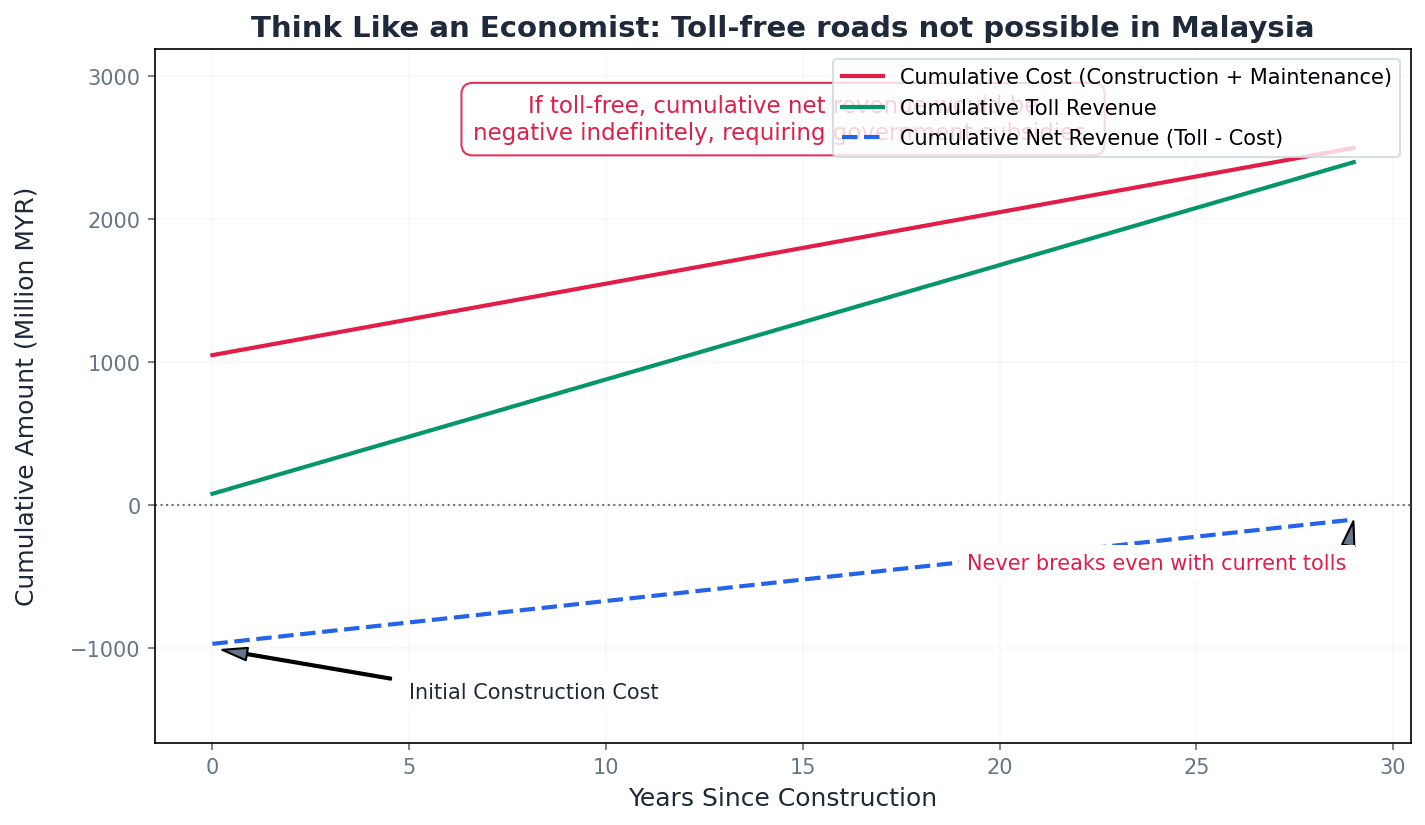

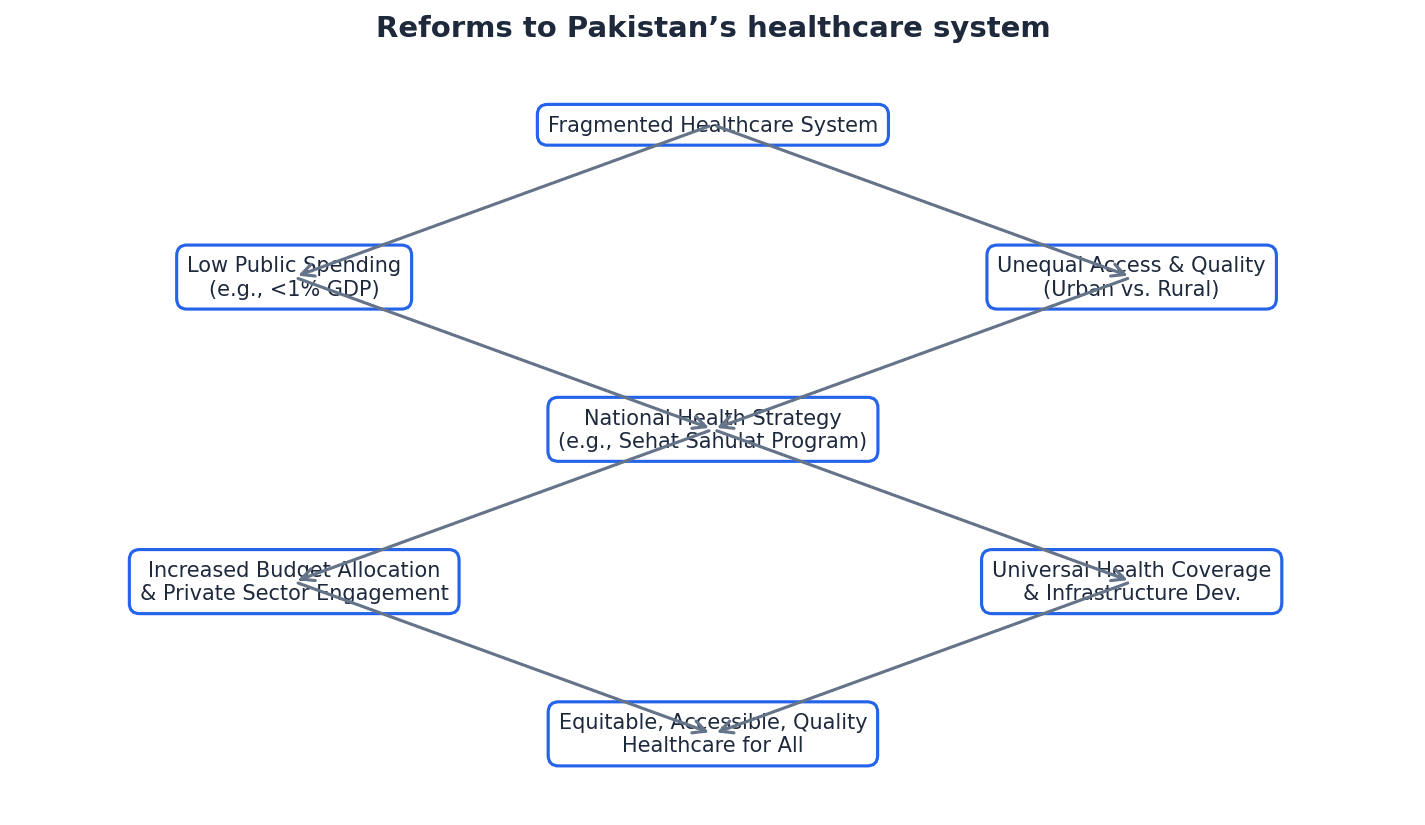

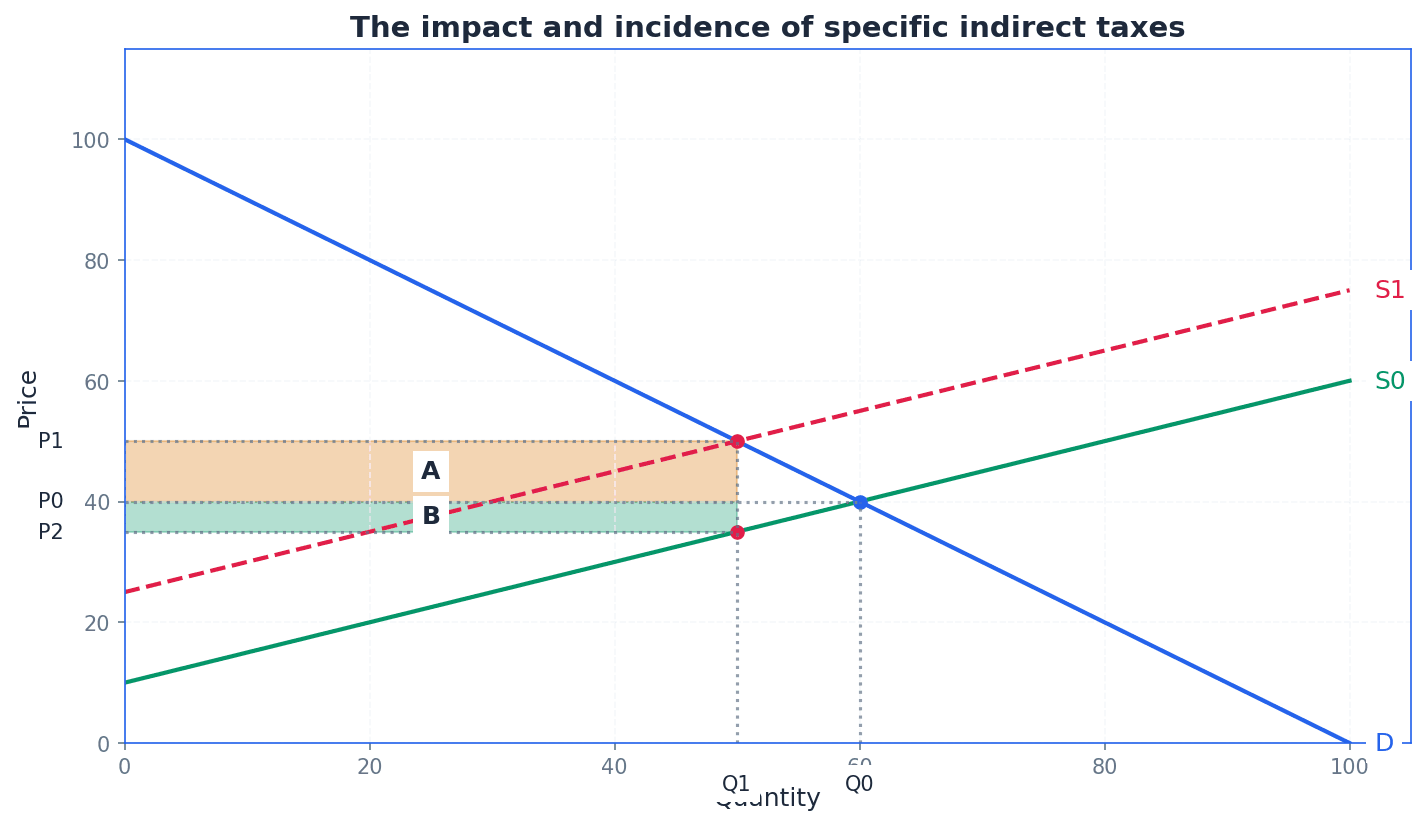

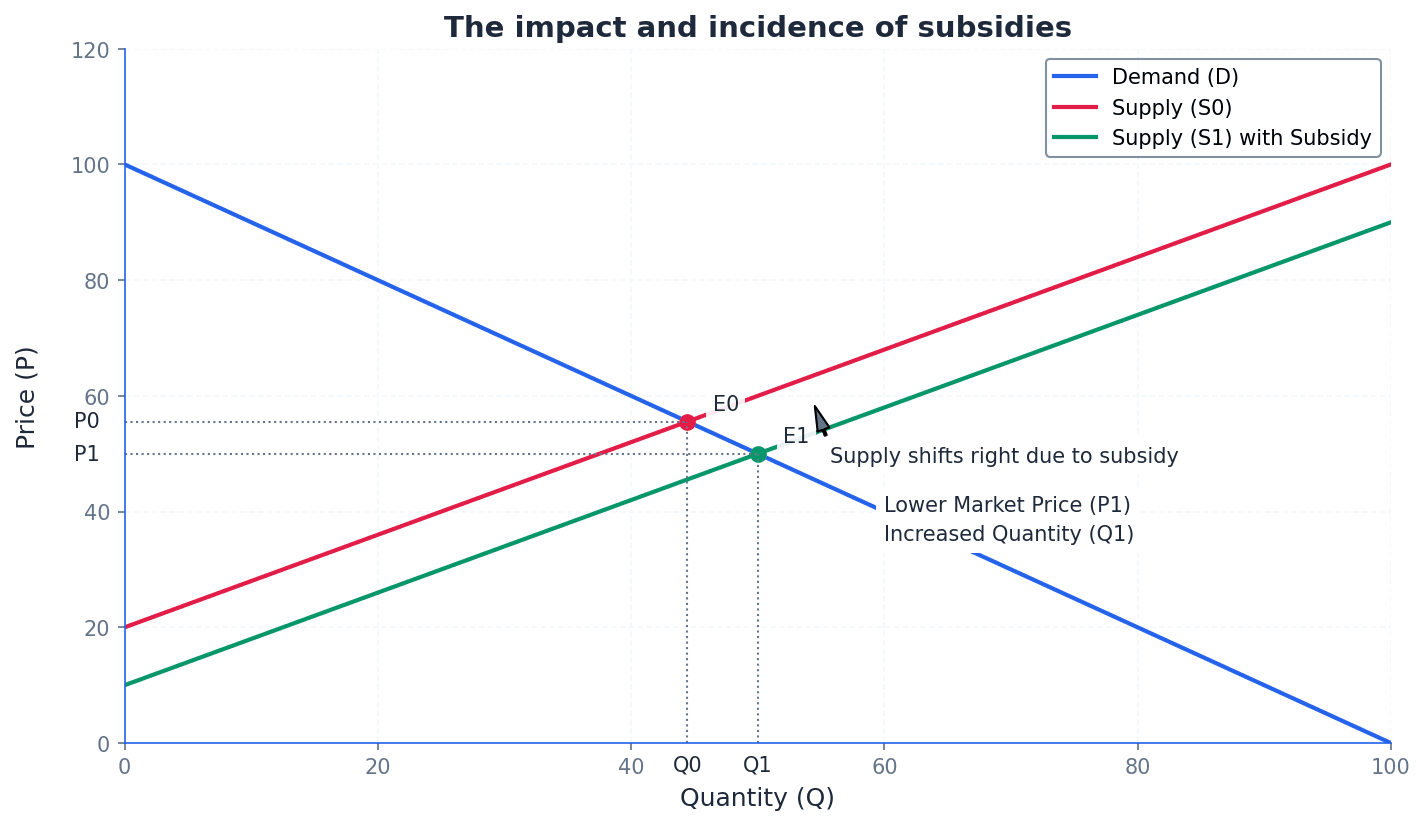

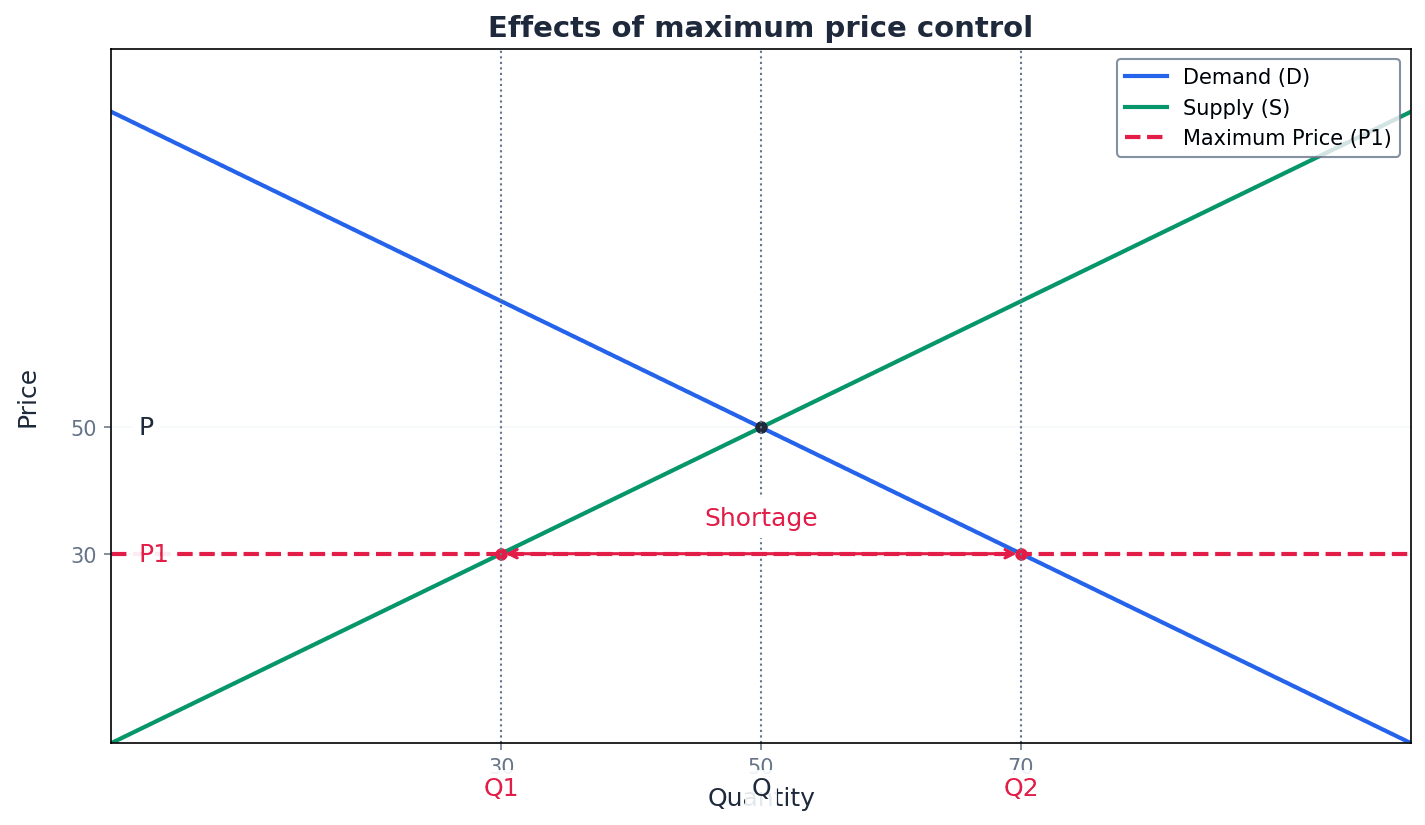

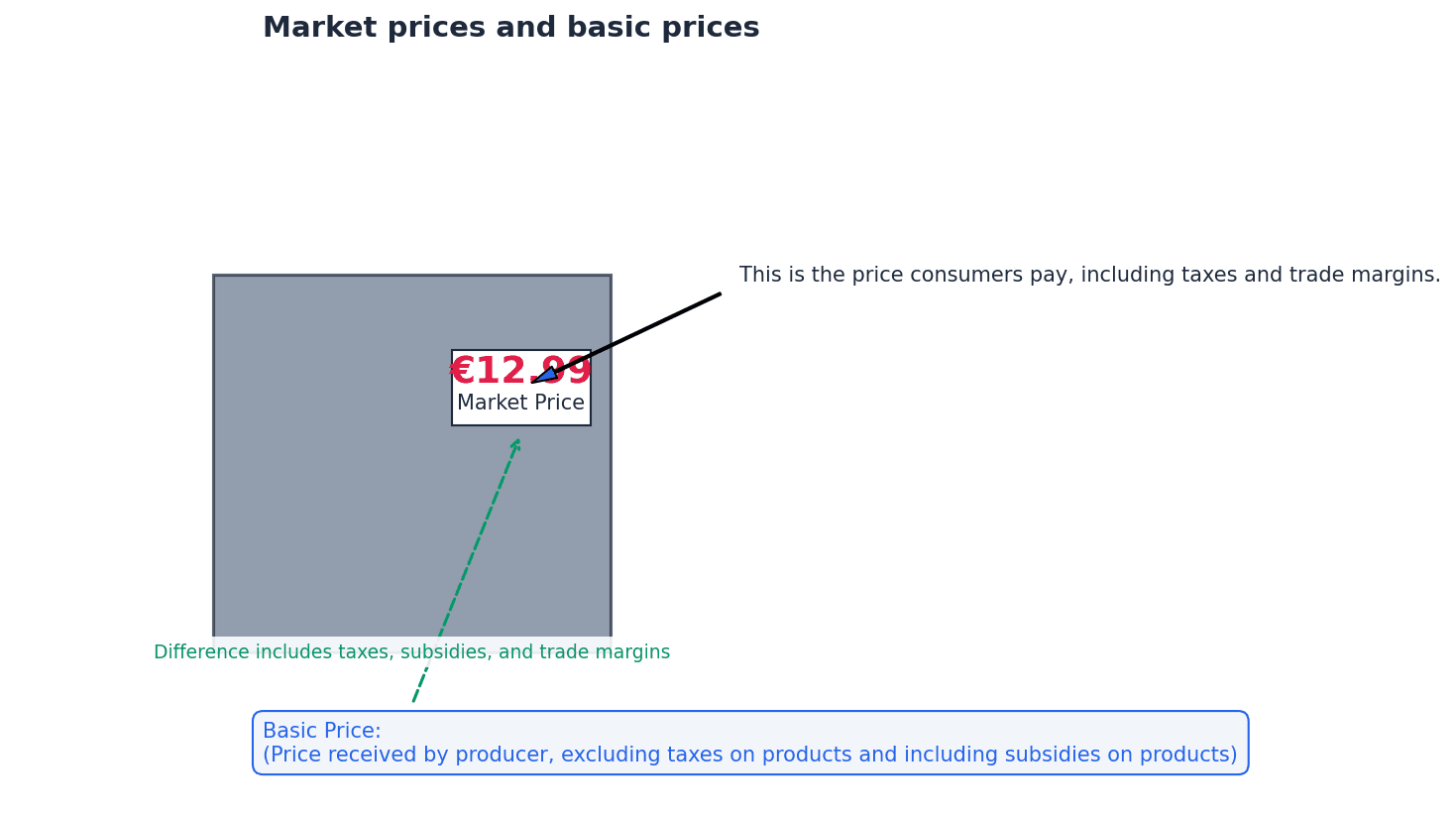

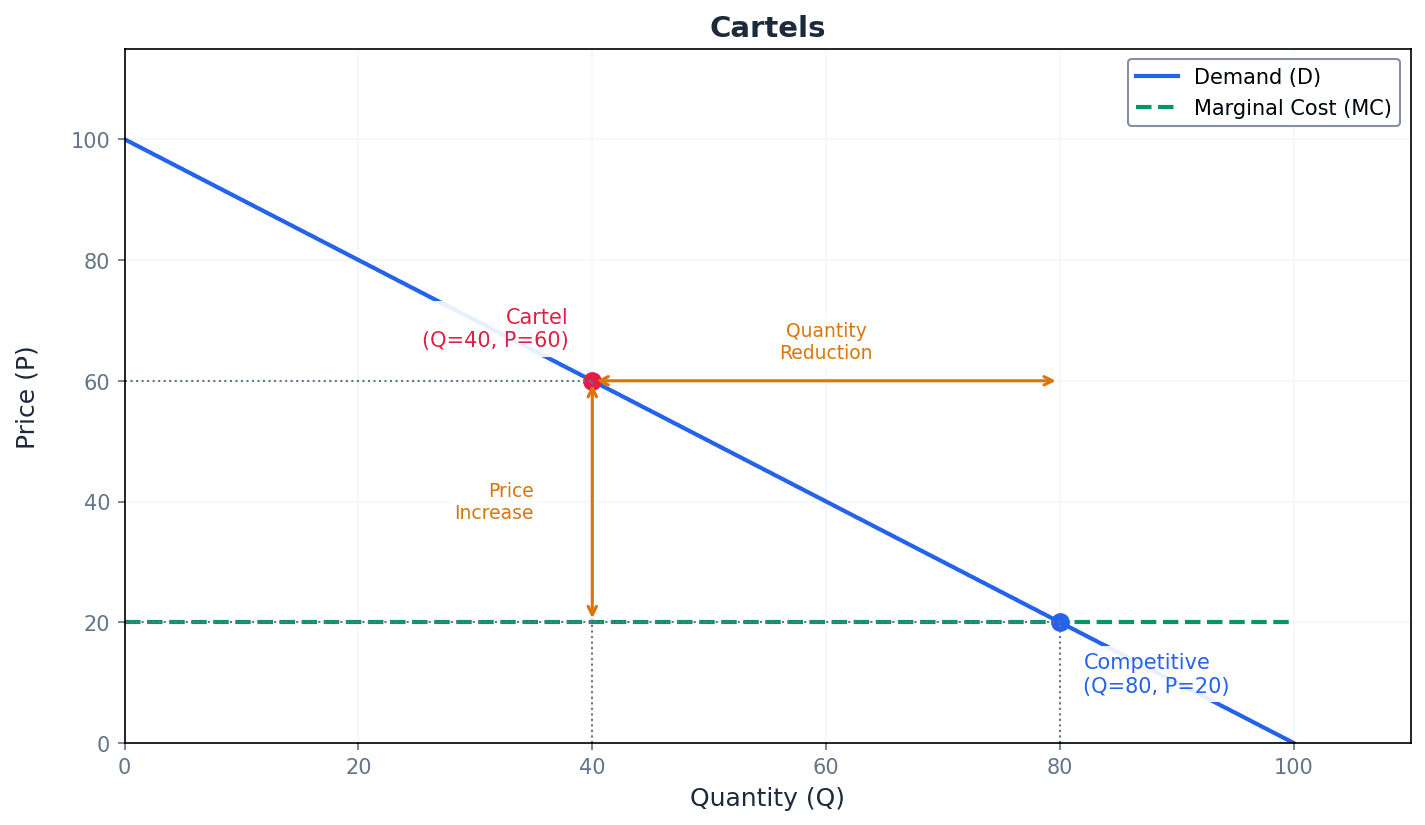

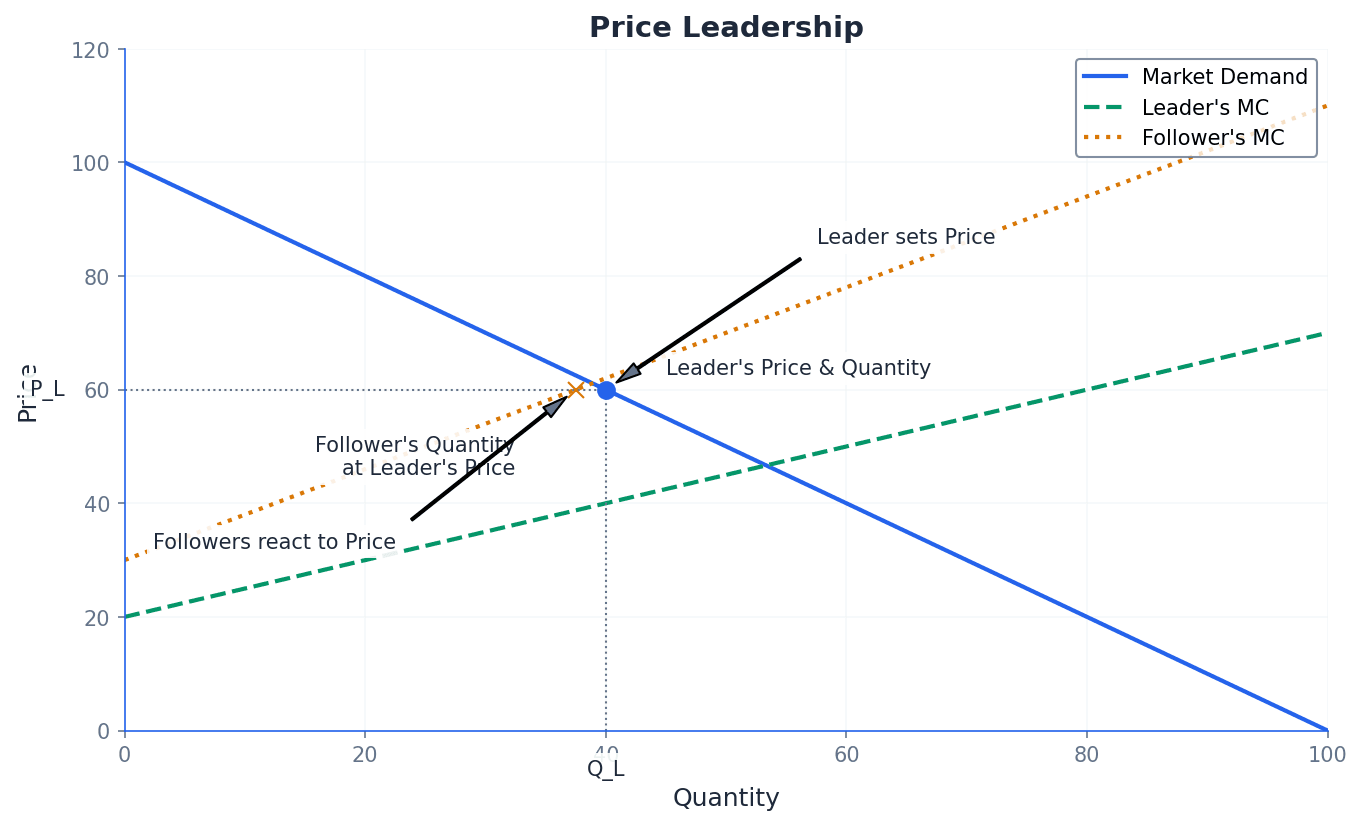

Nexelia Academy · Official Revision Notes

Complete A-Level revision notes · 54 chapters

This chapter introduces the fundamental economic problem of scarcity, which arises because human wants are unlimited while resources are limited. This necessitates individuals, firms, and governments to make choices, leading to the concept of opportunity cost, defined as the next best alternative foregone. All economies must address three basic questions of resource allocation: what to produce, how to produce, and for whom to produce.

Resources — Inputs used to produce goods and services.

These are the factors of production available in an economy, such as land, labour, capital, and enterprise. Resources are finite, meaning there is a limited supply of them, which contributes to the fundamental economic problem. Think of resources like the ingredients in a kitchen; you only have a certain amount of flour, sugar, and eggs, so you can't bake every cake you want simultaneously.

Students often think resources are just money, but actually resources include all inputs like raw materials, labour, and machinery.

Needs — Things like food, shelter and clothing that are needed for survival.

Needs are basic requirements for human existence, forming the foundation of an individual's scale of preference. While essential, even needs can be satisfied in various ways, leading to choices. Needs are like the basic functions of a smartphone – calling, texting, internet access – without which it wouldn't be a phone.

Wants — Things that people desire, which are always likely to be something else whatever their income.

Wants are unlimited and continually expanding, developing, and changing, driven by factors like culture, upbringing, life experiences, and observing others. They are distinct from needs, which are essential for survival. Imagine a child in a toy store; they always want the next new toy, even after getting one. This endless desire for more is what economists mean by unlimited wants.

Students often confuse wants with needs, but needs are essential for survival while wants are desires that improve quality of life.

Clearly distinguish between 'wants' and 'needs' in your answers; using them interchangeably will lose marks as they have distinct economic meanings.

Scarcity — The fundamental economic problem that arises because resources are scarce while people’s wants are unlimited.

Scarcity means that society does not have enough resources to produce all the goods and services necessary to satisfy everyone's wants. This necessitates making choices about how to allocate limited resources. If you have a small garden plot (limited resources) but want to grow every type of fruit, vegetable, and flower imaginable (unlimited wants), you face scarcity and must choose what to plant.

Students often think scarcity means there is simply not enough of something, but it specifically means there isn't enough to satisfy all human wants.

When defining scarcity, always include both 'limited resources' and 'unlimited wants' to demonstrate a complete understanding of the concept.

The fundamental economic problem stems from the reality that human wants are unlimited, while the resources available to satisfy these wants are limited. This inherent imbalance, known as scarcity, forces all economic agents – individuals, firms, and governments – to make choices about how to allocate their finite resources. Understanding why scarcity occurs is crucial to comprehending economic decision-making.

Choice — Taking decisions on how to allocate scarce resources between many competing uses.

Because resources are scarce and wants are unlimited, individuals, firms, and governments must make choices about which wants to satisfy. Every choice made implies foregoing other alternatives. Choosing what to watch on TV when there are many channels available means you are making a choice, and you cannot watch all shows simultaneously.

Students often think choice is simply picking something, but actually in economics, choice always implies a trade-off due to scarcity.

Opportunity cost — The cost of the choice in terms of the next best alternative.

Whenever a choice is made between alternatives due to scarcity, the opportunity cost is what is given up. It represents the real cost of a decision and is a recurring theme in economics. If you choose to spend your Saturday studying for an exam, the opportunity cost is the next best thing you could have done, like going to a football game with friends.

Students often think opportunity cost is all the alternatives foregone, but it is only the single next best alternative that is given up.

When calculating or identifying opportunity cost, ensure you specify the *next best* alternative, not just any alternative, to earn full marks.

The necessity of making choices due to scarcity directly leads to the concept of opportunity cost. Since resources are limited, satisfying one want means that another cannot be satisfied. The opportunity cost is the value of the next best alternative that is foregone when a choice is made. This concept applies to individuals, firms, and governments alike, as they all face resource constraints.

Scale of preference — Each individual’s scale of preference is a product of a set of influences, including culture, upbringing and life experiences, on which you place your more urgent wants at the top and the less urgent ones at the bottom.

This concept highlights that individuals prioritize their wants based on personal factors, leading to variations in what is considered essential or luxury. It explains why choices differ between people and how these preferences can evolve over time. Imagine making a shopping list for a limited budget. You'd put the absolute necessities like milk and bread at the top, and then less urgent items like a new gadget further down. Your friend's list might be completely different based on their own priorities.

Students often think everyone has the same scale of preference, but it is highly individual and influenced by personal circumstances and experiences.

Given the fundamental economic problem of scarcity, all economies, regardless of their structure, must answer three basic questions regarding the allocation of their limited resources. These questions are: What to produce? How to produce? and For whom to produce? The answers to these questions determine how a society addresses its economic challenges and satisfies its wants.

This question addresses which goods and services an economy will prioritize producing from its limited resources. Societies must decide between, for example, producing more consumer goods or more capital goods, or between public services like healthcare and private goods. These decisions reflect the collective choices and priorities of a society, often influenced by individual scales of preference.

This question concerns the methods and techniques used to produce the chosen goods and services. It involves decisions about the combination of resources (land, labour, capital, enterprise) to employ, the level of technology, and the organization of production. For instance, a society might choose between labour-intensive or capital-intensive production methods, considering efficiency and resource availability.

This question addresses how the goods and services produced will be distributed among the population. It involves decisions about income distribution, access to goods and services, and social equity. Societies must determine who benefits from production, whether it's based on income, need, or other criteria, which has significant implications for social welfare and economic equality.

Link 'choice' directly to 'scarcity' and 'opportunity cost' in your explanations, as these concepts are fundamentally interconnected.

When discussing basic economic problems, ensure you highlight that even after needs are met, wants remain unlimited, driving the problem of scarcity.

In case studies, actively look for examples of scarcity, the choices being made, and the resulting opportunity costs.

Advantages & Disadvantages

Unlimited Wants

Scarcity

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the fundamental economic problem of scarcity, linking it to unlimited wants and limited resources. State that this problem necessitates choices and leads to opportunity cost, and that all economies must answer three basic questions.

Conclusion

Summarize the interconnectedness of scarcity, choice, and opportunity cost as core economic principles. Reiterate that these concepts are central to understanding how economies function and allocate resources.

This chapter introduces economic methodology, explaining why economics is considered a social science due to its study of human behavior and use of scientific processes. It differentiates between positive statements (factual and testable) and normative statements (subjective and value-based), and discusses key analytical tools like ceteris paribus and the importance of different time periods for economic analysis.

Economics is considered a social science because it studies human behavior and uses scientific processes to develop models. This approach allows economists to analyze how individuals and societies make choices in the face of scarcity, applying systematic methods to understand complex interactions.

