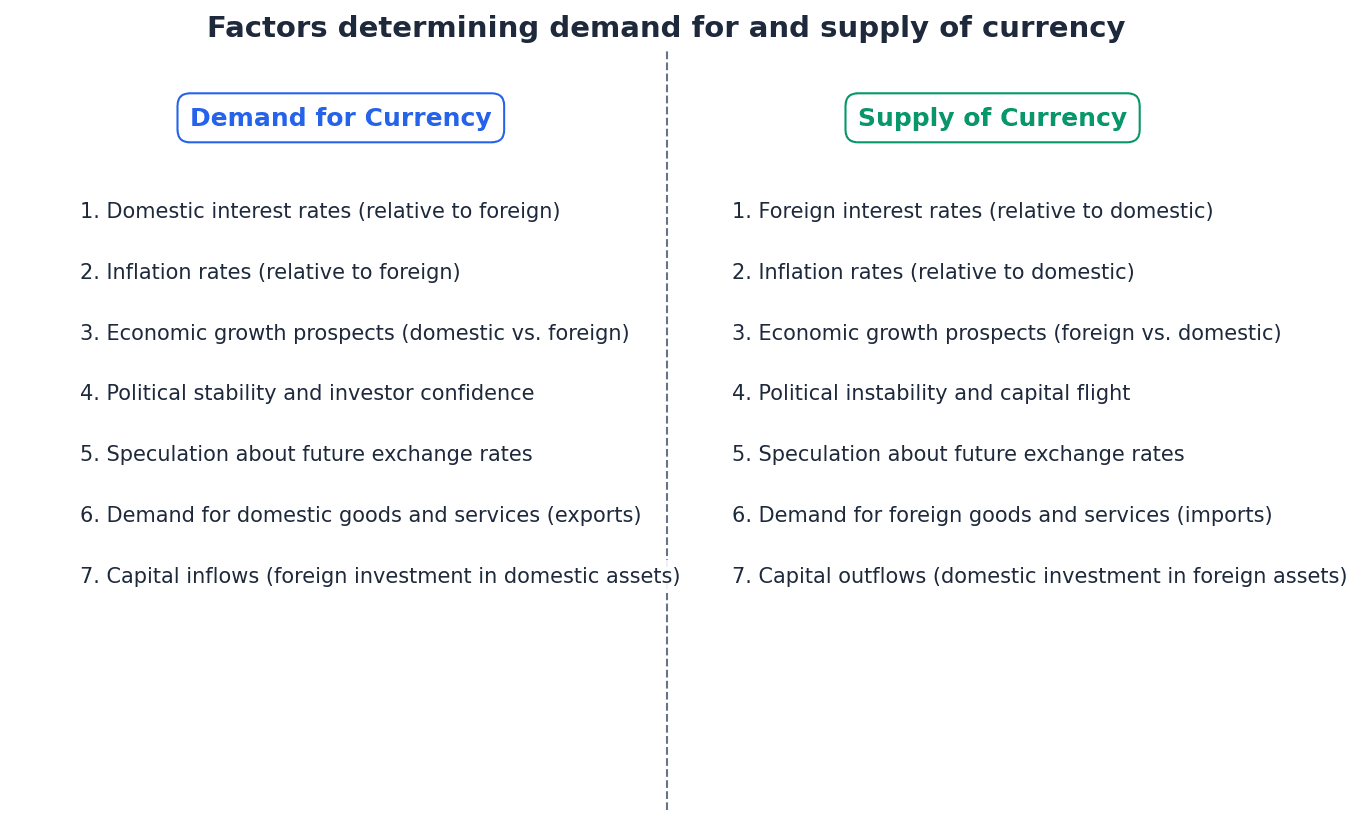

This chapter examines how external economic factors and government policies influence business operations. It covers government support, market failure, macroeconomic objectives like growth and inflation, and the impact of monetary, fiscal, supply-side, and exchange rate policies on business decisions.

market failure — Failure to allocate resources effectively is referred to as market failure.

Market failure occurs when the free market mechanism does not consider all costs, leading to an inefficient allocation of resources. For example, a shared kitchen where no one pays for cleaning supplies leads to a messy kitchen because the 'market' (cooking) fails to account for the 'external cost' (cleaning).

