Business · Enterprise

This chapter introduces the core concepts of business activity, including the purpose of businesses, the factors of production, and the crucial concept of adding value. It also explores the economic problem of scarcity and opportunity cost, and highlights the vital roles of entrepreneurs and intrapreneurs in driving economic development.

Business — A business is an organisation that uses resources to meet the needs of customers by providing a product or service that they demand.

Businesses are fundamental to economic activity, transforming scarce resources into goods and services that satisfy consumer needs. Their primary aim is often to add value and make a profit, contributing to a higher standard of living. Think of a baker: they take flour, water, and yeast (resources) and turn them into bread (a product) that customers want, adding value through their skill and effort.

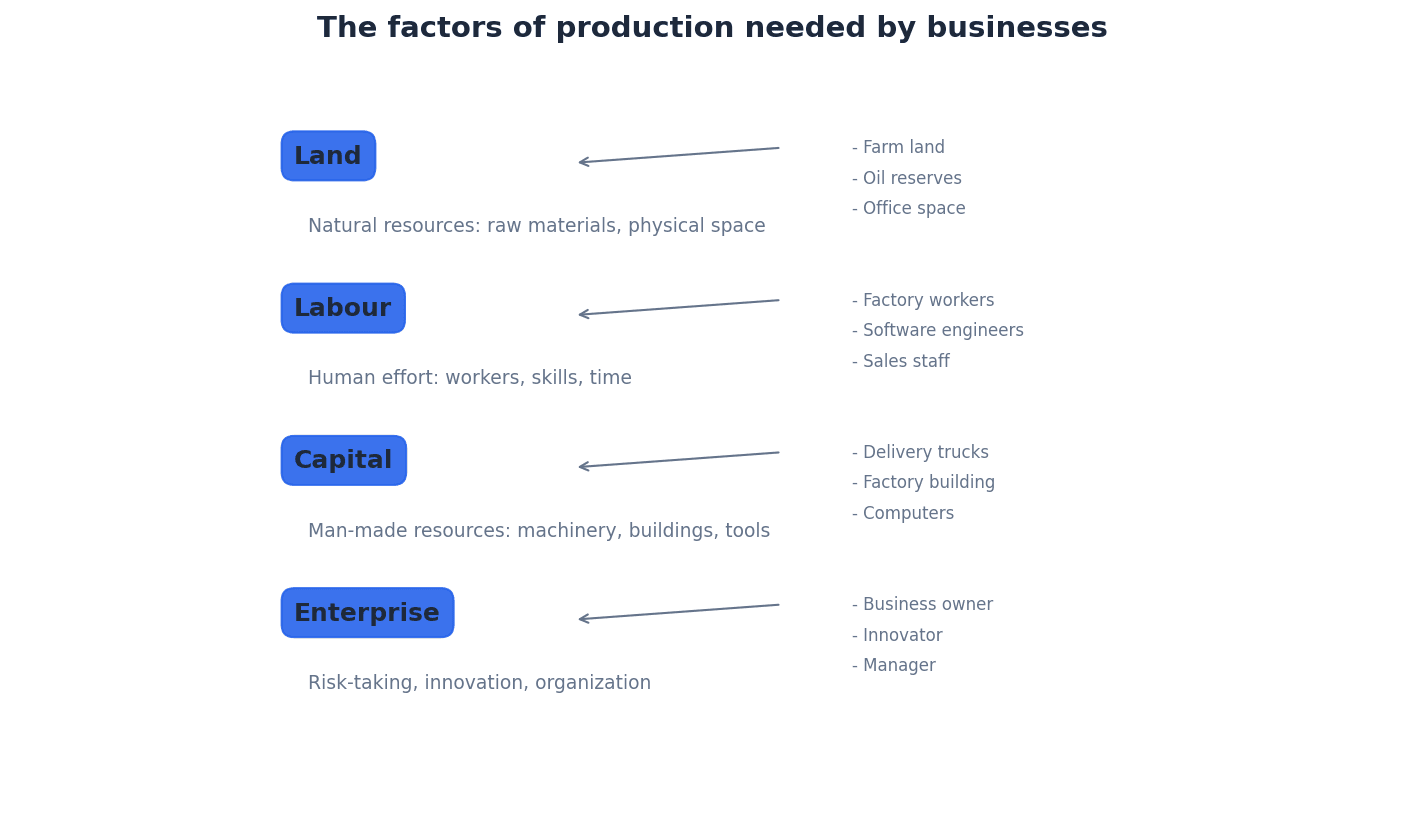

Factors of production — Factors of production are the resources needed by businesses to be able to operate and produce goods or services.

These four categories – land, labour, capital, and enterprise – are the fundamental building blocks for any economic activity. Their availability and efficient combination determine a business's capacity to produce. Imagine building a house: the land is where it stands, the builders are the labour, the tools and machinery are the capital, and the architect/project manager is the enterprise bringing it all together.

Be prepared to define and give examples for each of the four factors of production, as this is a common definitional question.

Land — Land is a general term that includes not only land itself but all the renewable and non-renewable resources of nature, such as coal, crude oil and timber.

This factor encompasses all natural resources, whether they are directly used as raw materials or provide the physical space for operations. Its scarcity is a core aspect of the economic problem. For a farmer, the land is the soil for crops, the water for irrigation, and even the sunlight that helps plants grow.