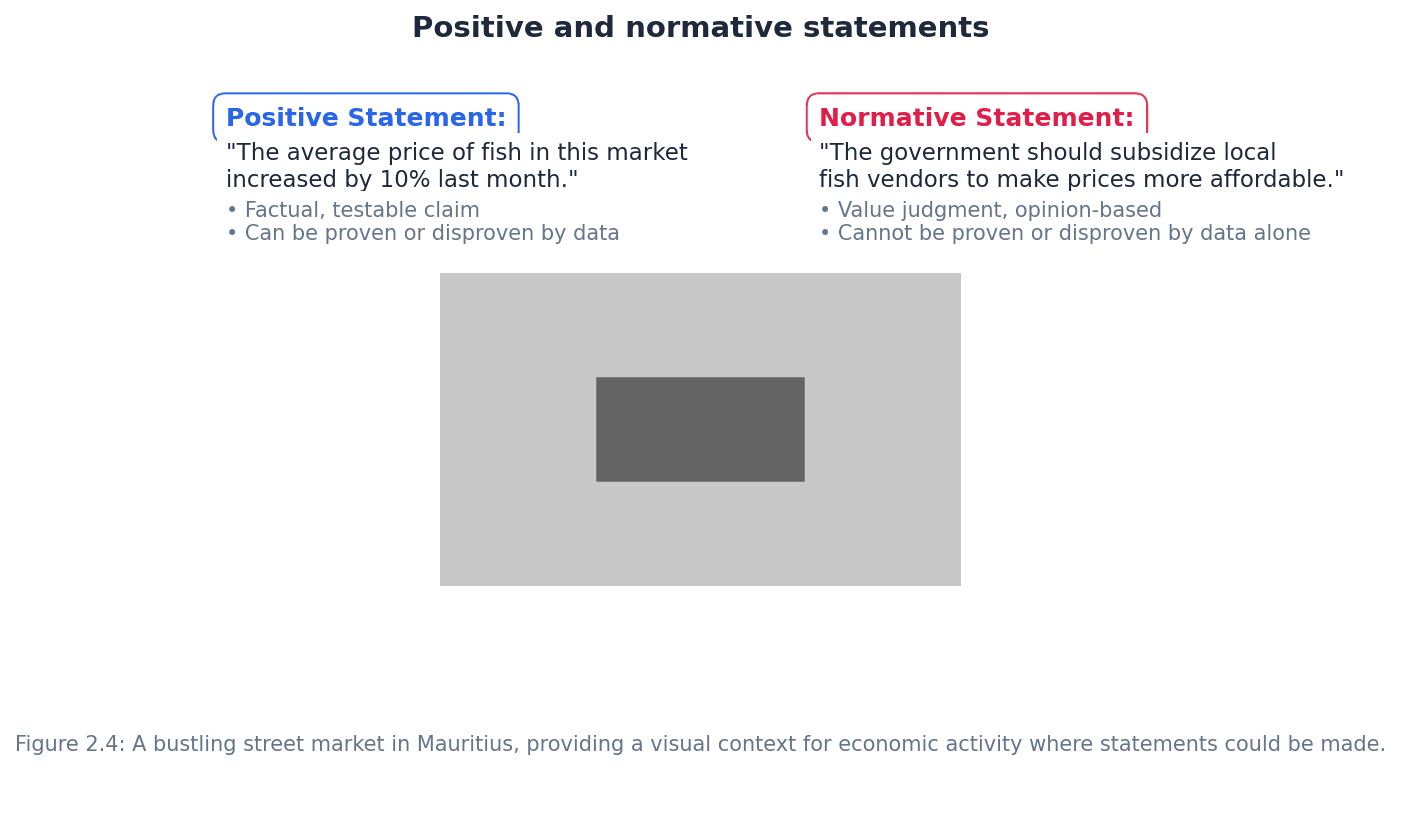

Positive statements — Statements that refer to what will happen, based on actual evidence or observation, without giving an opinion or making a value judgement.

These statements are objective and can be tested or verified against facts. They describe economic phenomena as they are or as they are predicted to be, allowing economists to analyze cause-and-effect relationships. For example, saying 'If you drop a ball, it will fall to the ground' is a positive statement in physics, as it describes an observable fact without personal opinion.

Students often think positive statements are always true, but actually they are statements that can be tested for truth or falsity using evidence, even if they turn out to be false.

When asked to identify or formulate a positive statement, ensure it is purely factual or testable, avoiding words like 'should', 'ought', 'best', or 'worst'.

Normative statements — Statements that express an opinion or make a value judgement within their analysis, and therefore can no longer be proven.

These statements are subjective and reflect personal beliefs or ethical positions. They often involve recommendations or evaluations of what 'should' be, rather than what 'is'. For instance, saying 'The government should increase taxes on sugary drinks to improve public health' is a normative statement, as it expresses an opinion about what ought to be done.

Students often think normative statements are simply 'wrong' or 'bad' statements, but actually they are statements that cannot be proven or disproven by facts alone because they contain a value judgement.

Look for keywords such as 'should', 'ought to', 'best', 'worst', 'good', 'bad', 'fair', or 'unfair' to identify normative statements in exam questions. When converting normative to positive, remove these subjective terms.

Ceteris paribus — A Latin term widely used by economists to refer to a situation where ‘other things remain equal’ or are unchanged.

This assumption allows economists to isolate the effect of a single variable on an outcome, simplifying complex situations for analysis. By holding all other factors constant, the impact of one specific change can be modeled and understood. Imagine testing how a car's speed changes with engine power; ceteris paribus means you assume road conditions, tire pressure, and wind resistance all stay the same, so you can focus only on the engine's effect.

Students often think ceteris paribus means all other factors are irrelevant, but actually it means those factors are temporarily assumed constant for analytical purposes, even though they might change in reality.

Always include 'ceteris paribus' in your explanations when discussing the effect of a single variable change (e.g., price on demand) to demonstrate a clear understanding of economic modeling assumptions. Failure to do so can lead to a loss of precision marks.

Economic analysis often distinguishes between different time periods because the flexibility of factors of production varies. This distinction helps economists understand how firms and markets adjust to changes over different horizons, from immediate responses to long-term strategic shifts.

Short run — A time period in which it is possible to change only some inputs, typically when labour can be increased or decreased to change what is produced.

In the short run, at least one factor of production (usually capital) is fixed, while others (like labour) are variable. This means firms can adjust output by changing variable inputs but cannot alter their scale of operations. For example, a bakery in the short run can hire more bakers (labour) to make more bread, but it cannot immediately build a new, larger oven (capital).

Students often think the short run is a specific calendar period (e.g., less than a year), but actually it is defined by the fixity of at least one factor of production, regardless of the actual time duration.

When discussing production decisions, clearly state which factors are variable and which are fixed in the short run. For example, 'In the short run, a firm can vary its labour input while its capital remains fixed.'

Long run — A time period in which it is possible for all factors of production or resources to change.

In the long run, all inputs, including capital, are variable. This allows firms to adjust their scale of operations, build new factories, or adopt new technologies to achieve their objectives more efficiently. In the long run, the bakery can decide to build a larger, more efficient oven or even open a new branch, as all its inputs can be changed.

Students often think the long run is simply 'a long time', but actually it is defined by the ability to vary all factors of production, which could be a few months for some industries or many years for others.

Emphasize that in the long run, firms have greater flexibility to adjust their production capacity and can achieve optimal efficiency by changing all inputs. Contrast this with the short run's fixed factors.

Very long run — A time period where not only are all factors of production variable but all other key inputs are variable, including technology, government regulations, and social concerns.

This period accounts for fundamental shifts in the economic environment that go beyond just changing traditional factors of production. It considers broader societal and technological changes that influence economic outcomes. In the very long run, the bakery might see the invention of fully automated bread-making robots (technology) or new health regulations that change consumer demand for certain ingredients (social concerns).

Students often confuse the very long run with just a longer version of the long run, but actually it specifically includes changes to external factors like technology and regulations, not just traditional inputs.

When discussing the very long run, highlight the impact of non-traditional inputs like technological advancements, institutional changes, and evolving social preferences, as these distinguish it from the long run.

In evaluation questions, use the positive/normative distinction. First, analyse the testable economic consequences (positive), then discuss the value judgements behind the policy or argument (normative).

Always distinguish between short-run and long-run effects in your analysis. A policy's impact can differ significantly when all factors of production are able to adjust.

Advantages & Disadvantages

Using Positive Statements in Economic Analysis

Using Normative Statements in Economic Policy Debates

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining key terms such as positive and normative statements, ceteris paribus, and the different time periods. Briefly state the importance of these concepts in economic methodology and outline the scope of your essay.

Conclusion

Summarise the main arguments, reiterating the importance of a robust economic methodology for understanding and addressing economic issues. Conclude by reflecting on the interplay between objective analysis (positive) and value judgements (normative) in shaping economic thought and policy.

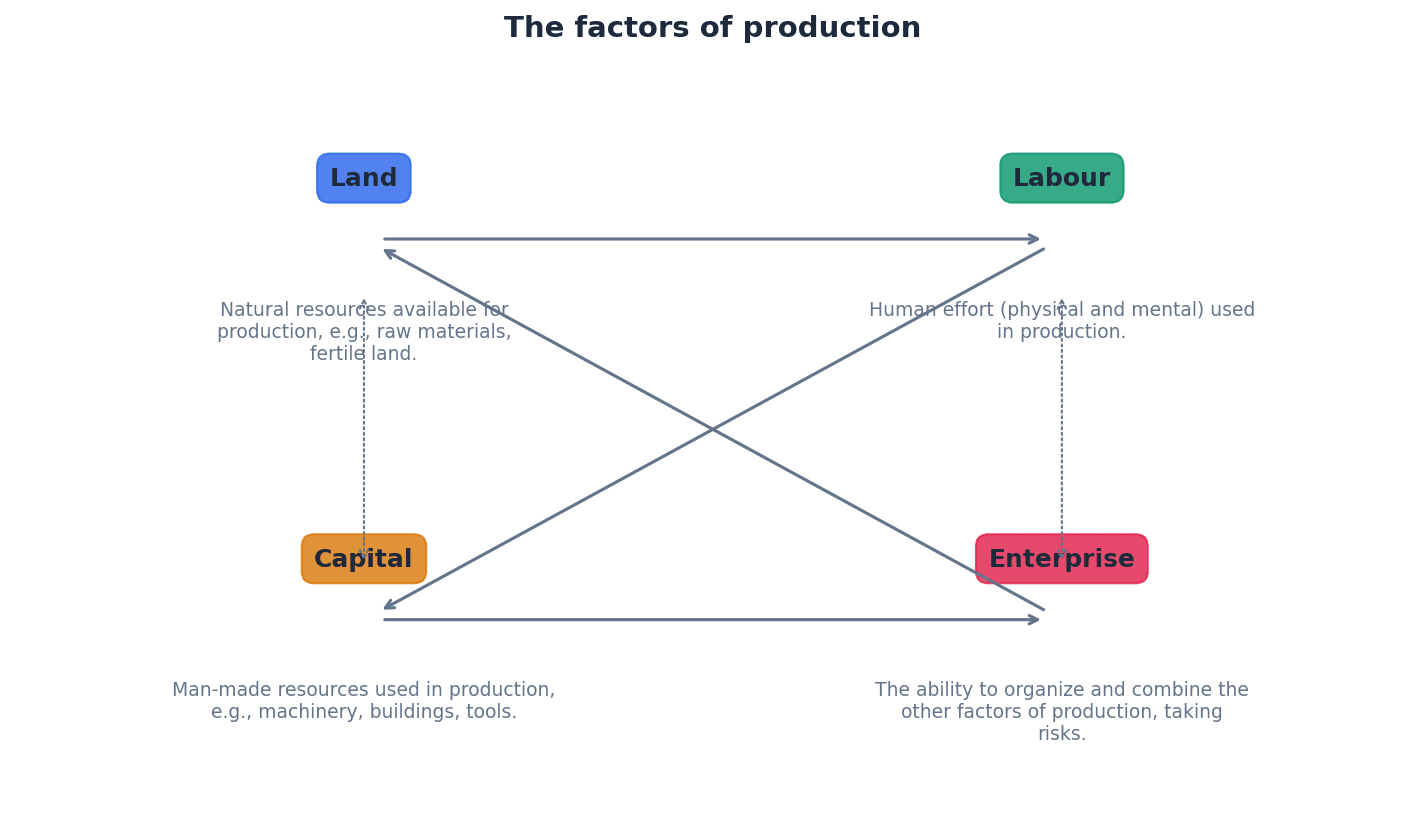

This chapter introduces the four fundamental factors of production: land, labour, capital, and enterprise, explaining their individual roles and rewards in an economy. It distinguishes between human and physical capital, and explores how specialisation and the division of labour enhance output, concluding with the critical function of the entrepreneur.

Factors of production — The means by which an economy produces a whole range of goods and services to meet the needs of its population.

These are the fundamental resources available in an economy, categorised into land, labour, capital, and enterprise. Owners of these factors receive payments when they are used by others, forming the basis of economic activity. Think of factors of production as the ingredients and tools a chef needs to make a meal: the kitchen (land), the chef's skills (labour), the oven and utensils (capital), and the chef's vision and risk-taking to create a new dish (enterprise).

Students often think factors of production are just physical items, but actually they include human resources and the intangible ability to organise and take risks.

When asked to 'define' factors of production, ensure you list all four and briefly explain what each entails, as this demonstrates comprehensive understanding.

Land — A natural resource that includes mineral deposits, rivers, lakes, climate, soil for agriculture, trees, and vegetation.

This factor encompasses all natural resources, both above and below the earth's surface, that are used in production. Its quality and quantity are crucial, especially in the context of climate change and resource availability. Imagine a farm: the soil, the water from the rain, the sunlight, and any minerals in the ground are all 'land'. It's not just the physical plot of ground, but all the natural elements it provides.

Students often think 'land' only refers to the physical space for buildings, but actually it's much broader, including all natural resources like oil, climate, and forests.

When providing examples of 'land', ensure you go beyond just physical space and include natural elements like climate, mineral deposits, and water sources to show a full understanding.