Students often confuse market failure with a business failing, but actually it refers to the market's inability to efficiently allocate resources, often due to external costs, public goods, or monopolies.

private costs — When a business makes a product, it must pay for the costs of the land, capital, labour and materials; these are called private costs.

Private costs are the direct costs incurred by a business in the production of goods or services, such as the ingredients for a cake, the oven, and the electricity bill for baking. These costs are typically reflected in a firm's accounting records and influence its pricing and output decisions.

Distinguish clearly between private costs and external costs when discussing market failure. An 'analysis' question might require you to explain how ignoring external costs leads to market failure.

monopoly — When a market is dominated by one supplier, a monopoly is said to exist.

A monopoly producer can restrict output and raise prices to maximise profits, leading to under-provision of products compared with demand. This is a form of market failure as it results in an inefficient allocation of resources and harms consumer welfare, much like being the only ice cream seller on a hot beach allows for very high prices.

macroeconomic objectives — All governments set targets for the whole economy and these are referred to as macroeconomic objectives.

These objectives typically include economic growth, low price inflation, low unemployment, a long-term balance of payments, and exchange rate stability. Governments use various policies to try and achieve these targets, guiding the entire economy towards desired outcomes like prosperity and stability.

Students often think all macroeconomic objectives can be achieved simultaneously, but actually there are often conflicts, such as between economic growth and low inflation.

economic growth — Economic growth is the annual percentage increase in a country’s total level of output – known as gross domestic product (GDP) – usually measured by changes in real GDP.

Economic growth signifies that a country is becoming richer, leading to higher living standards, increased employment, and more resources for public services. It is like a pie getting bigger each year, meaning the country's 'pie' of goods and services is expanding, so there's potentially more for everyone.

Students often think economic growth is always beneficial, but actually rapid growth can lead to negative externalities like increased pollution or job losses due to technological change.

gross domestic product (GDP) — Gross domestic product (GDP) is a country’s total level of output.

GDP is the total monetary value of all finished goods and services produced within a country's borders in a specific time period. Real GDP adjusts for inflation, providing a more accurate measure of economic growth, much like a total score a country gets for all the goods and services it produces in a year.

When discussing economic growth, specify 'real GDP' to indicate that inflation has been accounted for. Evaluate both the benefits and potential drawbacks, especially in relation to other macroeconomic objectives.