Students often think 'land' only refers to real estate, but actually it includes all natural resources, both above and below the surface.

Labour — Labour refers to the manual and skilled labour that make up the workforce of the business.

This factor represents the human effort, both physical and mental, applied in the production process. The quality and quantity of labour significantly impact a business's productivity and output. In a restaurant, the chefs, waiters, and cleaners all represent labour, each contributing their skills to the service.

Capital — Capital is not just the finance needed to set up a business and pay for its continuing operations, but also all the manufactured resources used in production, including capital goods such as computers, machines, factories, offices and vehicles.

Capital is crucial for enabling production, providing the tools and infrastructure necessary for businesses to operate efficiently. It represents accumulated wealth used to create more wealth. For a taxi company, the cars are capital goods, and the money used to buy them and pay for fuel is finance capital.

Students often think 'capital' only means money, but actually it also includes manufactured resources like machines and factories used in production.

Distinguish clearly between financial capital (money) and physical capital (capital goods) when discussing this factor of production.

Enterprise — Enterprise is the initiative and coordination provided by risk-taking individuals called entrepreneurs, who combine the other factors of production into a unit capable of producing goods and services.

Enterprise is the driving force behind business creation and innovation, involving the vision, risk-taking, and organisational skills needed to bring a business idea to fruition. It provides the managing, decision-making, and coordinating roles. The conductor of an orchestra is like enterprise, bringing together the musicians (labour), instruments (capital), and sheet music (land/resources) to create a performance.