Labour — The human resources available in any economy.

This factor refers to the physical and mental effort contributed by people to the production of goods and services. Both the quantity (number of workers) and quality (skills, education) of labour are vital for economic progress. In a car factory, the engineers designing the car, the assembly line workers, and the sales staff are all 'labour'. Their collective effort and skills contribute to making and selling the cars.

Students often think 'labour' is just about the number of people working, but actually the quality of labour, including skills and education, is equally important for economic progress.

When discussing 'labour', remember to consider both its quantity (e.g., population size, working age) and its quality (e.g., education, training, skills) as both impact productivity and economic growth.

Capital — A type of physical resource including anything that can be regarded as made by humans to aid production.

This factor comprises man-made goods used to produce other goods and services, such as factories, machinery, and infrastructure. It is combined with land and labour to facilitate production and its quality is particularly important in developing economies. For a baker, 'capital' would be the oven, the mixing machines, the delivery van, and the bakery building itself. These are all man-made tools that help the baker produce bread.

Students often think 'capital' means money, but actually in economics, it refers to physical assets like machinery and factories used in production, not financial capital.

Distinguish clearly between 'physical capital' (factories, machinery) and 'financial capital' (money) in your answers. The economic definition of capital refers to the former.

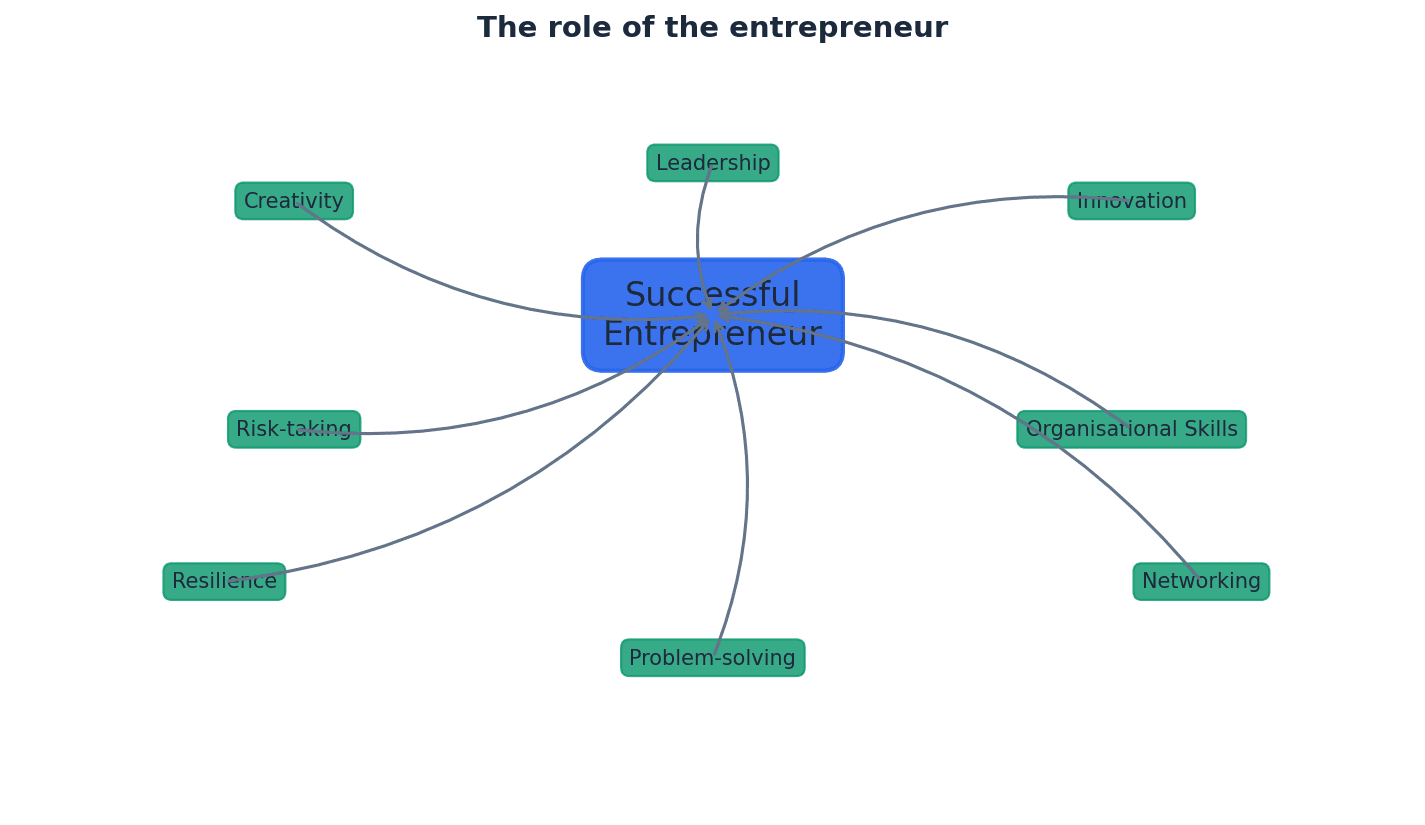

Enterprise — A form of human capital that organises other factors of production and refers to the ability and inventiveness of entrepreneurs who are prepared to take risks.

This factor is crucial for initiating and managing production, involving the entrepreneur's role in combining land, labour, and capital, and bearing the risks associated with business ventures. The reward for enterprise is profit. Think of a film director: they bring together the actors (labour), the set locations (land), the cameras and equipment (capital), and take the financial risk to create a movie. That's enterprise in action.

Students often think 'enterprise' is just about starting a business, but actually it specifically involves the organisation of other factors of production and the willingness to take risks.

When explaining the role of an entrepreneur, emphasise both their organisational function (combining factors) and their risk-taking ability, as both are key aspects of enterprise.

Human capital — The value of labour in contributing to the productive potential or future growth in an economy, covering the skills, knowledge and experience of labour.

This concept highlights the importance of investing in people's education, training, and health to enhance their productivity and future earnings. It applies to individuals and the population as a whole, driving economic growth. If a carpenter goes to a special course to learn how to build custom furniture, the new skills and knowledge they gain are 'human capital'. This investment makes them more valuable and productive.

Students often confuse 'human capital' with just 'labour', but actually human capital specifically refers to the *quality* of labour – the skills, knowledge, and experience that add value.

When comparing human capital and physical capital, focus on how human capital represents an investment in people's abilities, leading to future productivity gains, rather than just the physical presence of workers.

Physical capital — The result of more resources being made by businesses and government in the wide range of items such as factories, machinery and infrastructure.

This is the tangible capital used in production, distinct from human capital. Its quality and quantity are often considered a primary source of economic growth, especially in developing countries, by improving productive capacity. The machines in a factory, the roads for transport, and the office buildings are all 'physical capital'. They are tangible assets created by humans to help produce other goods and services.

Ensure you clearly differentiate physical capital (tangible assets) from human capital (skills and knowledge) and financial capital (money) in your explanations, as they are distinct economic concepts.

Human capital represents the value derived from the skills, knowledge, and experience of the labour force, which contributes to an economy's productive potential and future growth. In contrast, physical capital refers to the tangible, man-made resources like factories, machinery, and infrastructure that are used to aid production. While both are crucial for economic growth, human capital focuses on investment in people's abilities, whereas physical capital involves investment in physical assets to enhance productive capacity.

Specialisation — A situation where individuals and firms, regions and entire economies concentrate on producing some goods and services rather than others.

This process allows entities to focus on what they are best at, leading to increased efficiency and higher output. While it boosts production, it also necessitates exchange or trade as no one becomes self-sufficient. A baker specialises in making bread, while a farmer specialises in growing wheat. Both produce a surplus of their specialty, which they then trade with each other to meet all their needs.

Students often think specialisation means doing everything perfectly, but actually it means focusing on a specific task or product where one has a comparative advantage, even if not absolutely the best at everything.

When explaining specialisation, discuss both its benefits (increased output, efficiency) and its potential drawbacks (redundancy of skills, reliance on trade, vulnerability to market changes).

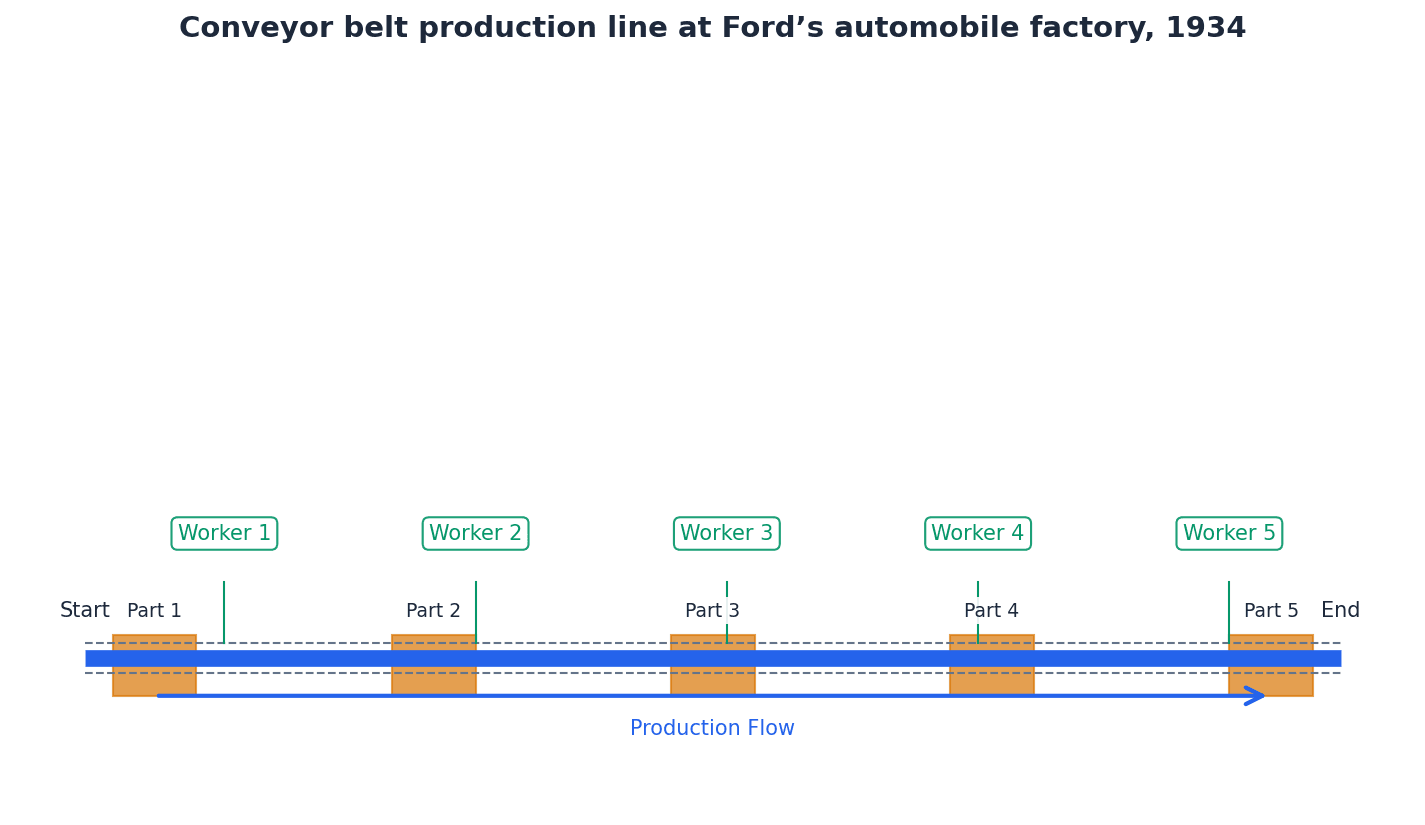

Division of labour — The process of production being broken down into a series of tasks, with each employee carrying out only one or a few of these operations.

This is a specific application of specialisation within a production unit, where workers focus on a single task. It typically leads to increased output per worker, improved quality, and reduced costs, but can also cause worker dissatisfaction. In a car assembly line, one worker might only install the wheels, another might only fit the doors, and another might only paint the car. Each specialises in a small part of the overall process.

Students often confuse 'division of labour' with 'specialisation' generally, but actually division of labour is a specific form of specialisation applied within a production process, breaking it into distinct tasks.

When asked about the division of labour, remember to mention Adam Smith's pin factory example as a classic illustration and discuss both the benefits (efficiency, output) and drawbacks (boredom, de-skilling) for workers.

Specialisation occurs when individuals, firms, or economies concentrate on producing specific goods or services. The division of labour is a particular form of specialisation where the production process is broken down into distinct tasks, with each worker focusing on one or a few operations. Both methods aim to increase output and efficiency, leading to higher productivity and potentially lower costs per unit. For example, a conveyor belt production line, such as those historically used at Ford's automobile factory, exemplifies the division of labour.

The entrepreneur plays a crucial role in 21st-century economies by organising the other factors of production: land, labour, and capital. They are responsible for combining these resources effectively to produce goods and services. Beyond organisation, entrepreneurs are also risk-takers, willing to bear the uncertainties associated with business ventures in pursuit of profit. Figures like James Dyson exemplify the entrepreneurial spirit, innovating and taking risks to bring new products to market.

When defining the four factors of production, also state their rewards: Rent (Land), Wages (Labour), Interest (Capital), and Profit (Enterprise).

For questions on specialisation, always provide a balanced answer by discussing both the benefits (e.g., higher output) and the drawbacks (e.g., worker boredom, over-reliance).

Clearly distinguish between an increase in 'physical capital' (more machines) and 'human capital' (a more skilled workforce) when explaining economic growth.

Advantages & Disadvantages

Specialisation

Division of Labour

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the factors of production and briefly outlining their importance in an economy. State the main arguments you will present regarding their roles and interconnections.

Conclusion

Summarise the key roles of the factors of production and their interdependencies. Reiterate the importance of effective organisation and investment in these factors for sustained economic growth and development. Offer a final evaluative thought on the dynamic nature of these factors in a changing global economy.

This chapter explores how different economic systems address the fundamental problem of scarcity and allocate resources. It details the characteristics, advantages, and disadvantages of market, planned, and mixed economies, emphasizing the role of the price mechanism and central planning.

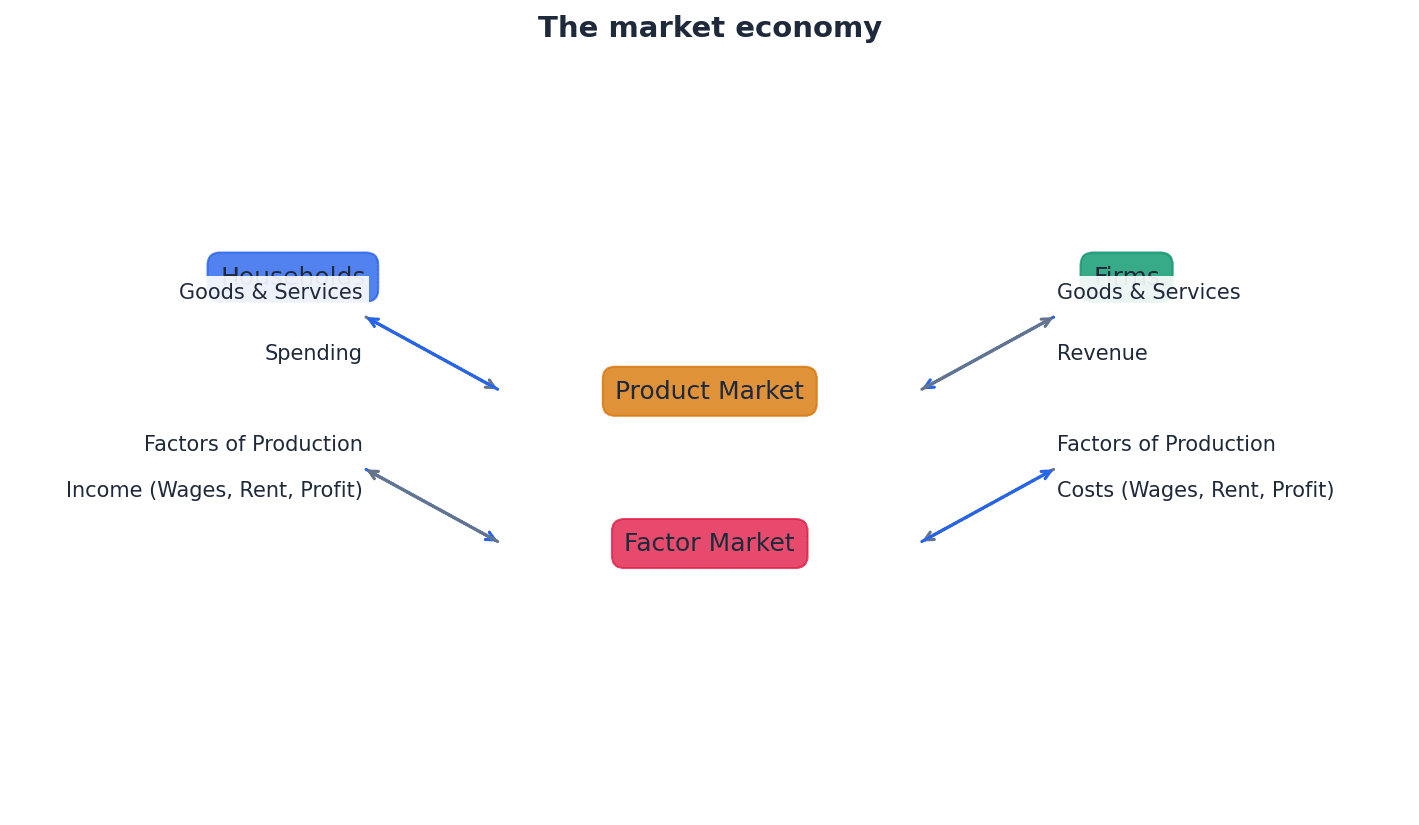

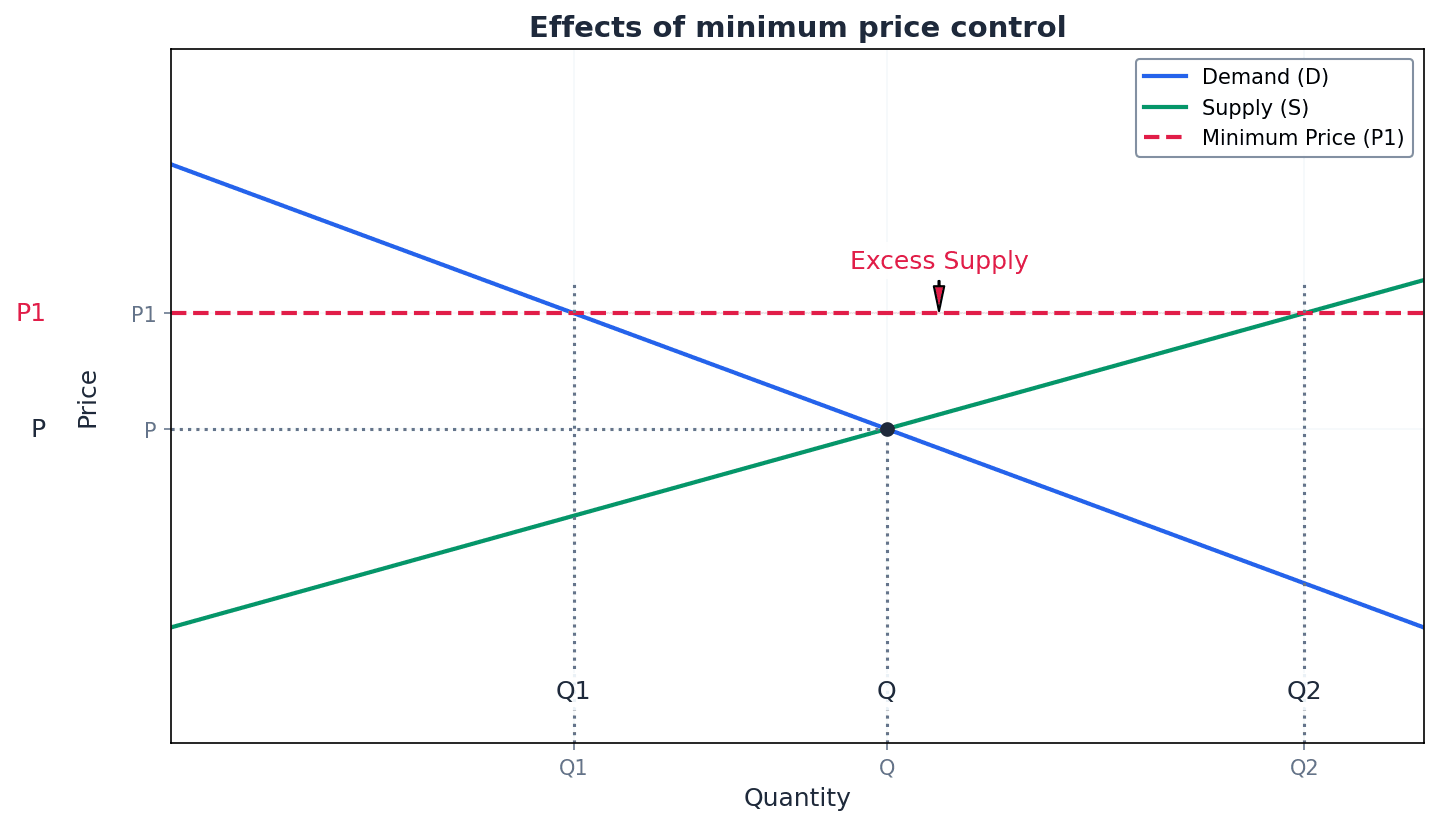

market economy — An economic system where resource allocation decisions are largely driven by the market mechanism, with individuals and firms making decisions without government intervention.

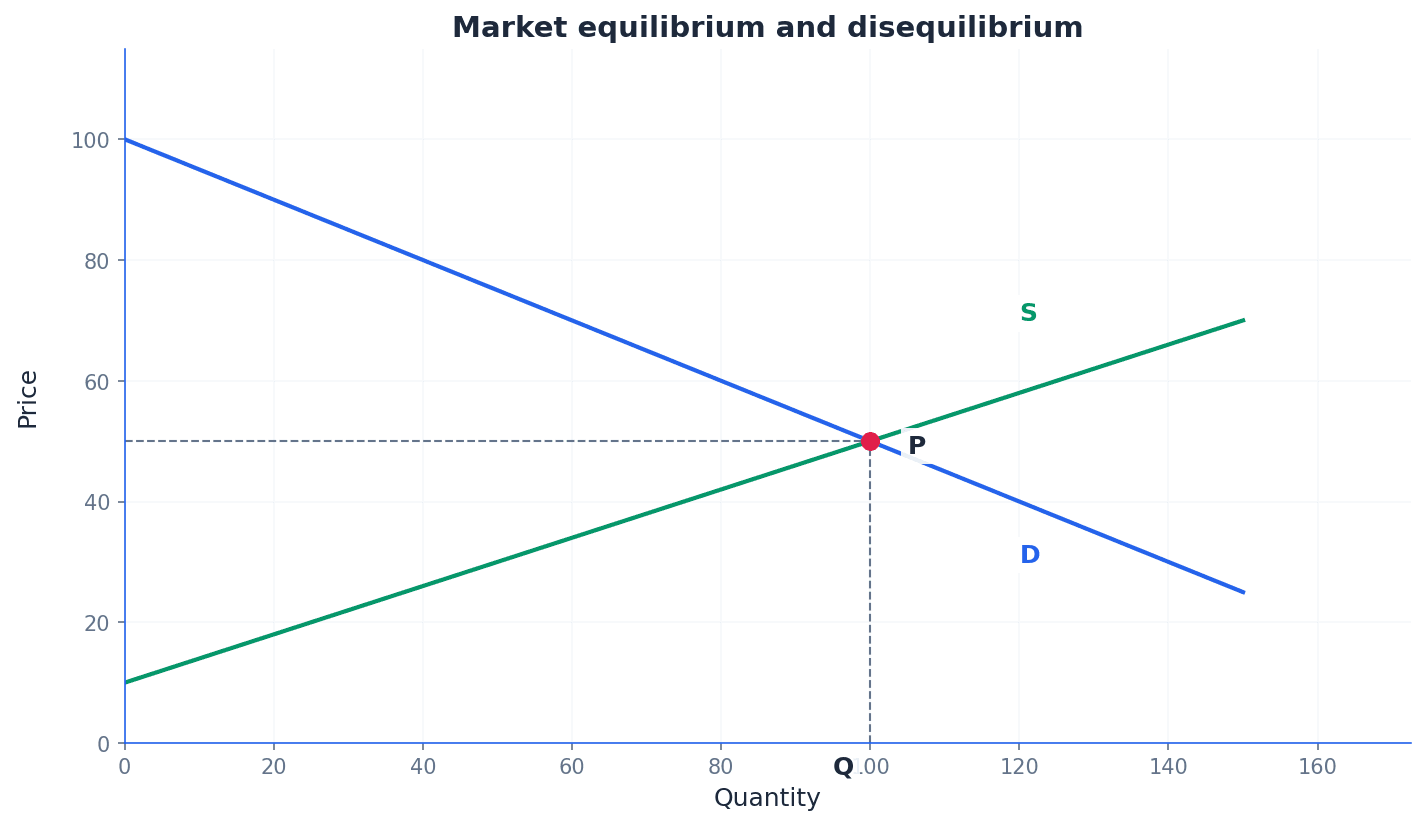

In a market economy, the forces of demand and supply, operating through the price mechanism, determine what, how, and for whom goods and services are produced. The government's role is minimal, primarily intervening only in cases of market failure. Imagine a giant farmers' market where every farmer decides what to grow based on what customers want and what prices they can get, and customers decide what to buy based on their needs and the prices offered, with no central authority.