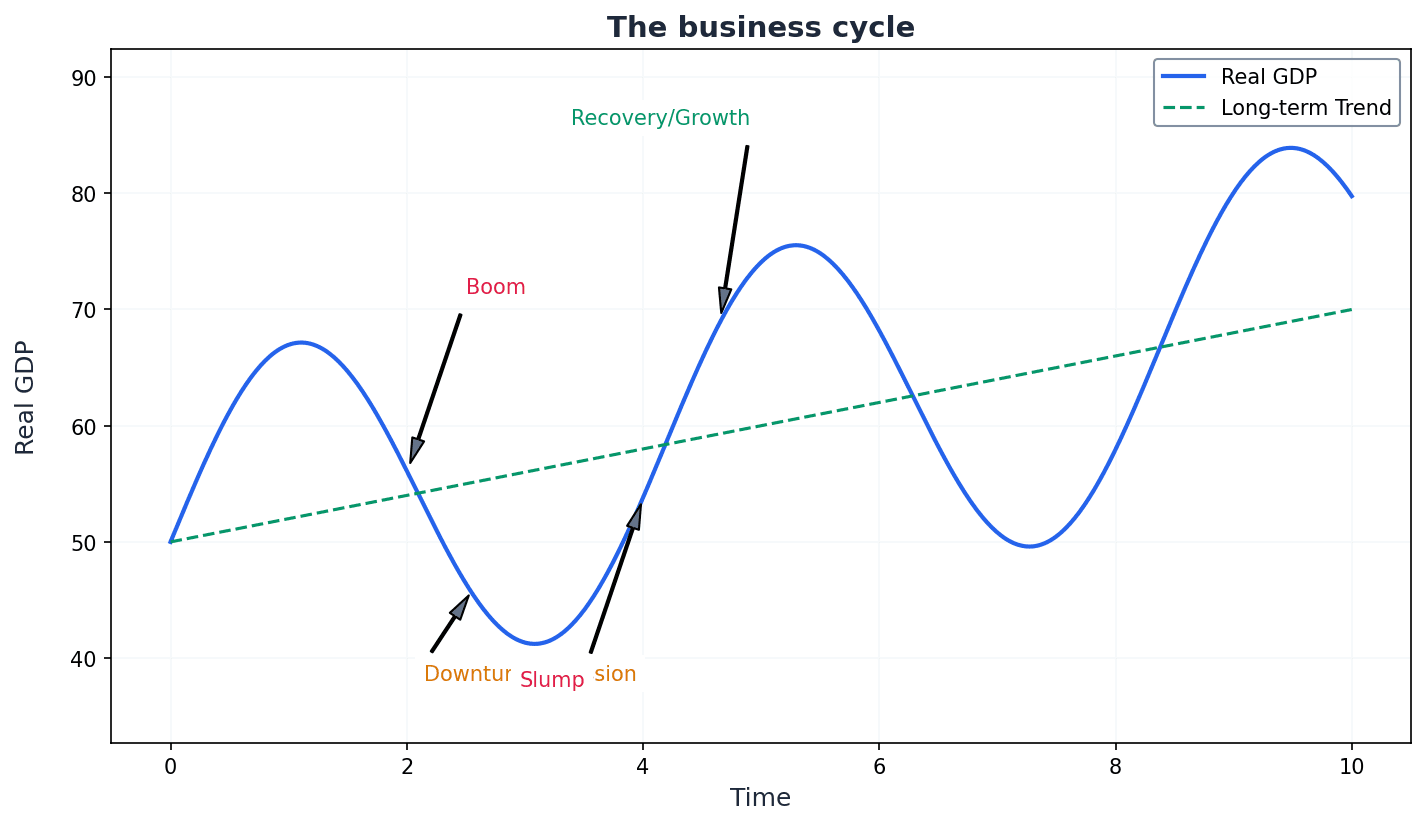

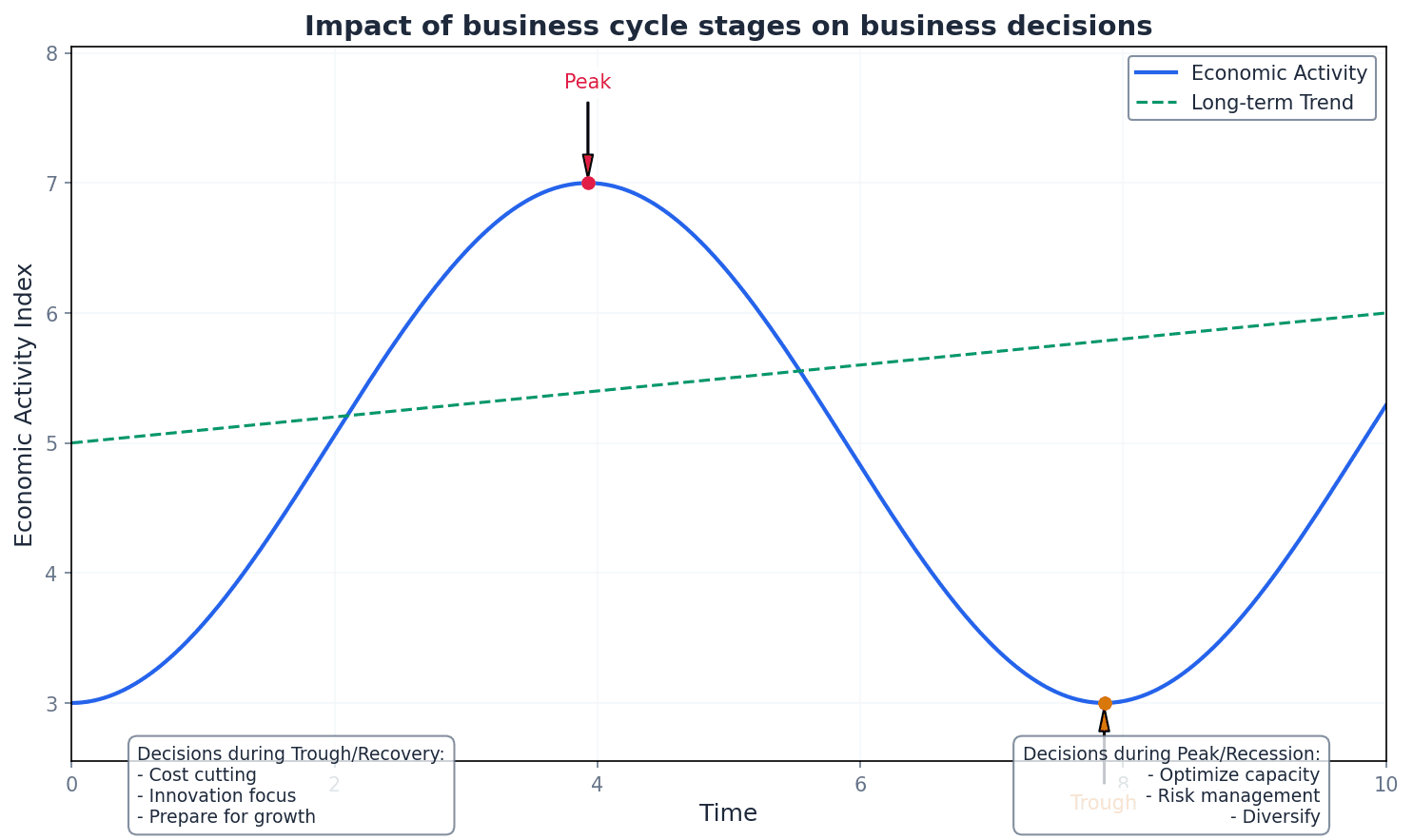

The business cycle describes the natural fluctuations in economic activity, moving through stages of boom, recession, slump, and recovery. Each stage has a distinct impact on business decisions regarding investment, employment, and pricing strategies. Businesses must adapt their strategies to these cyclical changes to remain competitive and profitable.

inflation — Inflation is the rate at which consumer prices, on average, increase each year.

Inflation means the spending power of money falls over time as goods and services become more expensive, like a balloon slowly expanding where the value of your money shrinks. It can be caused by cost-push factors (rising production costs) or demand-pull factors (excess consumer demand).

deflation — If one dollar buys more goods this year than it did last year, then the value of money has increased. This must have been caused by deflation.

Deflation is a sustained decrease in the general price level, meaning the spending power of money increases. While seemingly beneficial, it can lead to reduced demand as consumers delay purchases, lower profitability for businesses, and increased real value of debts, much like a shrinking balloon where your money buys more, but people might wait for prices to fall even further.

Students often think deflation is always good because prices are falling, but actually it can be very damaging to an economy by discouraging spending and investment, potentially leading to a recession.

When analysing inflation, distinguish between cost-push and demand-pull causes. Evaluate both the benefits of low inflation and the serious drawbacks of high inflation for businesses, including uncertainty and competitiveness.

cyclical unemployment — Cyclical unemployment is caused by falling demand for products during the recession stage of the business cycle.

During a recession, businesses produce fewer goods and services, leading to a reduced need for workers. This type of unemployment is directly linked to the overall economic downturn, similar to a restaurant needing fewer staff during a city-wide festival due to a temporary drop in customers.

Students often think all unemployment is due to a lack of skills, but actually cyclical unemployment is due to a lack of overall demand in the economy, not individual worker deficiencies.

structural unemployment — Structural unemployment results in certain types of workers being unable to find work, even though jobs could exist in expanding industries.

This occurs due to structural changes in the economy, such as shifts in consumer tastes or technological advancements replacing workers. Workers' skills may no longer match the available jobs, much like a blacksmith whose skills are obsolete in a world of mass-produced metal goods.

frictional unemployment — While workers are looking for other work, they are said to be frictionally unemployed.

This type of unemployment is short-term and occurs when workers are transitioning between jobs or entering the workforce for the first time. It is a natural feature of a dynamic labour market, like the brief period between finishing one TV series and finding a new one to watch.

When analysing unemployment, specify the type (cyclical, structural, frictional) as the impact and appropriate government response will differ.