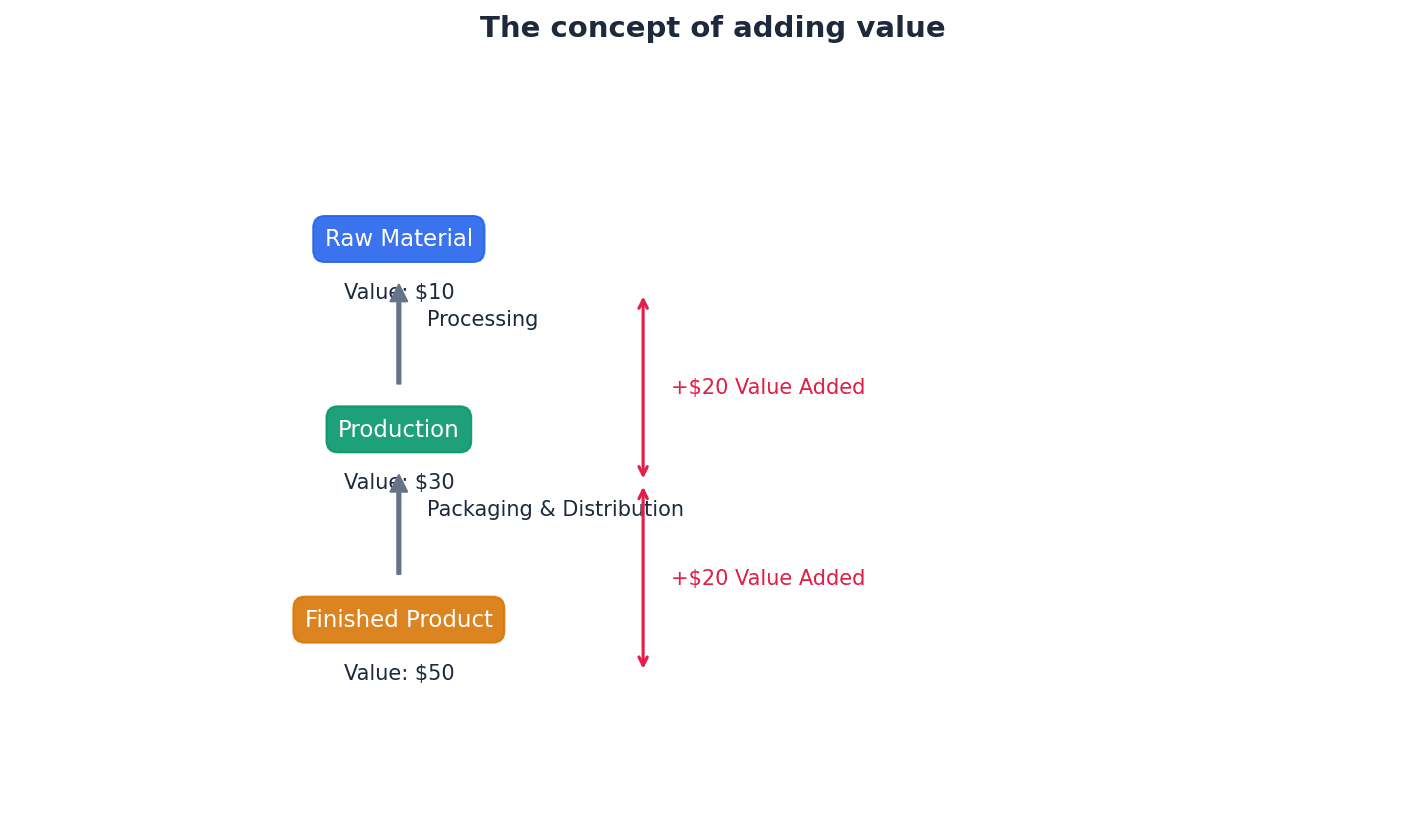

Added value — Added value is the difference between the selling price of the products sold by a business and the cost of the materials that it bought in.

Adding value is essential for a business's survival and profitability, as it allows the business to cover other costs (like labour and rent) and provide a return to investors. It reflects the perceived worth customers place on the transformed product or service. A coffee shop buys raw coffee beans for a low price, but after roasting, grinding, brewing, and serving it in a pleasant environment, the selling price of a cup of coffee is much higher, representing the added value.

Students often think added value is the same as profit, but actually profit is what remains after all costs, including labour and overheads, have been deducted from added value.

When asked to explain 'adding value', clearly state it's the difference between selling price and bought-in material costs, and explain its importance for covering other expenses and generating profit.