Students often think a market economy means no government at all. However, governments in market economies still provide some public services and regulate to prevent market failures.

When asked to 'explain' the workings of a market economy, ensure you detail the role of the price mechanism and the limited government intervention, using terms like 'demand', 'supply', and 'self-interest'.

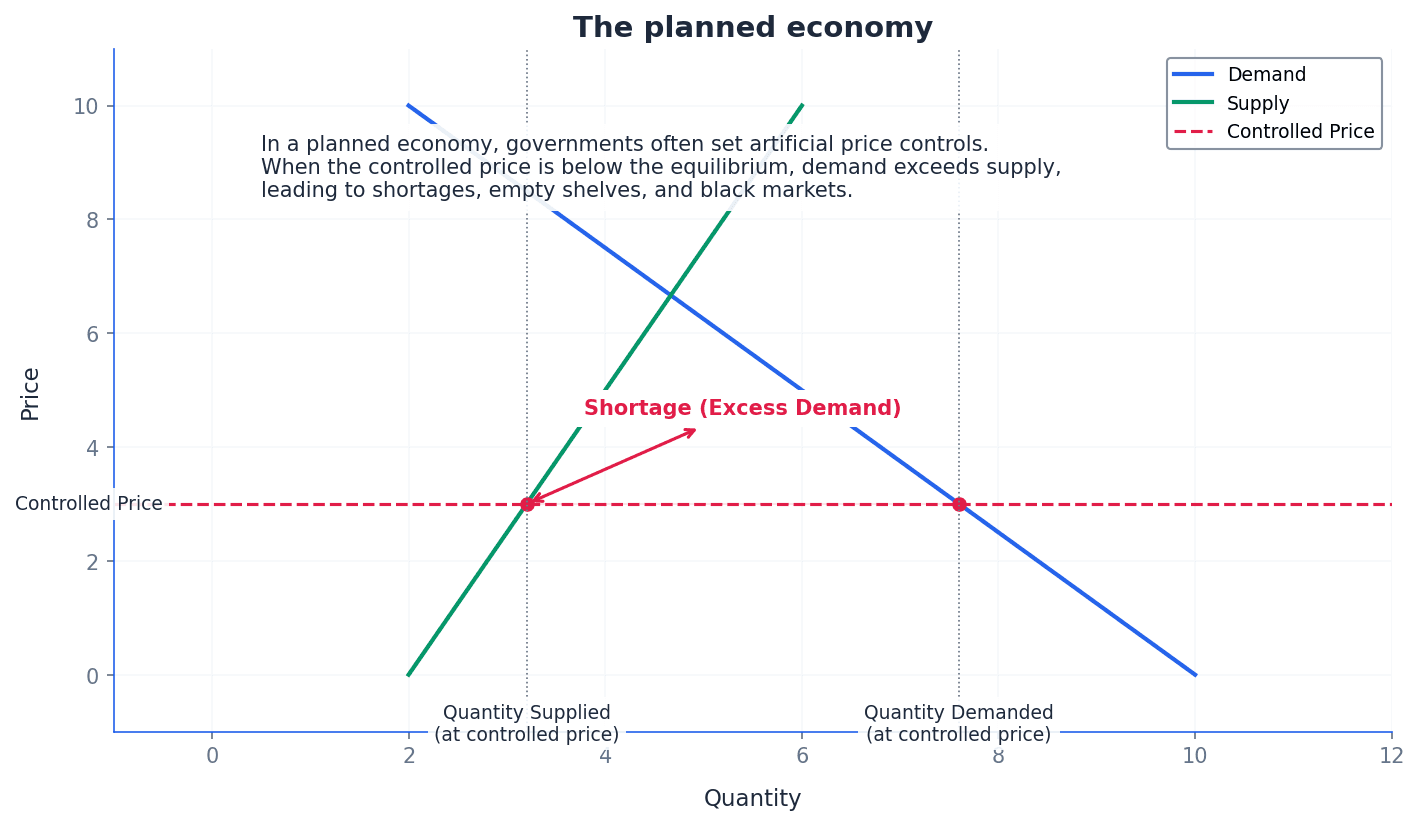

planned economy — An economic system where the government has a central role in all decisions regarding resource allocation, controlling what, how, and for whom goods and services are produced.

In a planned economy, central planning boards set production targets, control prices and wages, and own most productive resources. Consumer preferences and market forces have little to no role in resource allocation. Think of a single, massive company that owns all the factories, farms, and shops in a country, and its CEO (the government) decides exactly what everyone will produce, how much it will cost, and who gets it.

Students often think planned economies are purely theoretical. However, countries like Cuba and North Korea operate very close to the theoretical model, albeit with some minor private activity.

When discussing planned economies, remember to include present-day examples like Cuba or North Korea to demonstrate understanding, and highlight consequences such as shortages due to price controls.

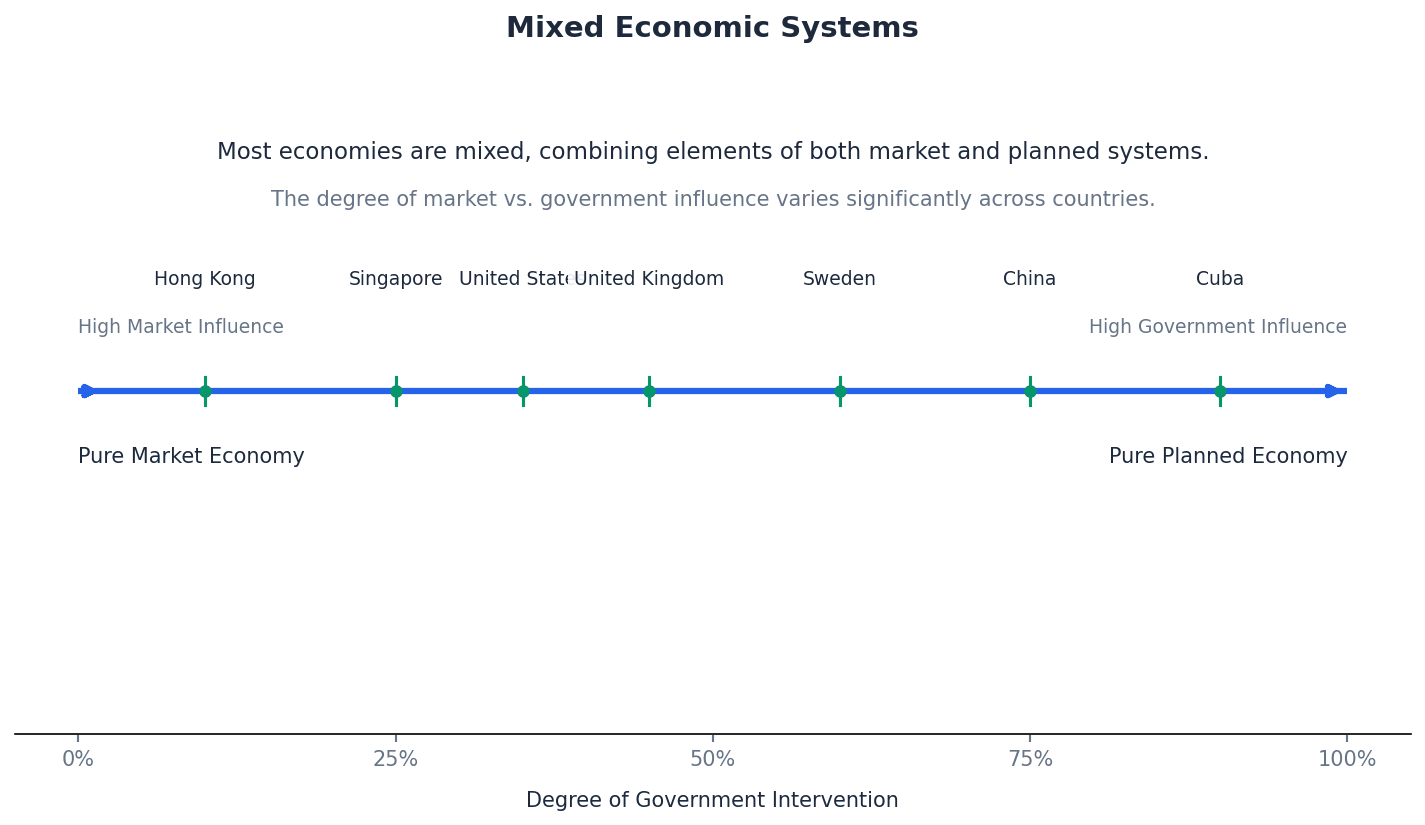

mixed economy — An economic system where both the private sector and public sector play a part in the allocation of resources, involving an interaction between firms, labour, and the government.

Mixed economies combine elements of both market and planned systems, with private ownership of most productive resources alongside some public ownership. Decisions are influenced by both market mechanisms and government intervention. Consider a football game where the players (private sector) largely decide their moves on the field, but there's also a referee (government) who enforces rules, calls fouls, and sometimes makes decisions that affect the flow of the game.

Students often think the classification of economies is exact. However, most economies are some form of mixed system, varying in the relative importance of the market mechanism and government.

When analysing a mixed economy, ensure you discuss the balance between market forces and government intervention, and consider the impact of policies like privatisation on resource allocation.

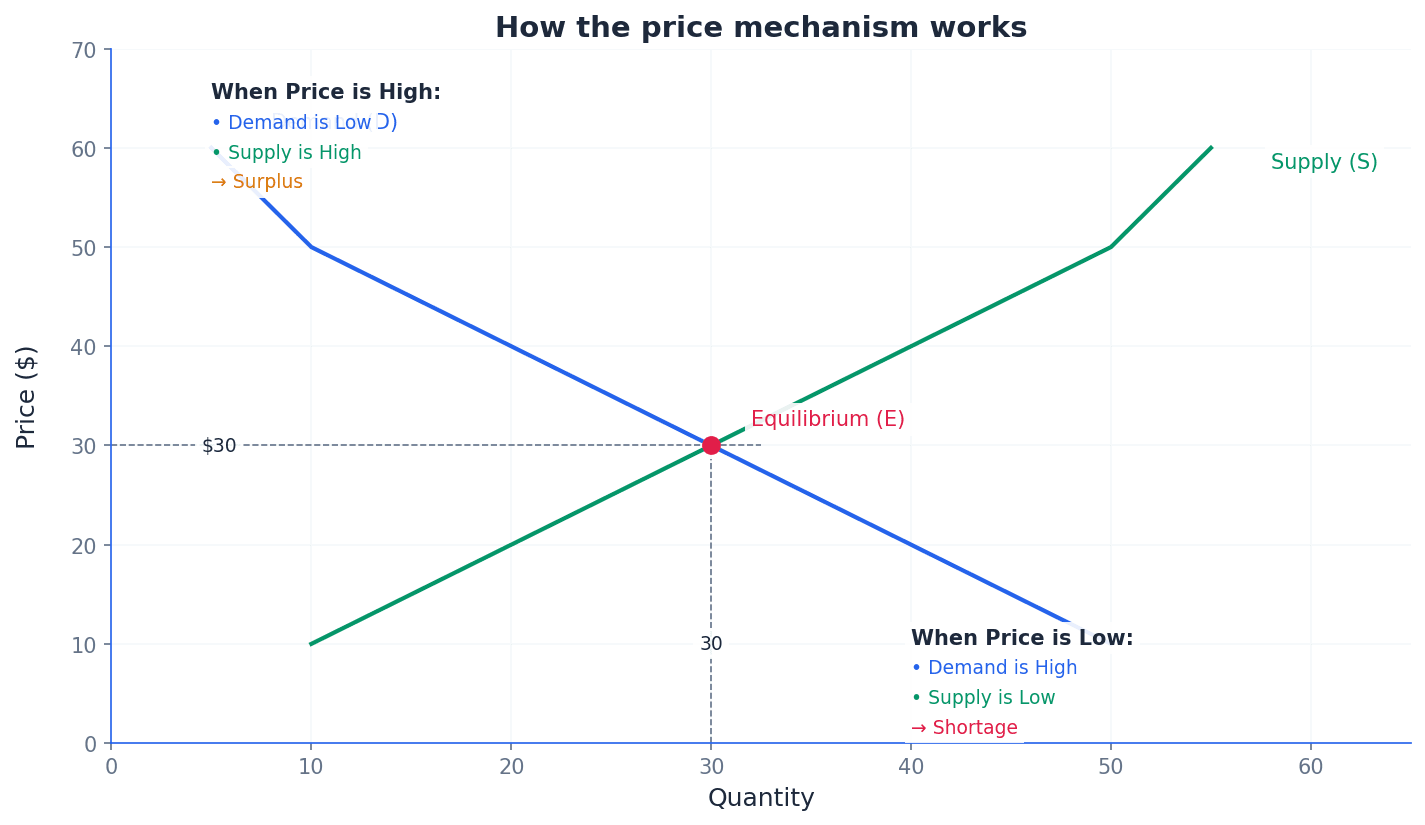

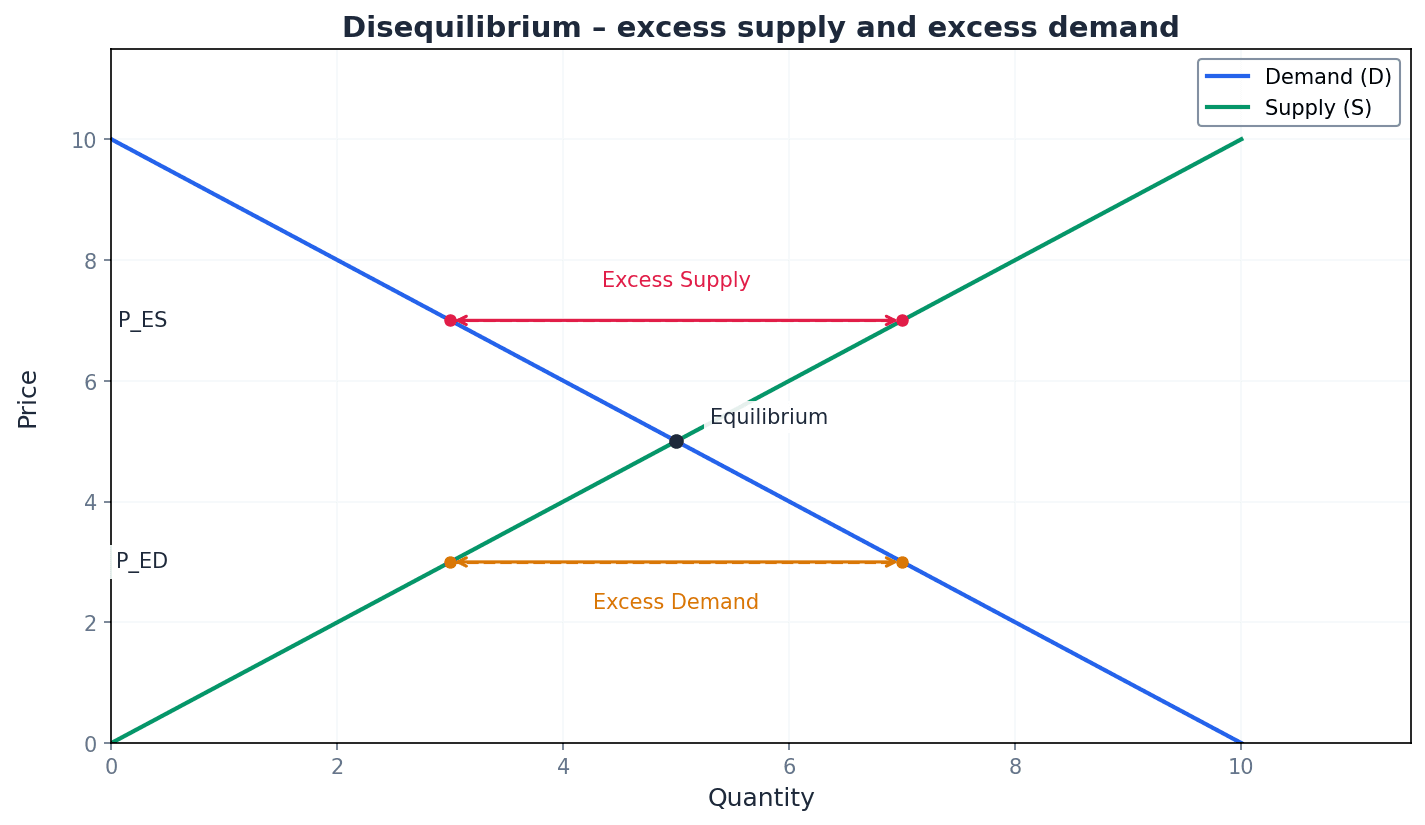

price mechanism — The process by which the forces of demand and supply interact to determine prices and allocate resources in a market economy.

The price mechanism works through changes in prices signaling to producers and consumers where resources are most needed. Excess supply leads to falling prices, discouraging production, while excess demand leads to rising prices, encouraging production. Imagine prices as traffic lights in an economy: a high price is a green light for producers to make more, and a red light for consumers to buy less; a low price is the opposite, guiding resources to where they are most valued.

Students often think the price mechanism only works when prices rise. However, it also functions when prices fall, signaling to firms to reduce supply or exit the market.

When explaining the price mechanism, use a diagram to illustrate how excess supply or demand leads to price adjustments and a movement towards equilibrium, clearly labeling axes and curves.

excess supply — A situation where the quantity supplied of a good or service exceeds the quantity demanded at a given price.

Excess supply results in goods being stockpiled, prompting firms to reduce prices to encourage purchases and clear stocks. This adjustment is a key part of how the price mechanism works to restore equilibrium. Imagine a baker making 100 loaves of bread but only 50 customers want to buy them at the current price; the remaining 50 loaves are excess supply.

market failure — A situation where the price mechanism does not provide the best allocation of resources.

Market failure occurs when the free market fails to allocate resources efficiently, leading to an underprovision of certain goods (like healthcare), non-provision of others (like fire services), or firms exploiting market power for excessive gain. Imagine a broken compass that points in the wrong direction; similarly, market failure means the price mechanism (the 'compass' of the economy) is not guiding resources to their optimal use.

Students often think market failure means the market completely stops working. However, it means the market is working inefficiently, leading to suboptimal outcomes for society.

When identifying market failures, provide specific examples such as public goods (non-excludable, non-rivalrous) or externalities, and explain why the market alone cannot provide them efficiently.

privatisation — The transfer of resources from public ownership to the private sector.

Privatisation is a trend seen in many economies, including former planned economies, as they move towards a mixed economic system. It involves selling state-owned enterprises or assets to private individuals or companies. It's like a public library (government-owned) being sold to a private company that then runs it as a for-profit bookstore.

When discussing privatisation, consider both the potential benefits (e.g., efficiency, innovation) and drawbacks (e.g., higher prices, job losses) and link them to resource allocation.

All economic systems must address the fundamental problem of scarcity by answering three core resource allocation questions: What to produce? How to produce it? For whom to produce it? Different economic systems—market, planned, and mixed—provide distinct frameworks for making these decisions.

In a market economy, the price mechanism is central to resource allocation. It acts as a signaling system, where changes in prices communicate information to both producers and consumers. For instance, rising prices signal to producers that a good is in high demand, encouraging them to increase supply, while falling prices signal excess supply, prompting firms to reduce output or exit the market.

While market economies are characterized by minimal government intervention, the government still plays a crucial role. Its primary functions include providing public services, regulating markets to ensure fair competition, and intervening to correct market failures, which occur when the price mechanism fails to allocate resources efficiently.

Most real-world economies are mixed, combining elements of both market and planned systems. This means that both the private sector, driven by market forces, and the public sector, influenced by government intervention, play a part in resource allocation. The balance between these two sectors varies significantly across different countries, with some leaning more towards market mechanisms (like New Zealand) and others retaining more government control.

When comparing economic systems, structure your answer around their different approaches to the 'What, How, and For Whom' questions.

In evaluation questions, always present a balanced view. For example, discuss the advantages of the price mechanism (e.g., efficiency) alongside its disadvantages (e.g., market failure).

Advantages & Disadvantages

Market Economy

Planned Economy

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the core problem of scarcity and the three fundamental economic questions. Then, briefly introduce the three main economic systems (market, planned, mixed) and state the essay's purpose, e.g., to compare their resource allocation mechanisms and evaluate their advantages and disadvantages.

Conclusion

Summarise the main arguments, reiterating that all systems face trade-offs in addressing scarcity. Conclude by stating that most real-world economies are mixed, reflecting an ongoing attempt to find an optimal balance between market forces and government intervention, and that the 'best' system is often context-dependent.