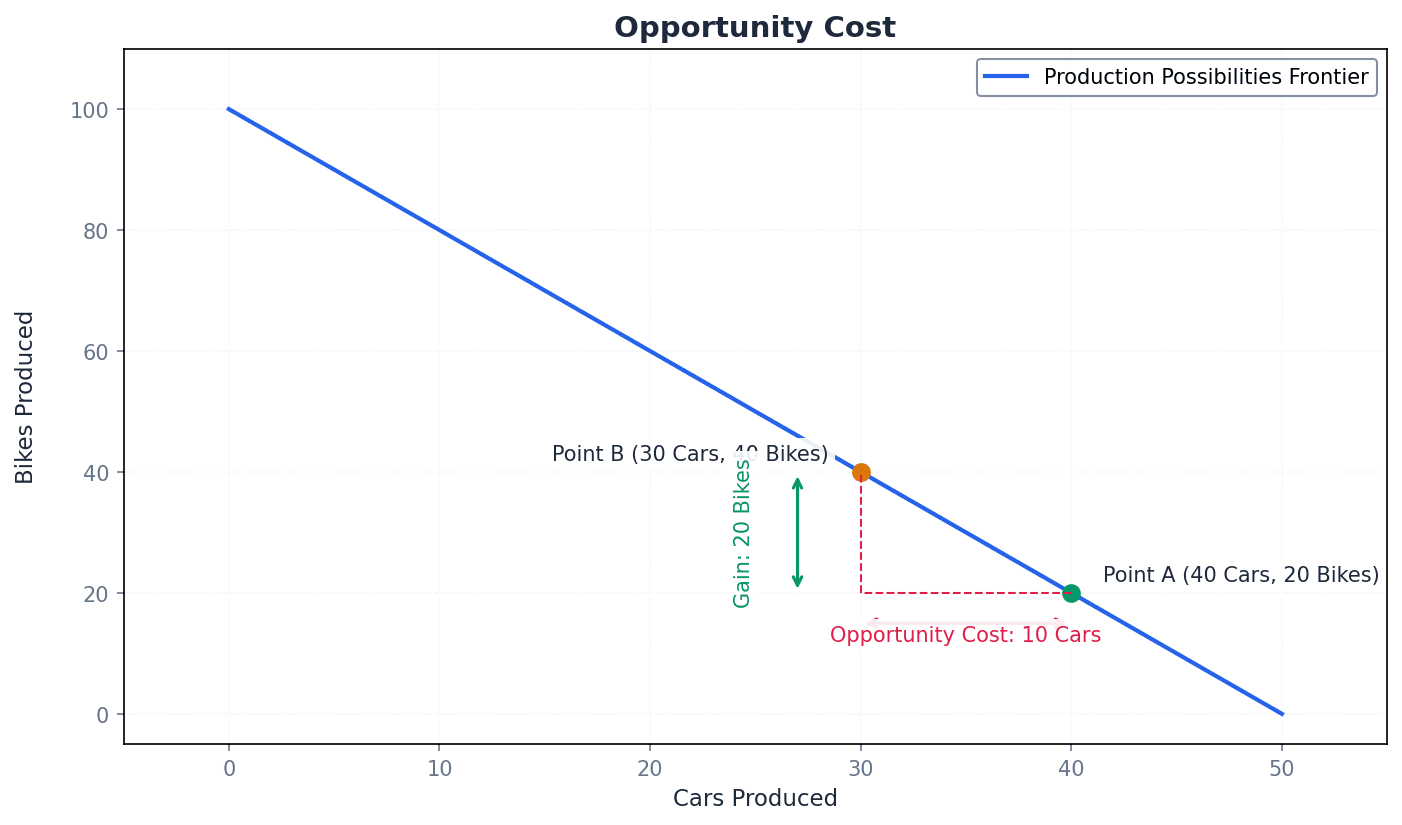

Economic problem — The economic problem is the situation where there are insufficient goods to satisfy all of our needs and wants at any one time.

This fundamental problem arises from the scarcity of resources relative to unlimited human wants. It forces individuals, businesses, and governments to make choices about how to allocate resources. Imagine having a limited budget for groceries but wanting to buy everything in the supermarket; you can't, so you have to choose what's most important.

Ensure your explanation of the economic problem links scarcity of resources to the inability to satisfy all needs and wants, leading to the necessity of choice.

Opportunity cost — Opportunity cost is the next most desired product which is given up when deciding to purchase or obtain one item over others.

This concept highlights the trade-offs inherent in all economic decisions. Every choice made means foregoing the benefits of the next best alternative, which is the true cost of that decision. If you choose to spend your Saturday studying for an exam, the opportunity cost might be going to a concert with friends, which was your next best alternative.

Students often think opportunity cost is all the things given up, but actually it is only the single next best alternative that is foregone.

When explaining opportunity cost, clearly identify the choice made and the single best alternative that was sacrificed as a direct result of that choice.

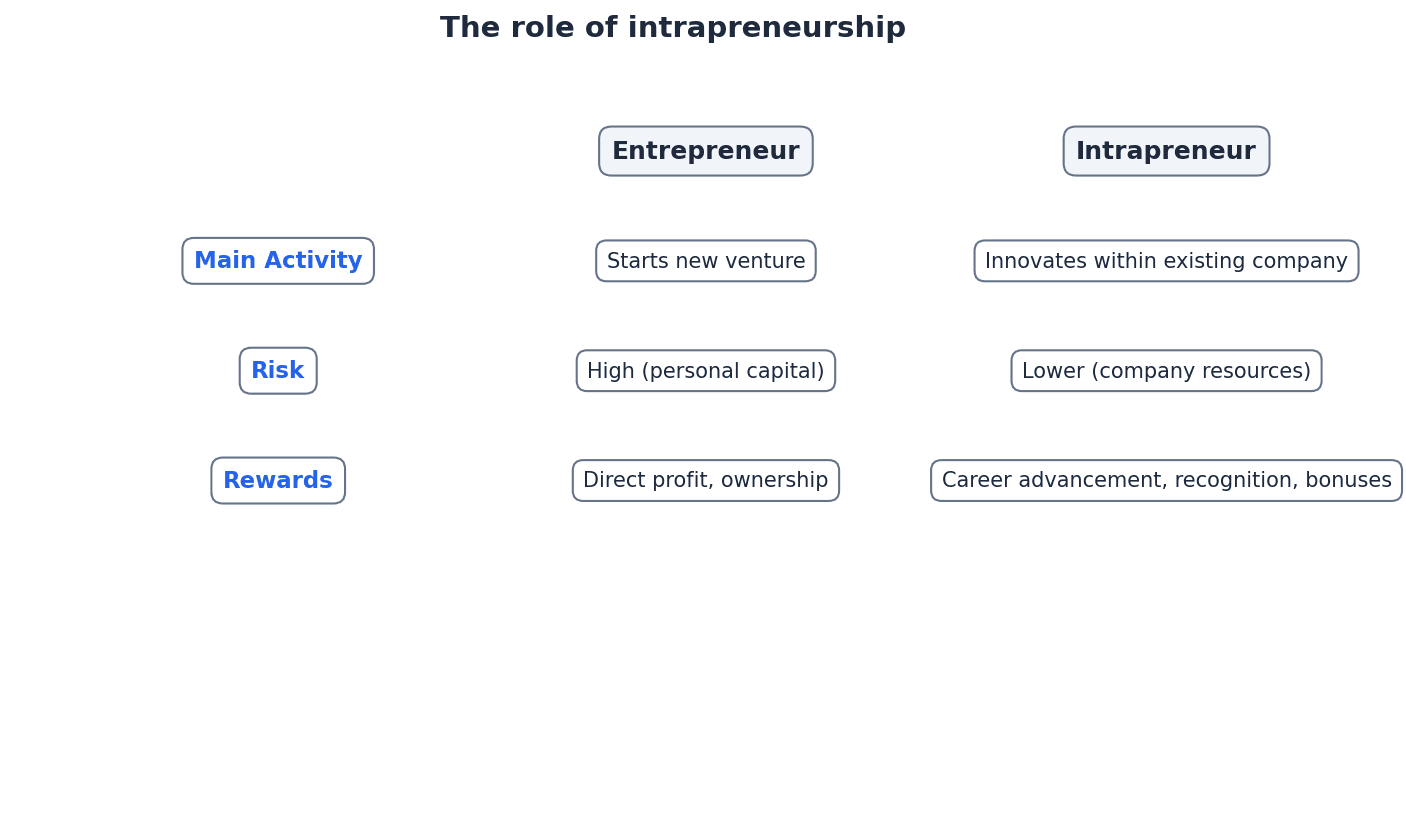

Entrepreneur — An entrepreneur is a risk-taking individual who combines the other factors of production into a unit capable of producing goods and services, providing the managing, decision-making and coordinating roles.

Entrepreneurs are central to economic development, identifying market gaps, innovating, and taking personal and financial risks to create new businesses. Their qualities include innovation, commitment, multi-skilling, leadership, self-confidence, and risk-taking. A chef who decides to open their own restaurant, investing their savings, hiring staff, designing the menu, and managing daily operations, is an entrepreneur.

When analysing entrepreneurs, focus on their personal qualities (e.g., risk-taking, innovation) and their role in combining factors of production and managing the business.

Entrepreneurs and their enterprise are vital for a country's economic development. They drive innovation, create new businesses, generate employment opportunities, and contribute to tax revenues. This leads to increased competition, a wider variety of goods and services, and ultimately a higher standard of living for the population. However, entrepreneurs often face barriers such as obtaining sufficient capital, finding good locations, intense competition, and managing business risk and uncertainty.

Intrapreneur — An intrapreneur is a person who has the same qualities as entrepreneurs and is encouraged to demonstrate the same skills as entrepreneurs within an existing business.