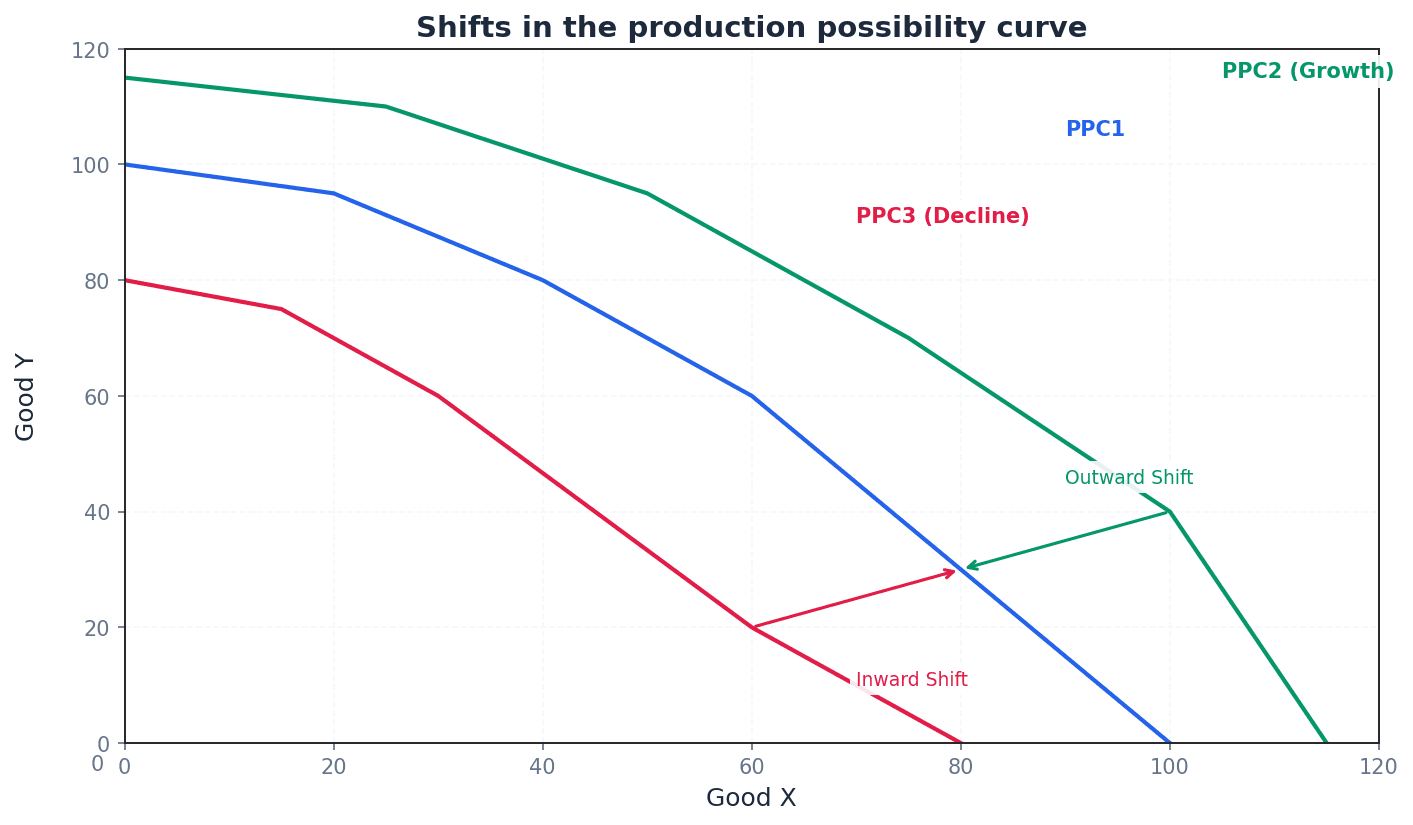

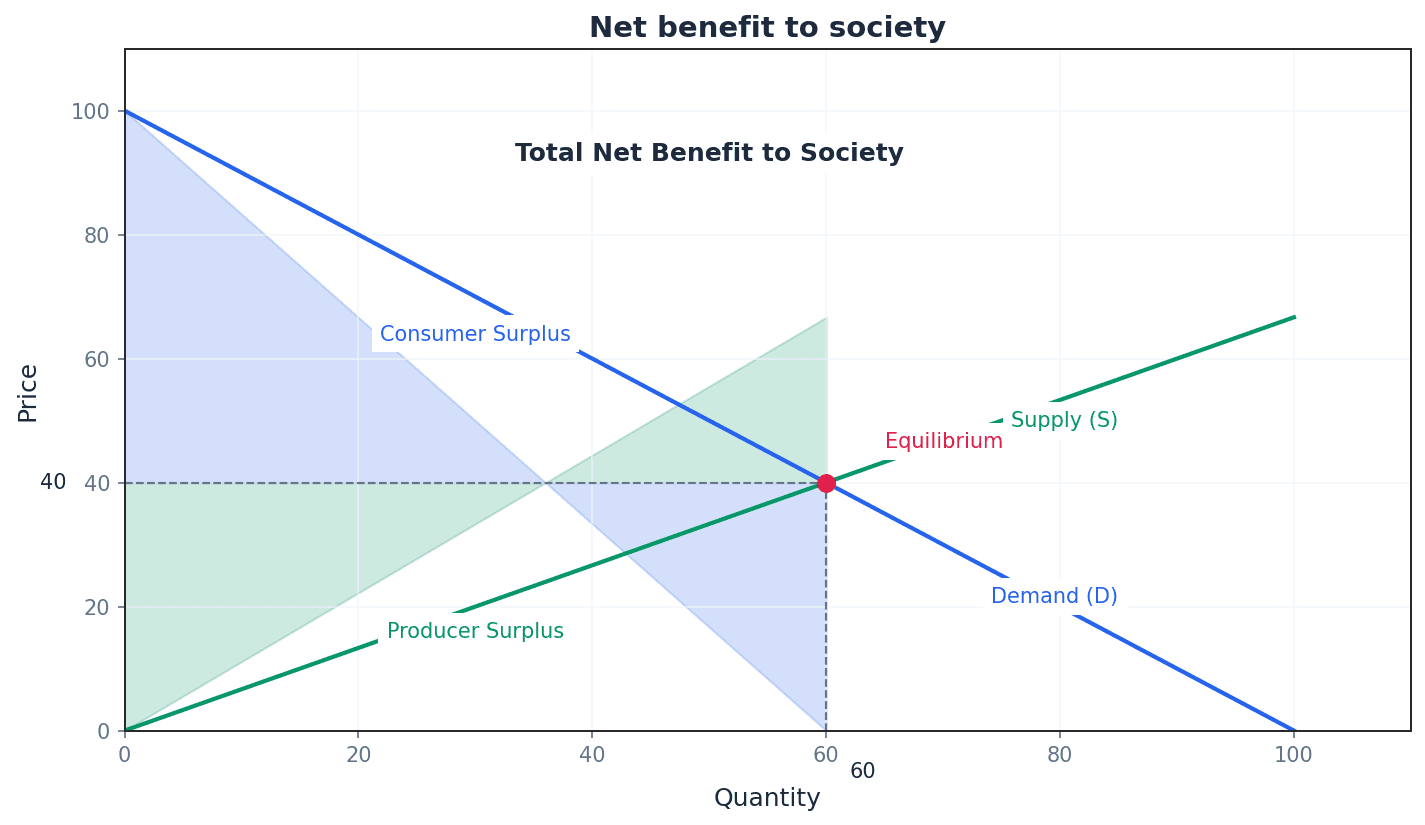

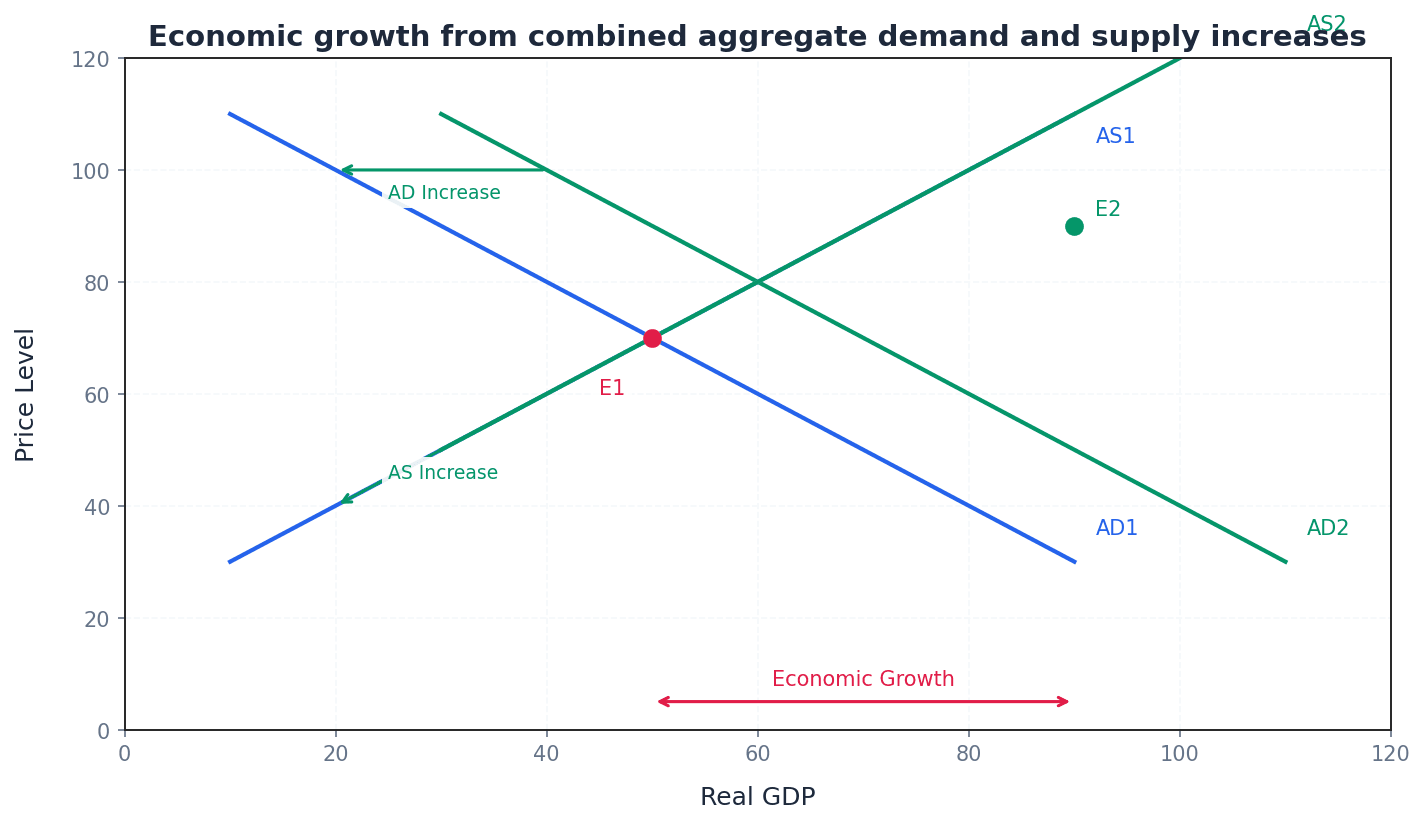

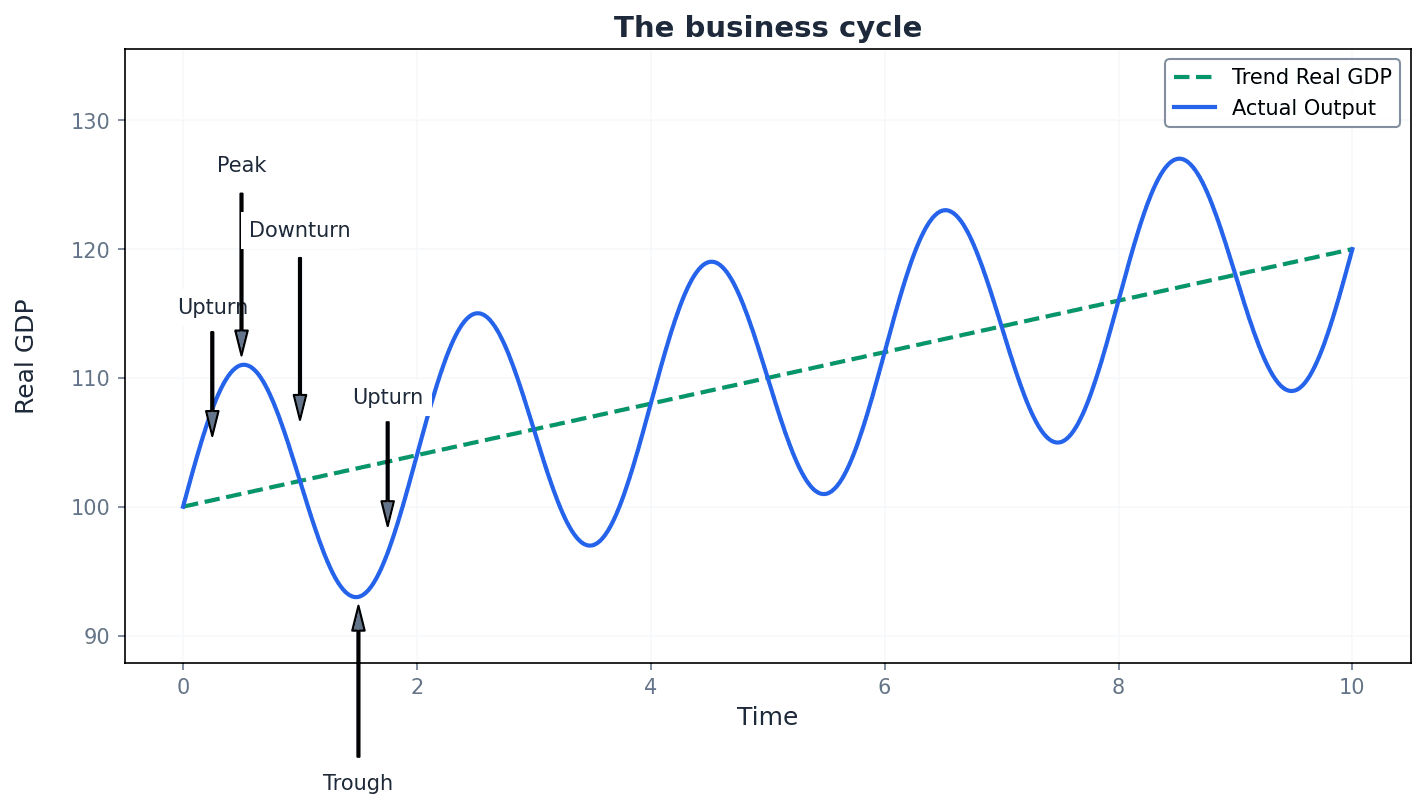

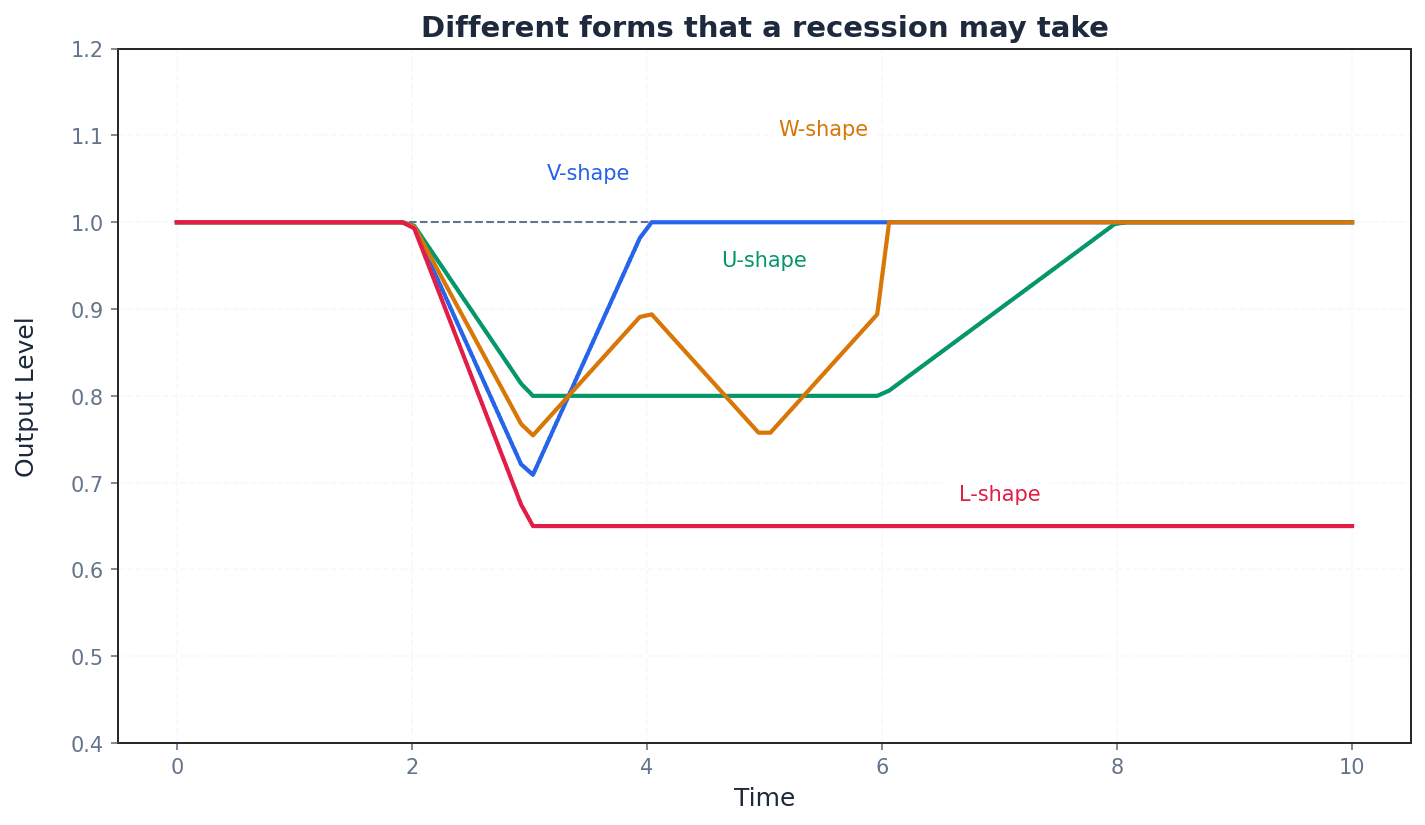

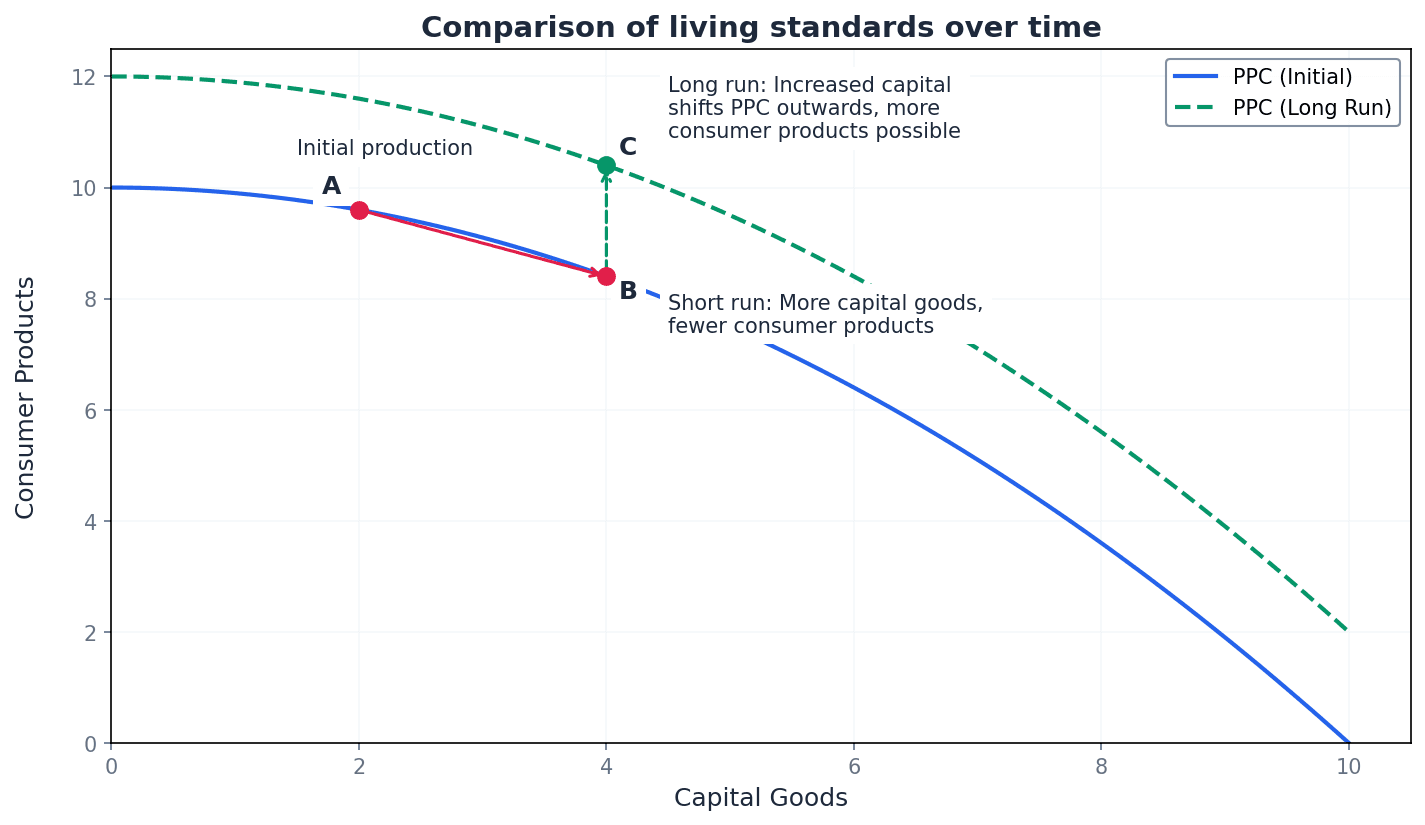

This chapter introduces the Production Possibility Curve (PPC) as a fundamental economic model illustrating scarcity, choice, and opportunity cost. It explores how the PPC's shape reflects different opportunity costs and how shifts in the curve represent changes in an economy's productive capacity due to resource or technological changes.

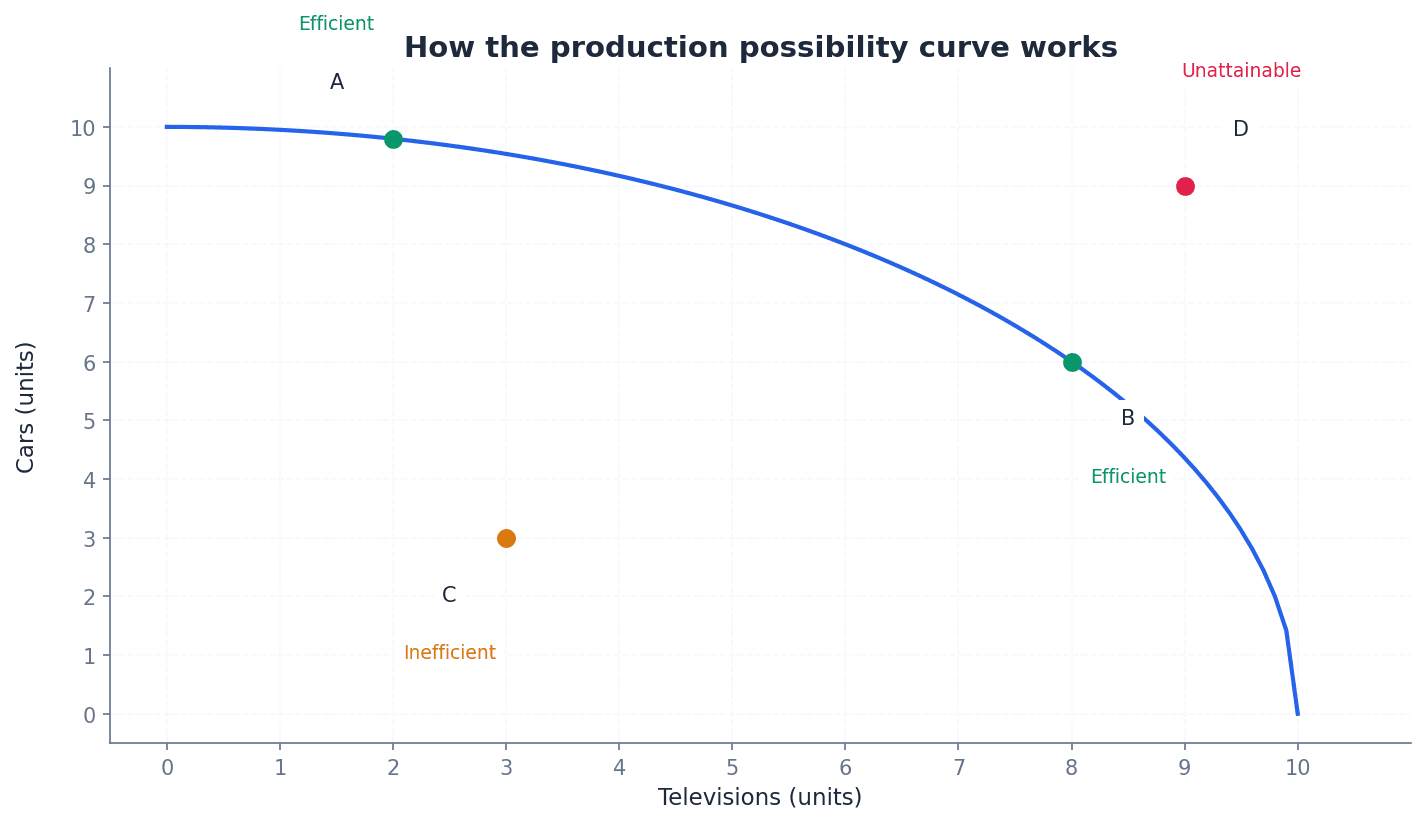

production possibility curve — A simple economic model that shows the choices available and how resources are allocated, representing the maximum level of output of each of two goods that can be produced.

Also known as the production possibility frontier, it draws a boundary between what can be produced and what cannot. Any point on the curve signifies efficient resource allocation, while points inside indicate inefficiency and points outside are unattainable with current resources. Imagine a baker who can make either cakes or cookies with a fixed amount of flour, sugar, and time. The PPC shows all the combinations of cakes and cookies they can make if they use all their ingredients and time efficiently.

scarcity — A situation where the economy does not have the resources required to achieve a desired level of output of goods.

Scarcity is a fundamental economic problem that necessitates choices about resource allocation. On a PPC diagram, scarcity is represented by any point outside the curve, indicating an unattainable production level. If you only have £10, you face scarcity because you can't buy everything you want; you have to choose what to buy within your budget.

Students often think scarcity means there's 'not enough' of something, but actually it means there are insufficient resources to satisfy all wants, even if some quantity exists.

opportunity cost — The benefit given up from the production of one good when resources are reallocated to produce more of another good.

It is the value of the next best alternative forgone. On a PPC, moving from one point to another demonstrates opportunity cost, as producing more of one good requires giving up some production of the other. This cost can be constant (straight-line PPC) or increasing (curved PPC). If you choose to spend your Saturday studying for an exam, the opportunity cost is the fun you could have had going to a party with friends.

Students often think opportunity cost is just the monetary price, but actually it's the value of the next best alternative forgone, which might not have a direct monetary cost.

trade-off — The process of deciding whether to give up some of one good in order to obtain more of another.

A trade-off is inherent in situations of scarcity where resources are fully utilised. On a PPC, any movement along the curve represents a trade-off, as increasing the production of one good necessitates decreasing the production of another. The numerical extent of a trade-off can be quantified by comparing the changes in production levels. Choosing to spend more time on your part-time job means you have to trade off some study time, or vice versa.

Students often confuse trade-off with opportunity cost, but actually a trade-off is the act of making a choice between alternatives, while opportunity cost is the value of the specific alternative that was forgone.

productive capacity — The total ability of an economy to produce goods and services.

This is represented by the position of the production possibility curve. An outward shift of the PPC indicates an increase in productive capacity, while an inward shift indicates a decrease. Changes in resource availability or technology are the main drivers of shifts in productive capacity. Think of a factory's maximum output. If the factory gets new, more efficient machines or hires more skilled workers, its productive capacity increases, allowing it to make more products.

Students often think productive capacity only refers to current output, but actually it refers to the maximum potential output an economy can achieve if all resources are fully and efficiently utilized.

The production possibility curve (PPC) serves as a simple economic model to illustrate fundamental economic concepts such as scarcity, choice, and opportunity cost within an economy. It delineates the maximum level of output of two goods that can be produced given an economy's available resources and technology. The PPC acts as a boundary, separating what is achievable from what is not, thereby highlighting the trade-offs inherent in resource allocation.

When asked to 'explain the meaning and purpose' of a PPC, ensure you define it as a boundary of maximum output and state its use in illustrating scarcity, choice, and opportunity cost. Label axes clearly with two goods.

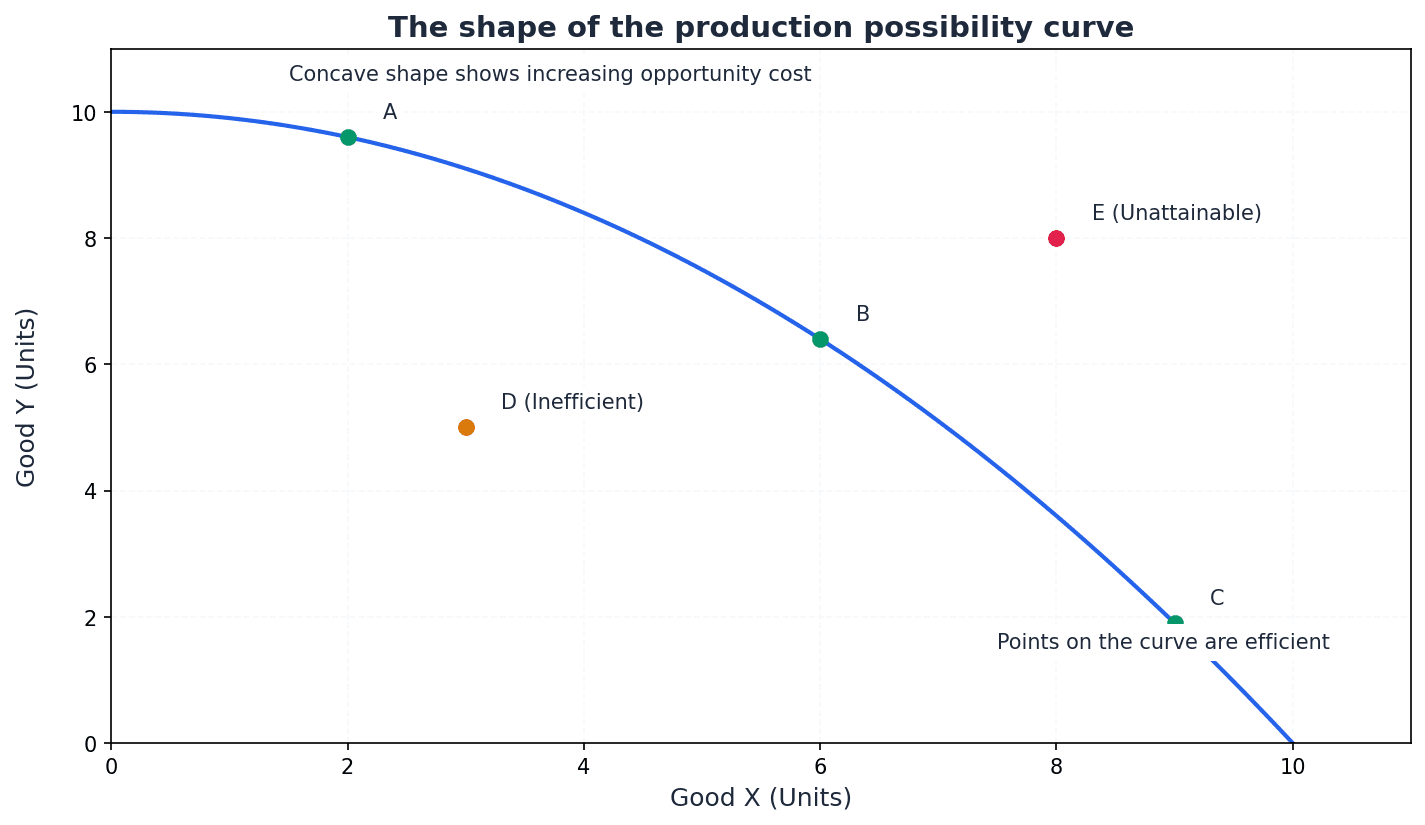

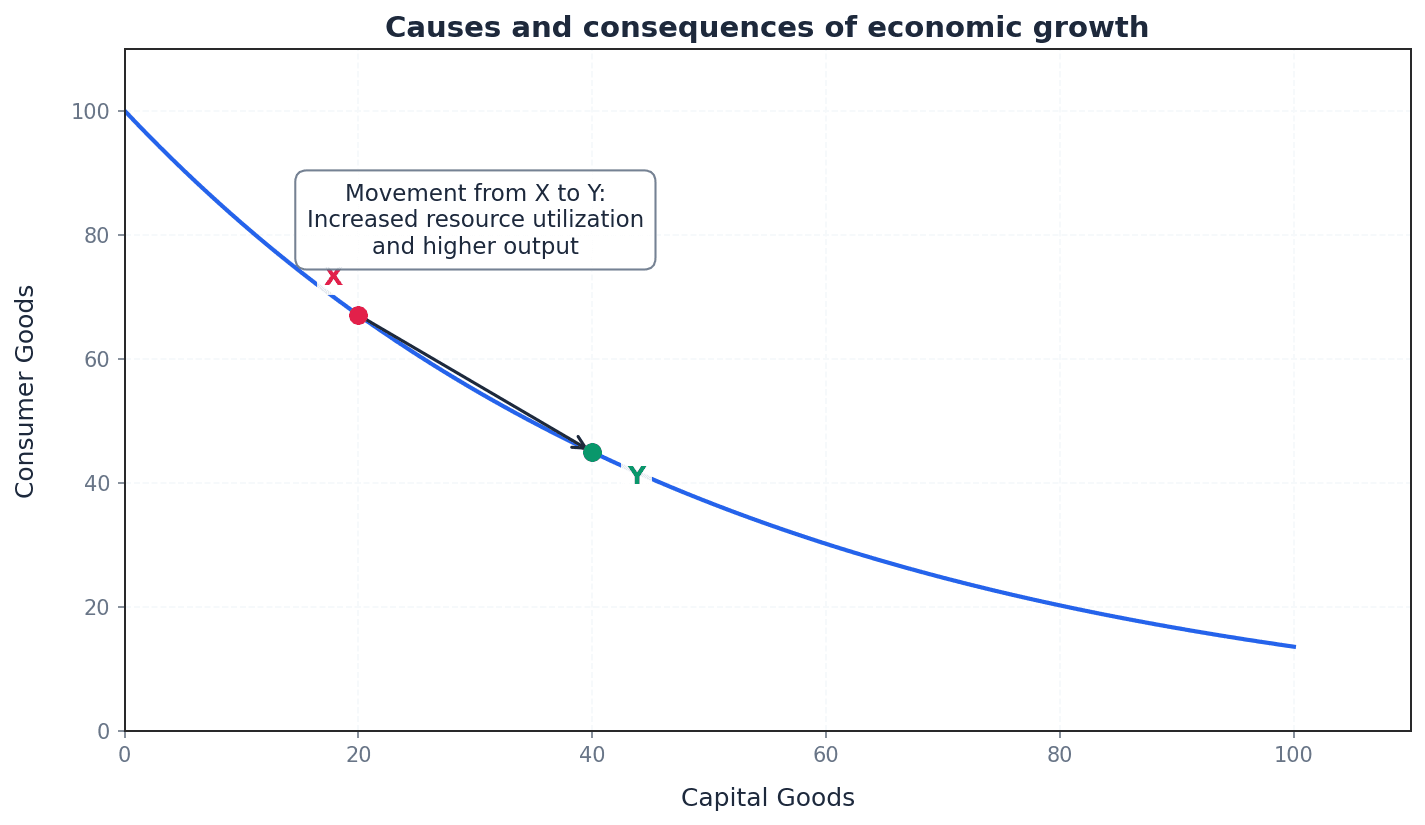

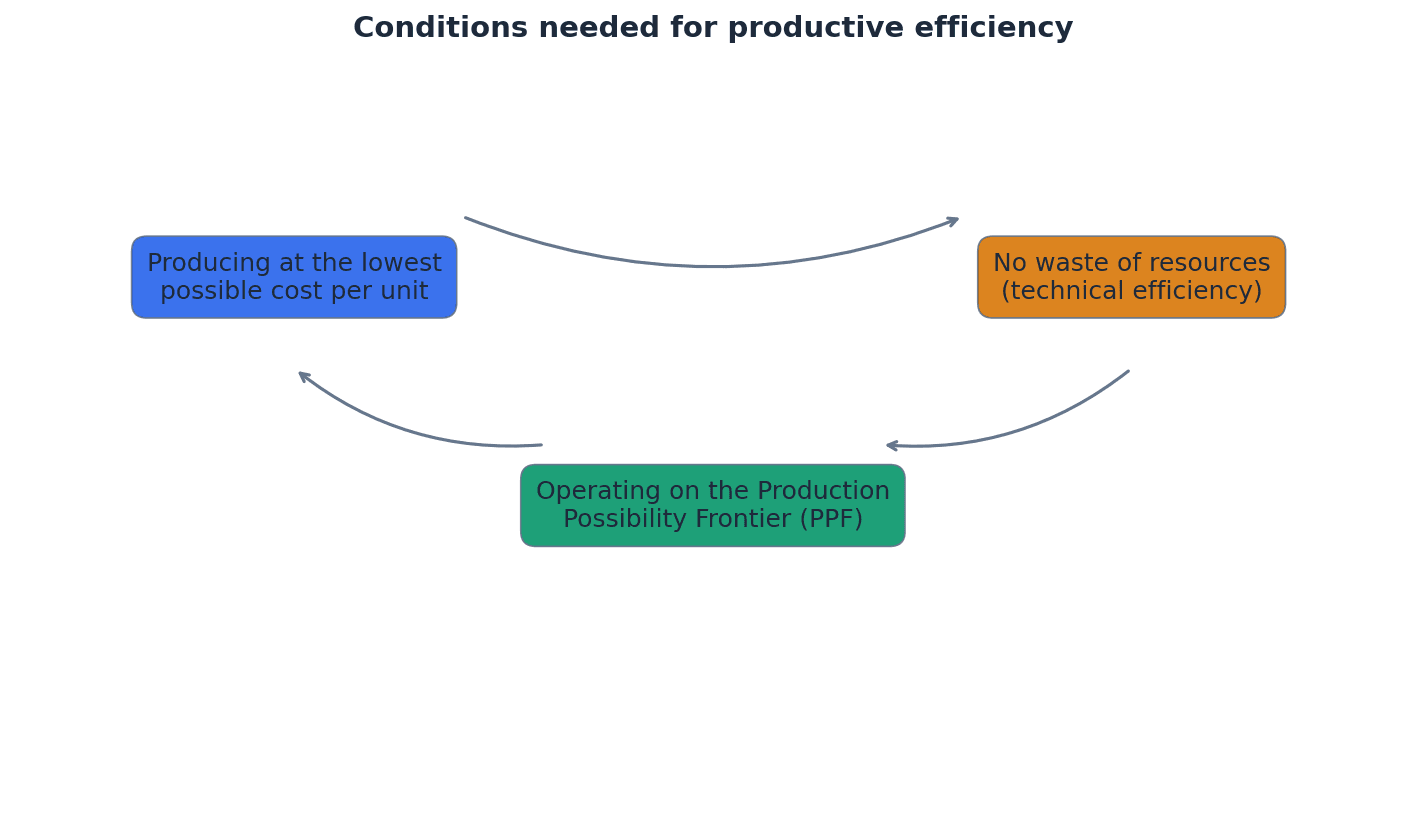

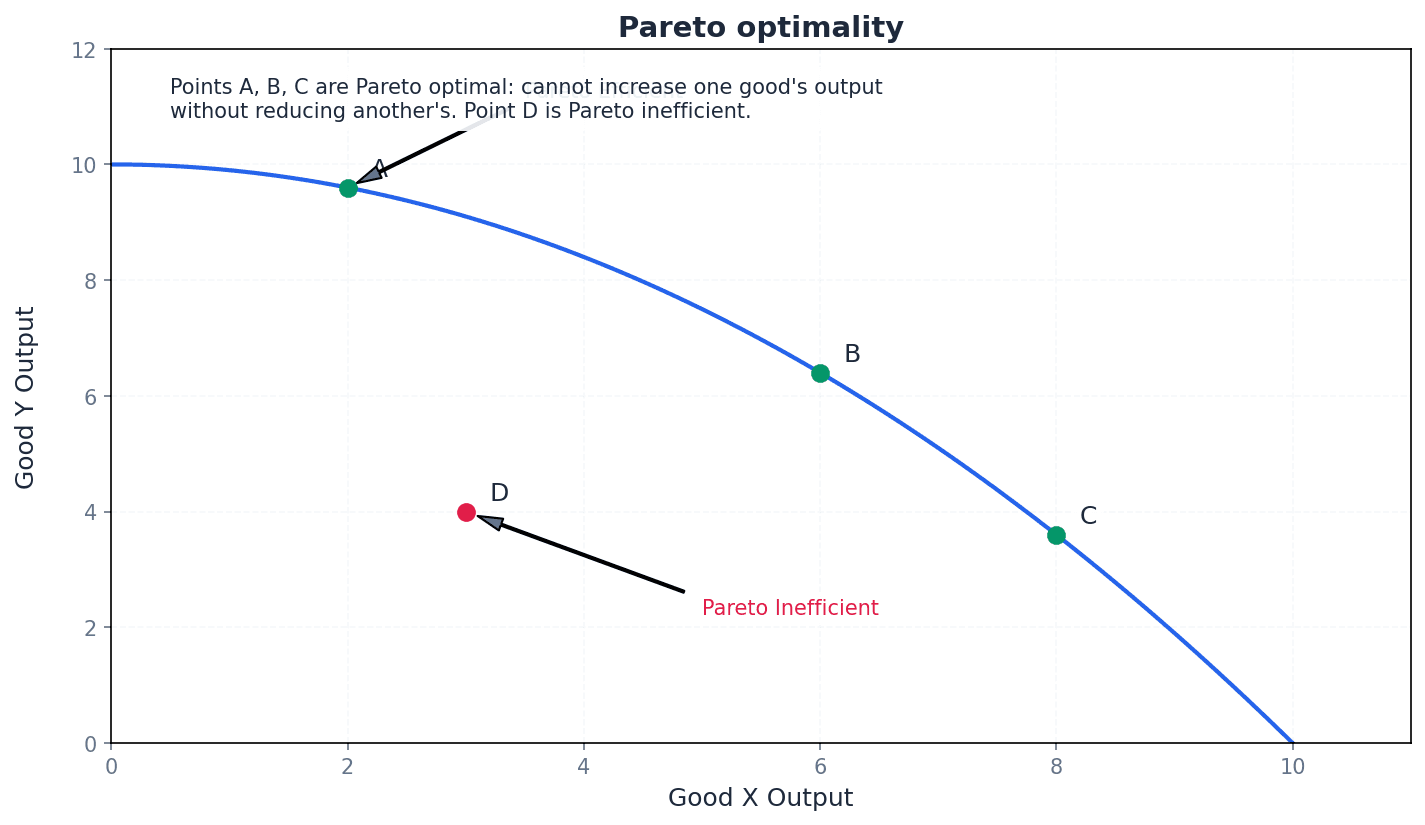

Points located directly on the production possibility curve represent productively efficient outcomes, meaning all available resources are fully and efficiently utilised. Conversely, any point inside the PPC signifies inefficiency, indicating that resources are either unemployed or underemployed. Points lying outside the PPC are currently unattainable, demonstrating the concept of scarcity due to insufficient resources or technology.

Use precise terminology: 'productively efficient' for points on the curve, 'inefficient' or 'unemployed resources' for points inside, and 'unattainable' for points outside.

A movement along the PPC demonstrates a trade-off, where increasing the production of one good necessitates decreasing the production of another. This trade-off directly illustrates opportunity cost, which is the value of the next best alternative forgone. For example, to produce more capital goods, an economy must give up some consumer goods, and the amount of consumer goods sacrificed is the opportunity cost.

When calculating or explaining opportunity cost, clearly state what is being 'given up' in terms of the other good. For a curved PPC, explain why opportunity cost increases as more of one good is produced (e.g., resources are not equally suited).

The shape of the PPC reflects the nature of opportunity costs. A straight-line PPC indicates a constant opportunity cost, meaning that resources are perfectly adaptable between the production of the two goods. More commonly, the PPC is bowed outwards (concave to the origin), signifying increasing opportunity costs. This occurs because resources are not equally suited to producing both goods, so as more of one good is produced, increasingly less suitable resources must be reallocated, leading to larger sacrifices of the other good.

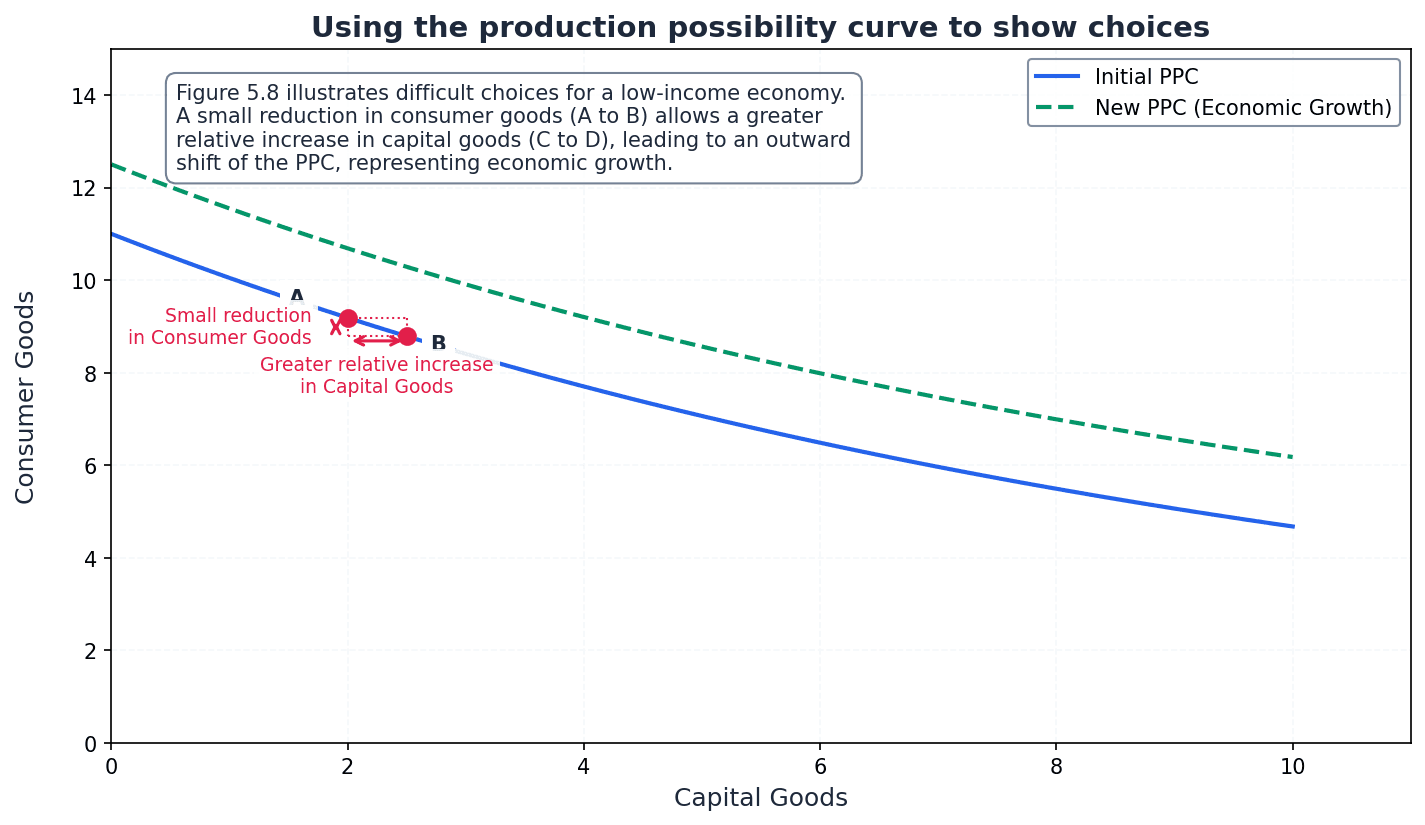

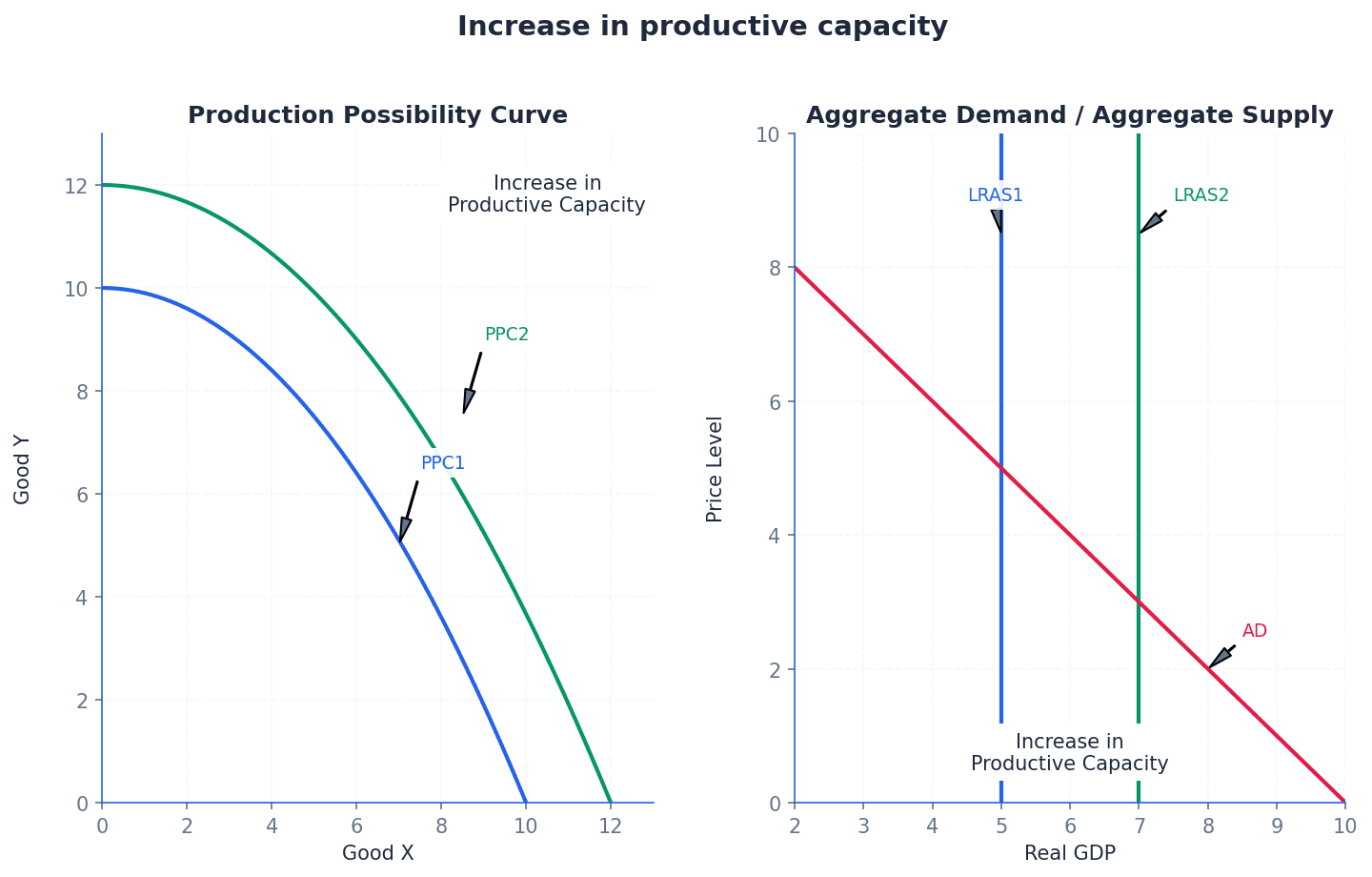

Changes in an economy's productive capacity lead to shifts in the PPC. An outward shift of the curve indicates economic growth, meaning the economy can now produce more of both goods. This is typically caused by an increase in the quantity or quality of resources (e.g., more labour, better education) or advancements in technology. Conversely, an inward shift of the PPC signifies a decrease in productive capacity, perhaps due to events like natural disasters or war.

When explaining shifts in the PPC, explicitly link the shift to a change in the economy's 'productive capacity' and identify whether it's an increase (outward shift) or decrease (inward shift), citing reasons like resource changes or technological advancements.

Students often confuse a movement along the curve (reallocating resources) with a shift of the curve (changing productive capacity).

Students often think the PPC shows what an economy 'should' produce, but actually it only shows what 'can' be produced given resources and technology, highlighting choices and trade-offs.

Always fully label your PPC diagrams: title, both axes (e.g., 'Capital Goods', 'Consumer Goods'), and any points (A, B, C) you refer to in your explanation.

When explaining a shift, you must state the direction (e.g., 'outward shift') and give a valid reason (e.g., 'due to an improvement in technology').