Intrapreneurs drive innovation and change from within established organisations, helping businesses adapt to dynamic environments and retain creative talent. They take risks on behalf of the company, not personally. An employee at a large tech company who develops a new product feature or service idea, champions it, and brings it to market using company resources, is an intrapreneur.

Distinguish intrapreneurs from entrepreneurs by highlighting that intrapreneurs operate within an existing business, with the business taking the risk and receiving the rewards.

Business plan — A business plan is a detailed document outlining a new business's strategies, operations, marketing, management team, and financial forecasts.

It serves as a roadmap for the business and a crucial tool for attracting finance from investors and lenders. While beneficial for planning, it can also create a false sense of certainty or lead to inflexibility if not adapted to a dynamic environment. Think of a business plan as a detailed blueprint for building a house; it shows what you intend to build, how you'll build it, who will help, and how much it will cost, to convince a bank to lend you money.

Students often think a business plan guarantees success, but actually it's a forecast and a guide, and external factors can still lead to failure if the plan isn't flexible.

When evaluating business plans, discuss both their benefits (e.g., securing finance, clear direction) and limitations (e.g., inflexibility, based on forecasts).

Always evaluate. When asked about business plans, discuss both their benefits (e.g., securing finance) and limitations (e.g., can be rigid).

Advantages

Disadvantages

Advantages

Disadvantages

Advantages

Disadvantages

For 12+ mark questions, always evaluate both sides before reaching a judgement.

Adapt these for any 12+ mark question on this topic

Examiner tips

Introduction

Start by defining key terms relevant to the question (e.g., entrepreneur, economic development, business plan). Briefly outline the main arguments you will present.

Main Body

Evaluation

For evaluation, consider the context. For example, 'However, the extent of an entrepreneur's contribution to economic development depends on the scale of their business and the sector they operate in.' Or, 'The effectiveness of a business plan is ultimately limited by the dynamic nature of the market and the entrepreneur's ability to adapt.'

Conclusion

Summarise your main arguments and provide a final, reasoned judgment that directly answers the question. Avoid introducing new information. Emphasise the overall significance of enterprise and planning while acknowledging their complexities.