When discussing economic growth, draw a PPC diagram showing an outward shift to illustrate the increase in the economy's productive capacity.

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the Production Possibility Curve (PPC) and stating its primary purpose as a model to illustrate scarcity, choice, and opportunity cost. Briefly outline the key aspects you will discuss, such as its shape, shifts, and implications for an economy.

Conclusion

Summarise the main points, reiterating the PPC's significance as a foundational model for understanding resource allocation and economic choices. Conclude with a final evaluative statement on its usefulness despite its simplifications.

This chapter classifies goods and services based on their characteristics of excludability and rivalry, categorising them into free, private, public, and quasi-public goods. It also introduces merit and demerit goods, explaining how market failures like information asymmetry and low income lead to their underconsumption or overconsumption, often necessitating government intervention.

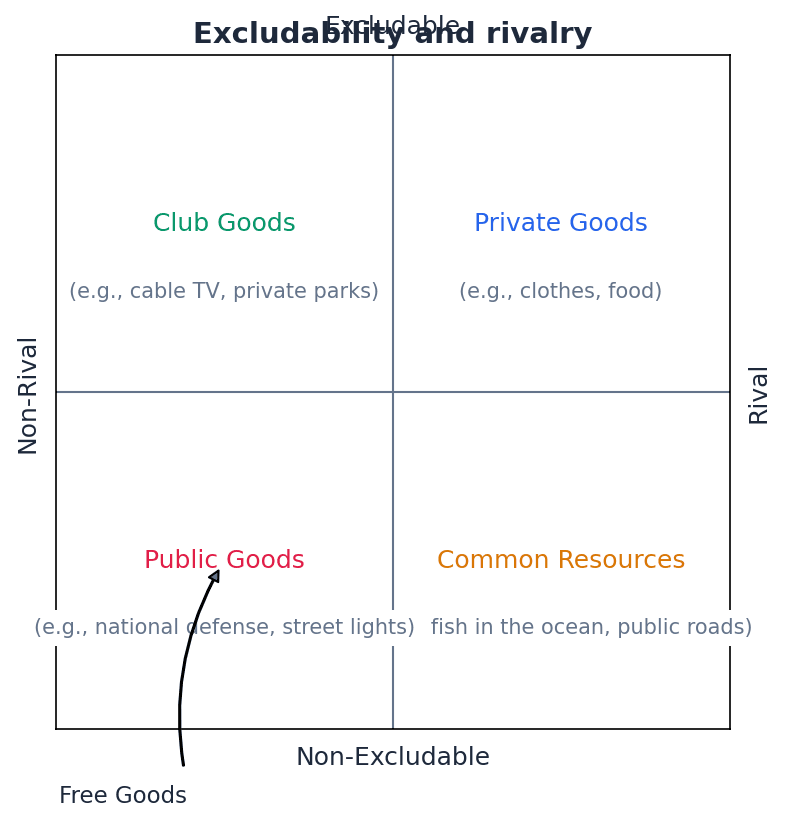

Excludability — A good is excludable (or exclusive) if other consumers can be prevented from using or consuming it.

This characteristic determines if a provider can charge a price for a good and prevent non-payers from using it. For private goods, excludability is typically achieved by charging a price, while non-excludable goods are freely available. For example, a concert ticket is excludable; without it, you cannot enter.

Rivalry — A good is rival if only one person can consume it and in doing so the good is not available for other consumers.

This characteristic describes whether one person's consumption of a good diminishes its availability for others. Most private goods are rivalrous, meaning consumption by one person directly reduces the amount available for others. For instance, eating a slice of pizza is rivalrous; once consumed, it's gone for others.

When explaining excludability, clearly state how prevention of consumption occurs, usually through pricing, for full marks.

Students often think excludability means the good is physically limited, but actually it refers to the ability to prevent consumption by those who don't pay.

Distinguish clearly between 'rival' and 'non-rival' when classifying goods; for public goods, always use 'non-rival' to avoid confusion.

Students often think non-rivalry means there's an infinite supply, but actually it means one person's consumption doesn't reduce the amount available to others.

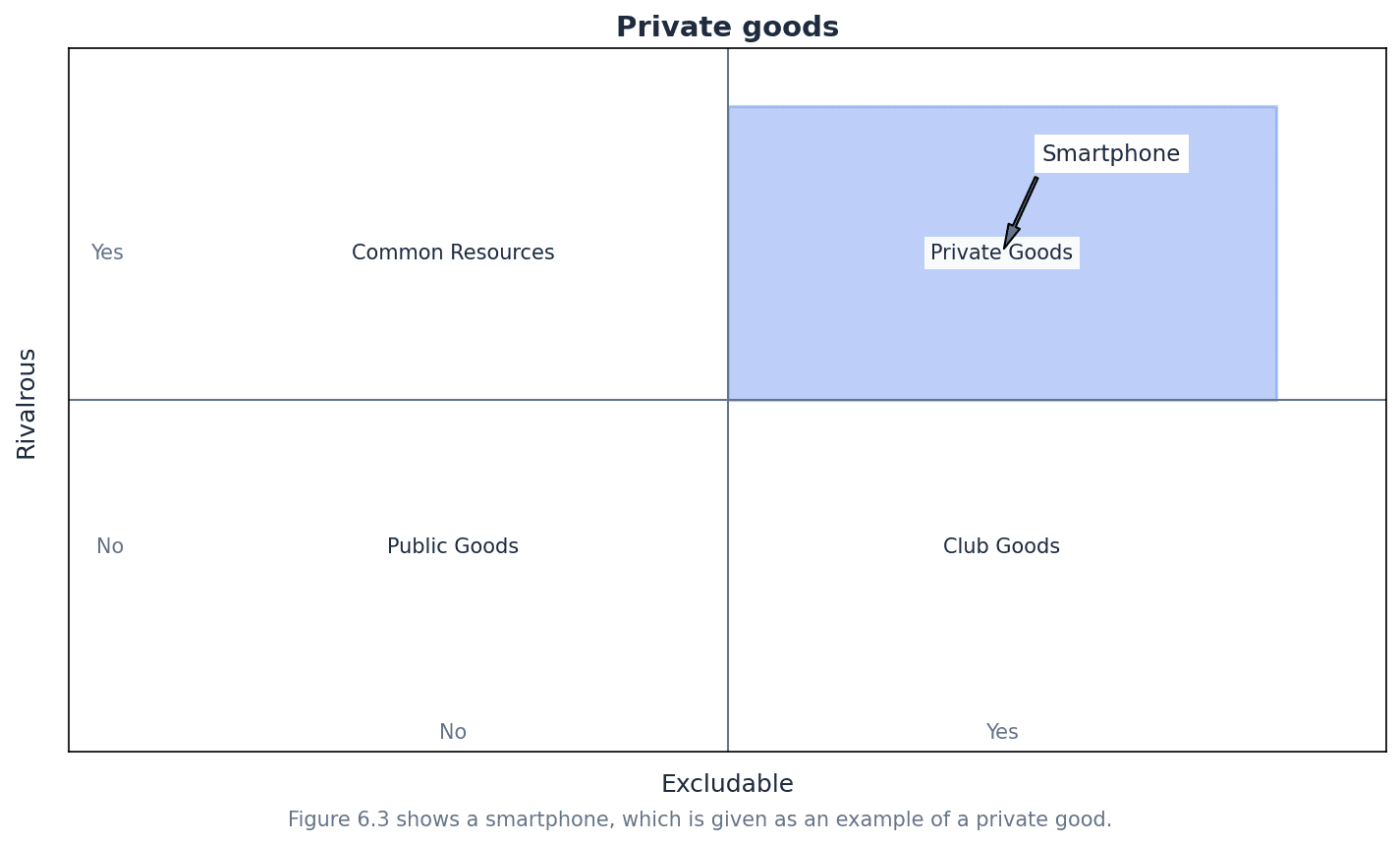

Private goods — Private goods are also known as economic goods since they have a cost in terms of the resources used and are scarce.

These goods are bought and consumed by individuals or firms for their own benefit and possess the characteristics of excludability and rivalry. A price must be charged for private goods due to their scarcity and the resources used in their production. A smartphone is a private good because it's excludable (you pay for it) and rivalrous (only you can use that specific phone).

When asked to define private goods, ensure you explicitly mention both excludability and rivalry as their key characteristics.

Students often think private goods are only luxury items, but actually they include most everyday items like food, clothes, and petrol.

Free goods — Free goods have zero opportunity cost since consumption is not limited by scarcity.

These goods have no prices and, in principle, require no factors of production to produce them. They are rare in economics because most goods involve some form of scarcity or resource use. The air we breathe is a free good; it has no price and its consumption by one person doesn't diminish its availability for others.

When discussing free goods, always link them to the concept of zero opportunity cost and the absence of scarcity.

Students often think 'free' means 'no monetary cost', but actually in economics, it means zero opportunity cost due to unlimited supply.

Public good — A public good has two characteristics: it must be non-excludable and non-rival.

Once a public good is provided for one consumer, it's impossible to stop anyone else from benefiting, and consumption by more people does not reduce the benefit to others. Governments often provide public goods because the free market may fail to do so due to the free rider problem. A lighthouse is a public good, warning all ships (non-excludable) without diminishing the warning for others (non-rival).

Always use 'non-excludable' and 'non-rival' when describing public goods to avoid confusion with private goods characteristics.

Students often confuse public goods with 'government-provided goods', but actually the key is their non-excludable and non-rival characteristics, regardless of who provides them.

Free rider problem — The free rider problem arises where people enjoy the benefits of a public good without having paid for it.

This problem is due to the non-excludability of public goods, making it difficult for private firms to charge for their provision and thus make a profit. Consequently, the free market may not produce public goods even if there is demand. For example, if a private company built a non-toll road, everyone could use it without paying, making it impossible for the company to recover costs.

When explaining the free rider problem, explicitly link it to the non-excludability characteristic of public goods and its consequence for market provision.

Students often think the free rider problem is about people avoiding taxes, but actually it's about the inability to exclude non-payers from consuming a non-excludable good.

The unique characteristics of public goods, specifically non-excludability and non-rivalry, lead to a significant market failure known as the free rider problem. Because individuals can benefit from a public good without paying for it, private firms find it unprofitable to provide such goods. This means that the free market, left to its own devices, will under-provide or completely fail to provide public goods, even if there is a societal demand for them. This necessitates government intervention for their provision, such as national defence or street lighting.

Quasi-public goods — Some goods that may appear to be public goods do not meet both of these characteristics in full.

These goods possess some, but not all, of the characteristics of a pure public good. They might be non-rivalrous but excludable, or non-excludable up to a point but then become rivalrous due to congestion. A toll road is a quasi-public good; it's non-rivalrous until it becomes congested, but it is excludable because you must pay a toll to use it.

When identifying quasi-public goods, clearly state which characteristic (excludability or rivalry) is not fully met and why.

Students often think quasi-public goods are just 'almost public goods', but actually they specifically fail to meet one or both of the non-excludability and non-rivalry criteria fully.

Information failure — Information failure arises because consumers do not recognise how good or bad a particular product is for them: either they do not have the right information or they simply lack some relevant information.

This market failure occurs when consumers make irrational decisions due to incomplete or inaccurate information about the benefits or harmful effects of products. It is a key reason for the underconsumption of merit goods and overconsumption of demerit goods. Not knowing the full health risks of smoking or the long-term benefits of education are examples of information failure.

When explaining information failure, provide specific examples of how consumers might be misinformed or uninformed about a product's true costs or benefits.

Students often think information failure means no information is available, but actually it means consumers either lack relevant information or misinterpret it.

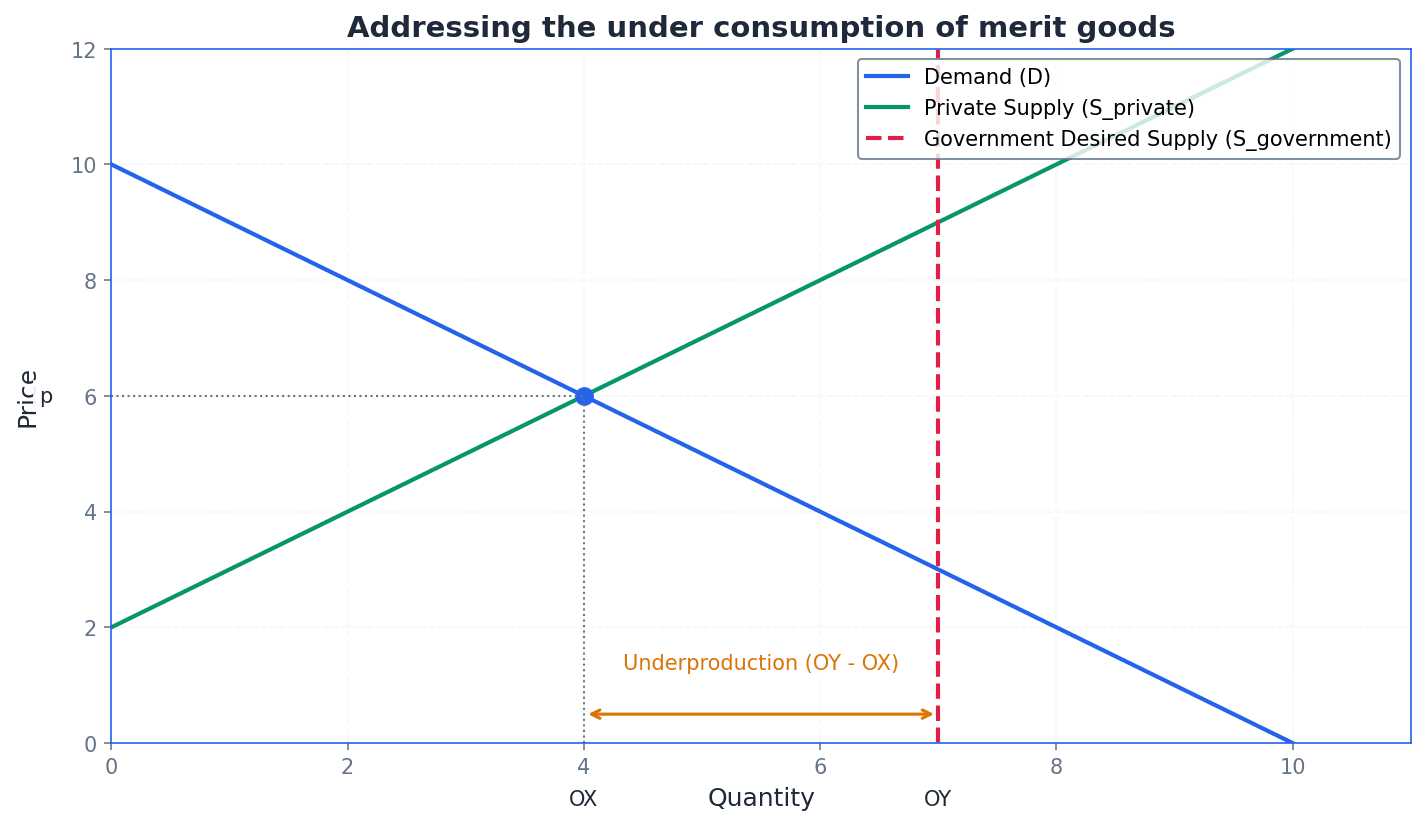

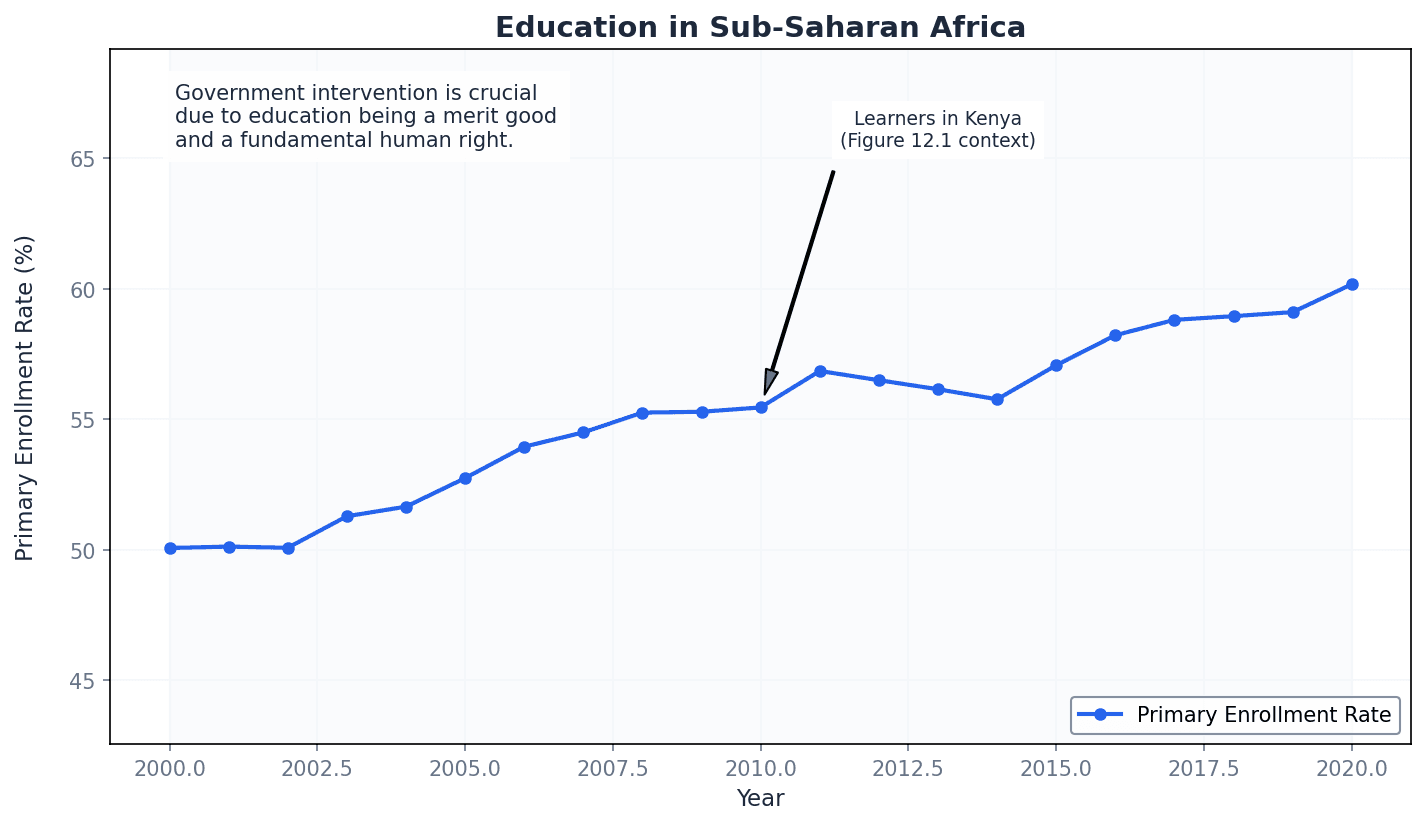

Merit good — A merit good is a good that is thought to be desirable but which is underprovided by the market.

Merit goods are often underconsumed due to information failure (consumers don't fully recognise their benefits) and low income. Governments tend to provide or subsidise merit goods to encourage their consumption, as they often have positive externalities. Education is a merit good; individuals may not fully appreciate its long-term benefits or cannot afford it, leading to underconsumption.

When discussing merit goods, always refer to information failure and underconsumption to provide a complete economic analysis.

Students often think merit goods are simply 'good things', but actually the key is their underprovision and underconsumption in the market due to information failure and/or low income.

Merit goods are typically underconsumed in a free market because consumers suffer from information failure. This means individuals may not fully appreciate the true long-term benefits of consuming these goods, leading to a demand that is below the socially optimal level. Additionally, low income can prevent individuals from affording merit goods, further contributing to their underconsumption. Government intervention, such as subsidies or direct provision, is often necessary to correct this market failure.

Demerit good — A demerit good, on the other hand, is seen as any product that is thought to be undesirable and which is overprovided by the market.

Demerit goods are often overconsumed due to information failure (consumers don't fully recognise their harmful effects) and characteristics like being habit-forming, cheap, and readily available. Governments often intervene to reduce their consumption through taxes, regulations, or advertising restrictions. Cigarettes are a demerit good; consumers may not fully understand the long-term health risks, leading to overconsumption.

When analysing demerit goods, explain how information failure leads to overconsumption and mention government interventions to reduce it.

Students often think demerit goods are just 'bad things', but actually the key is their overprovision and overconsumption in the market due to information failure and often negative externalities.

Demerit goods are typically overconsumed in a free market due to information failure. Consumers may not fully understand the long-term negative consequences or harmful effects associated with these products, leading to a demand that exceeds the socially optimal level. Factors such as their addictive nature, low cost, and easy availability can exacerbate this overconsumption. Governments often intervene with measures like taxes, regulations, or public awareness campaigns to reduce the consumption of demerit goods.

For any public good question, define it using BOTH non-rivalry and non-excludability, and explain what each term means.

Always link the non-excludable nature of public goods directly to the 'free-rider problem' to explain why the market fails to provide them.

When discussing merit or demerit goods, you MUST explain the market failure. State clearly that consumption is not at the socially optimal level because of information failure.

Use a clear, real-world example to illustrate each type of good (e.g., Public Good = national defence; Quasi-Public Good = a busy motorway; Merit Good = vaccination).

In evaluation, consider how the classification of a good can change. A quiet road is non-rival (quasi-public), but at rush hour it becomes rival (private).

Advantages & Disadvantages

Government Provision of Public Goods

Government Intervention for Merit Goods

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining the core concepts of excludability and rivalry, stating their importance in classifying goods. Briefly outline the types of goods to be discussed (private, public, merit, demerit) and mention the role of market failure, particularly information failure, in their provision.

Conclusion

Summarise the main classifications of goods and the market failures associated with public, merit, and demerit goods. Reiterate the importance of understanding these classifications for effective economic policy and the role of government in addressing market inefficiencies.

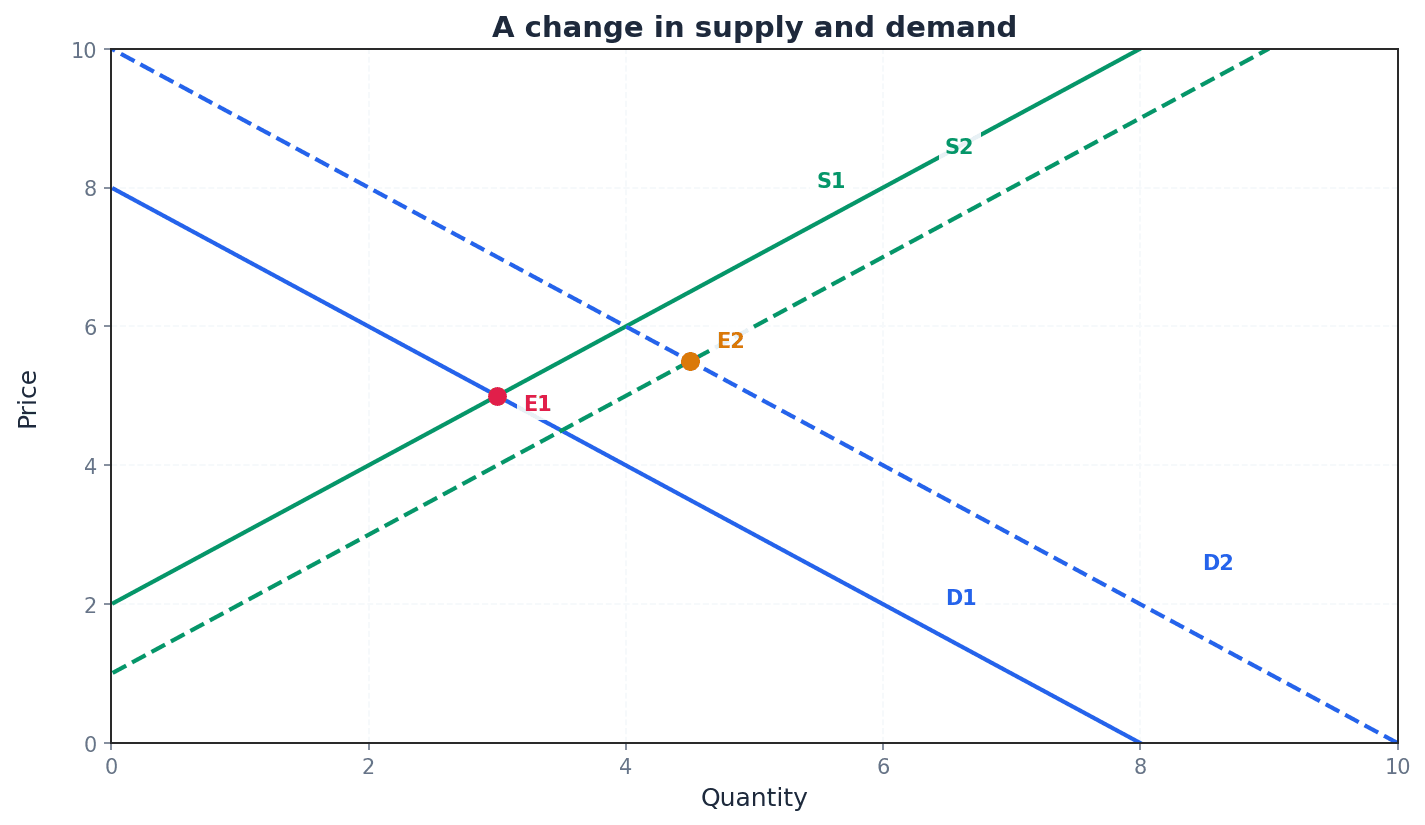

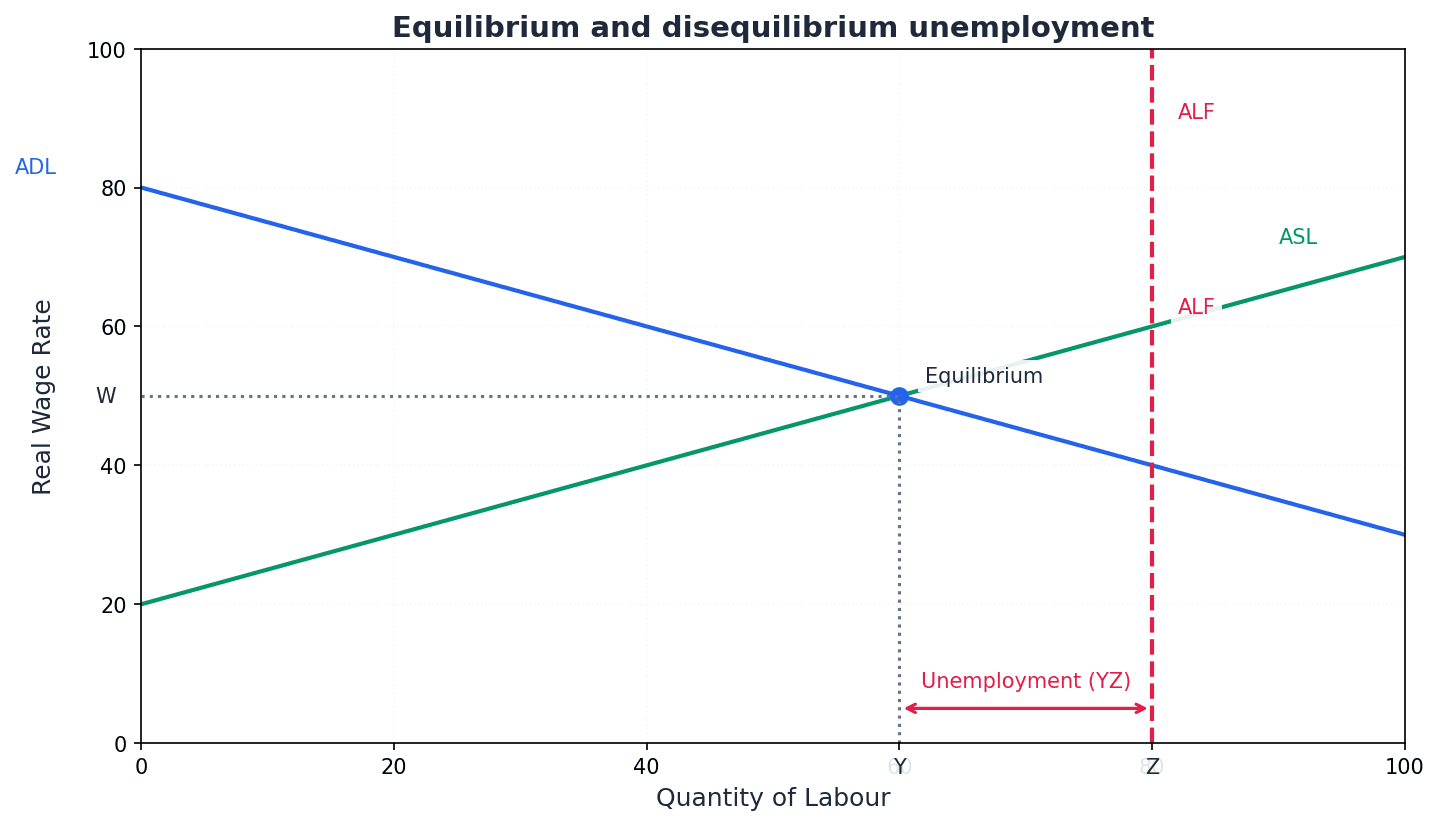

This chapter introduces the fundamental concepts of demand and supply, explaining how they interact within markets through the price mechanism. It defines effective demand and supply, detailing the various factors that influence each, and distinguishes between movements along and shifts of the demand and supply curves.

notional demand — Notional demand refers to buyers wanting a product.

This is the initial desire for a product, without necessarily considering the ability to purchase it. For example, you might have a notional demand for a luxury yacht, meaning you want one, but without the money to buy it, it doesn't become effective demand.

effective demand — Effective demand is notional demand for a product backed by purchasing power.

This is the actual demand that economists refer to, as it represents a real intention to buy, supported by the financial means to do so. Sellers only respond to effective demand. If you want a concert ticket and have the money to buy it, your desire becomes effective demand, and you can actually purchase it.

Students often think 'demand' is just wanting something, but actually economists refer to effective demand, which includes the ability to pay.

Always refer to 'effective demand' when discussing demand in economic contexts, as it implies both willingness and ability to purchase.

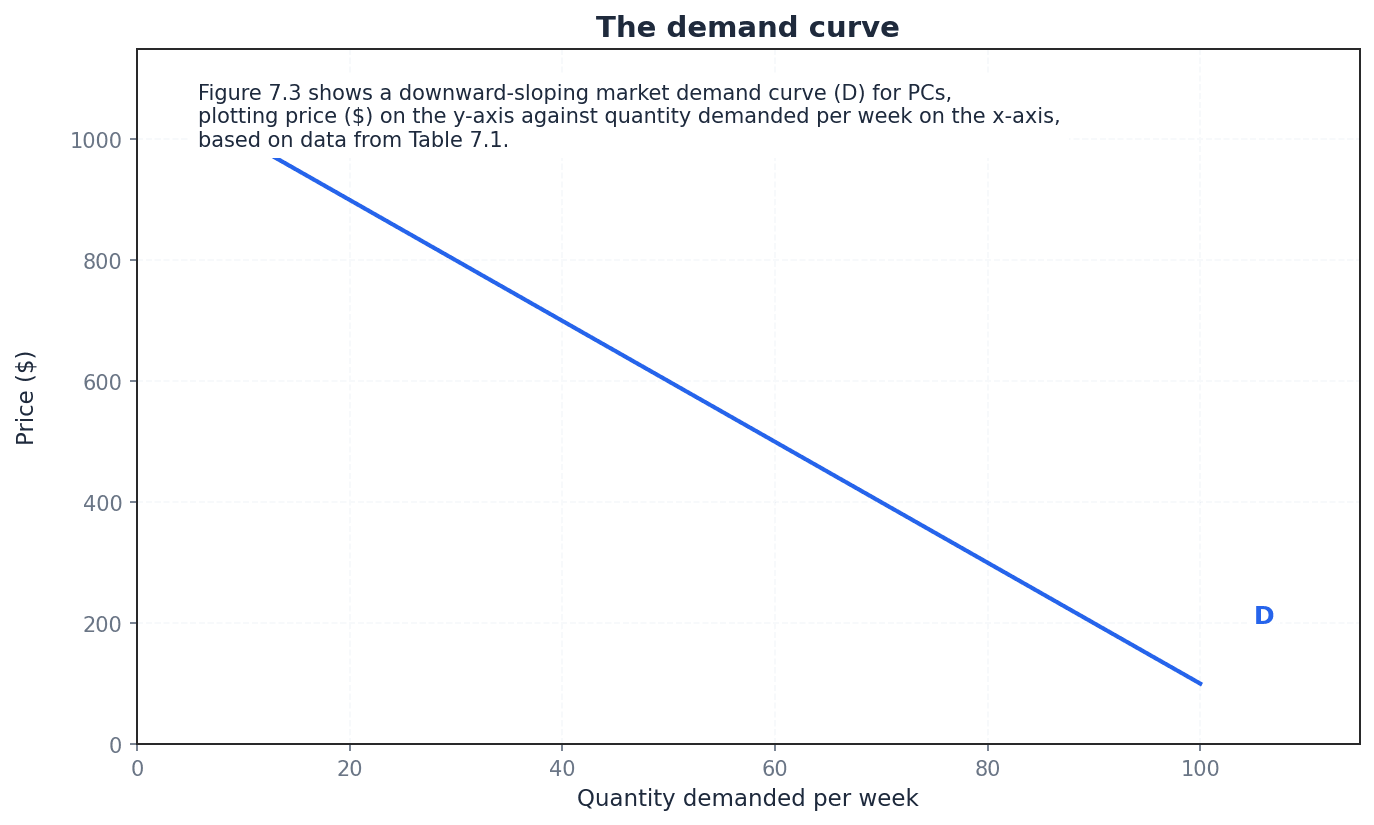

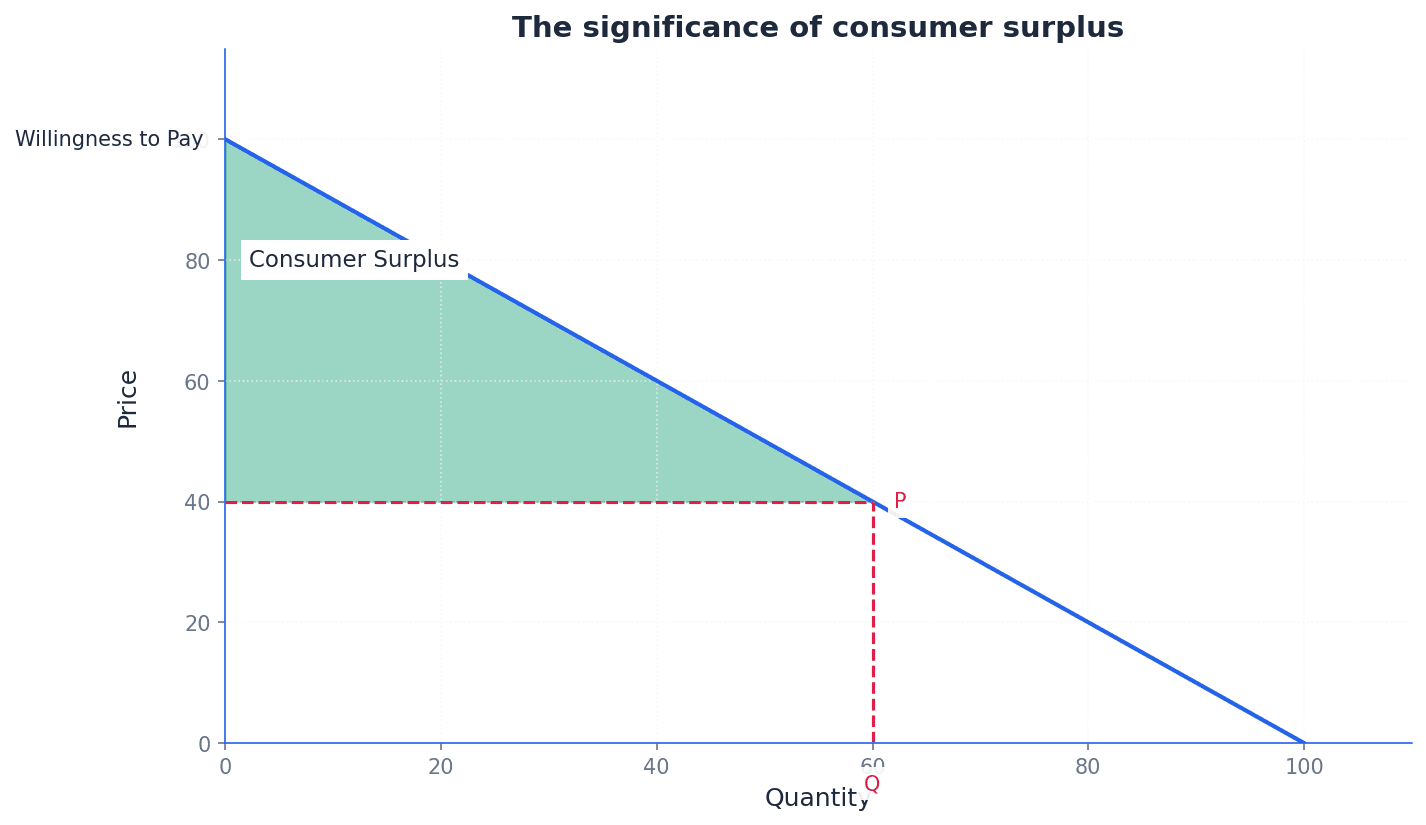

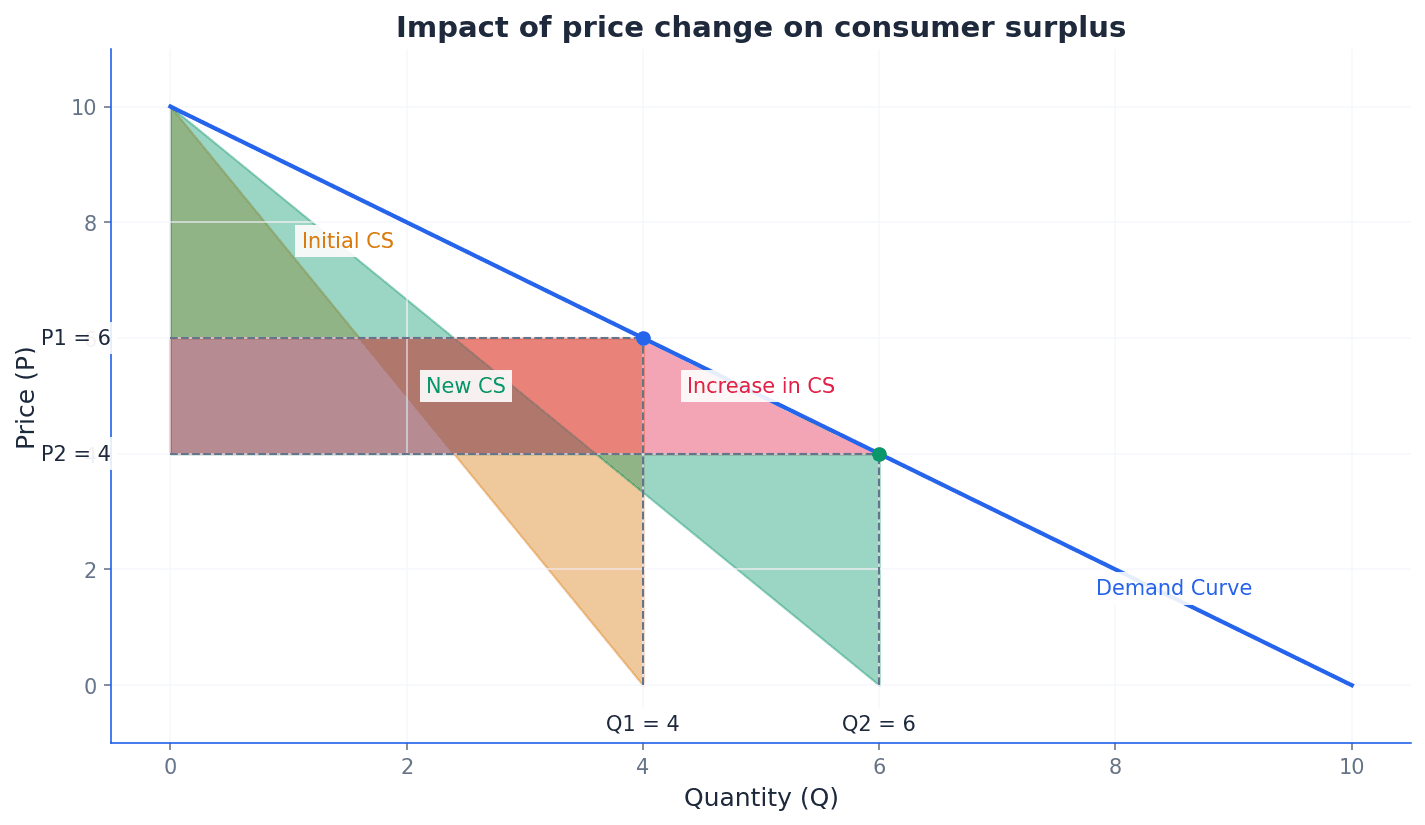

Demand — Demand refers to the quantity of a product that buyers are willing and able to buy at different prices per period of time, ceteris paribus or other things equal.

This definition highlights that demand is not just about wanting a product, but also having the purchasing power to acquire it. It's measured over a specific time period and assumes all other influencing factors remain constant. Imagine you really want a new video game, but you only have enough money to buy it if it's on sale. Your effective demand only kicks in when the price drops to what you're willing and able to pay.

When defining demand, ensure you include 'willing and able to buy', 'at different prices', and 'per period of time', along with 'ceteris paribus' for full marks.

demand schedule — A demand schedule is a data set that represents consumers’ preferences and the quantity of a product that people are willing and able to buy at various prices per period of time, ceteris paribus.

This table of data forms the basis for plotting a demand curve, showing the inverse relationship between price and quantity demanded. It aggregates individual preferences into a market view. Think of a menu at a restaurant that lists different prices for a dish and how many people would order it at each price – that's like a demand schedule.

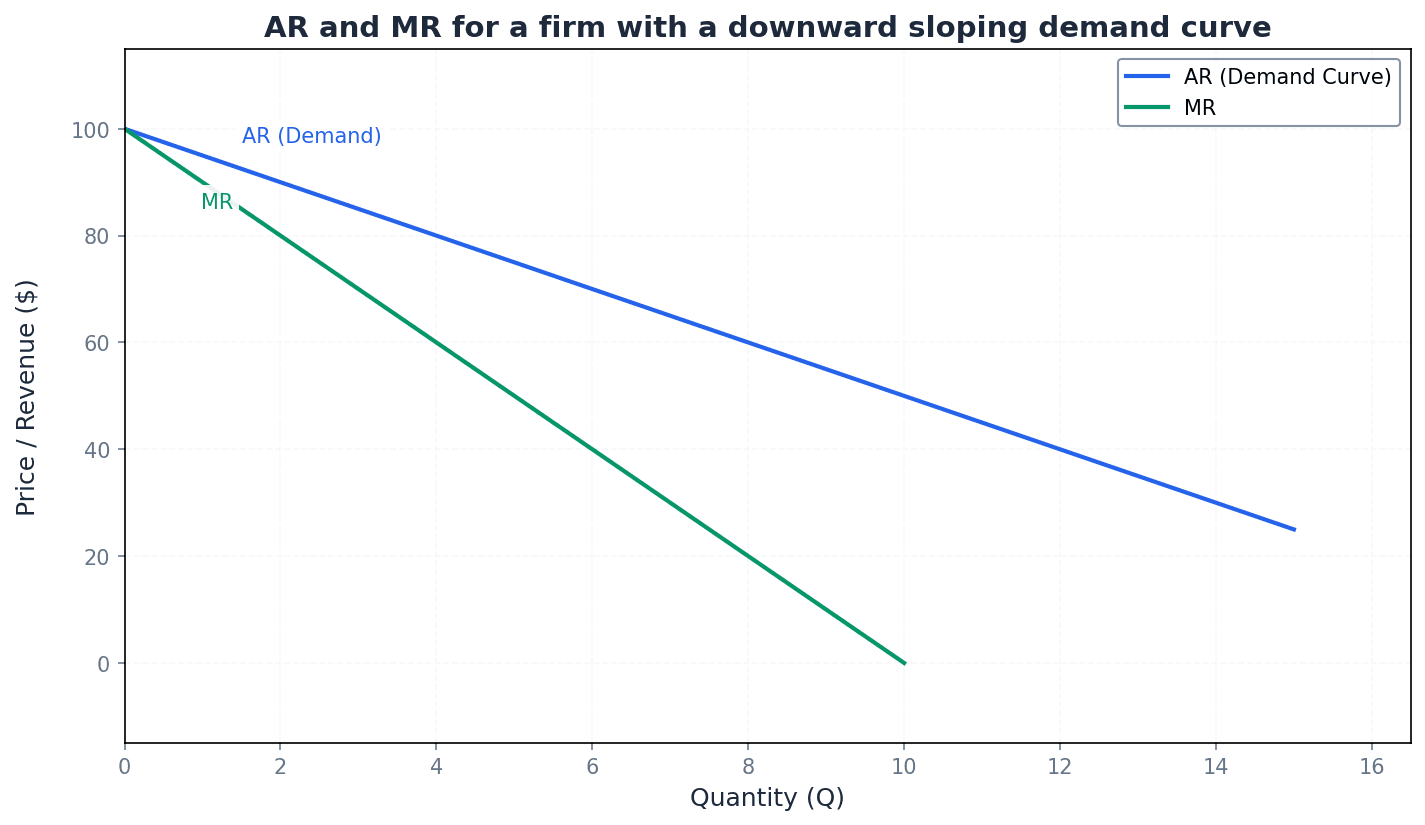

demand curve — A demand curve (D) is a graphical representation of the quantity of a product that buyers are willing and able to buy at different prices per period of time, ceteris paribus.

It typically slopes downwards from left to right, illustrating the inverse relationship between price and quantity demanded. It can represent individual or market demand. Imagine a slide at a playground: as the price (height) goes down, more people (quantity demanded) are willing to 'slide' or buy.

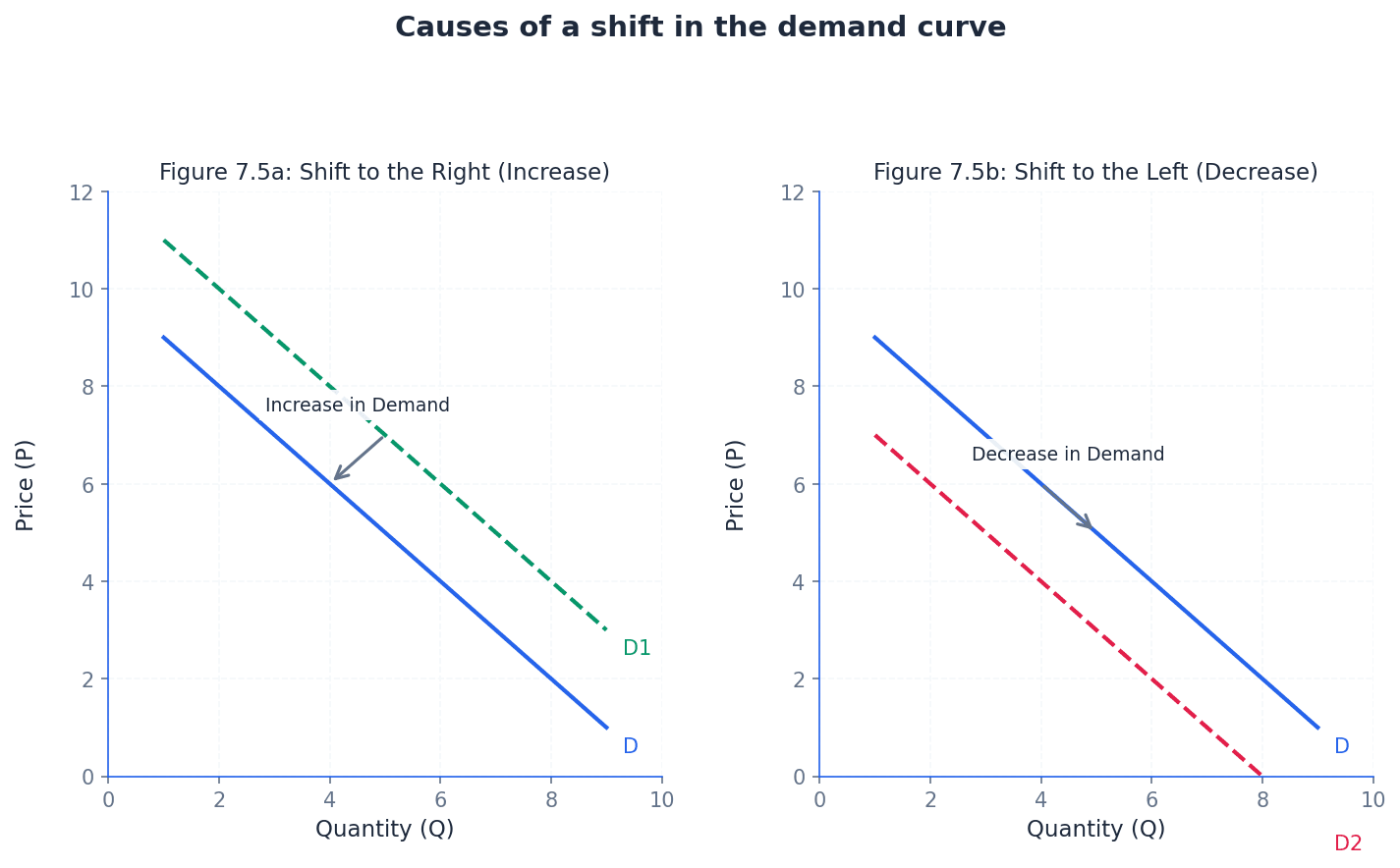

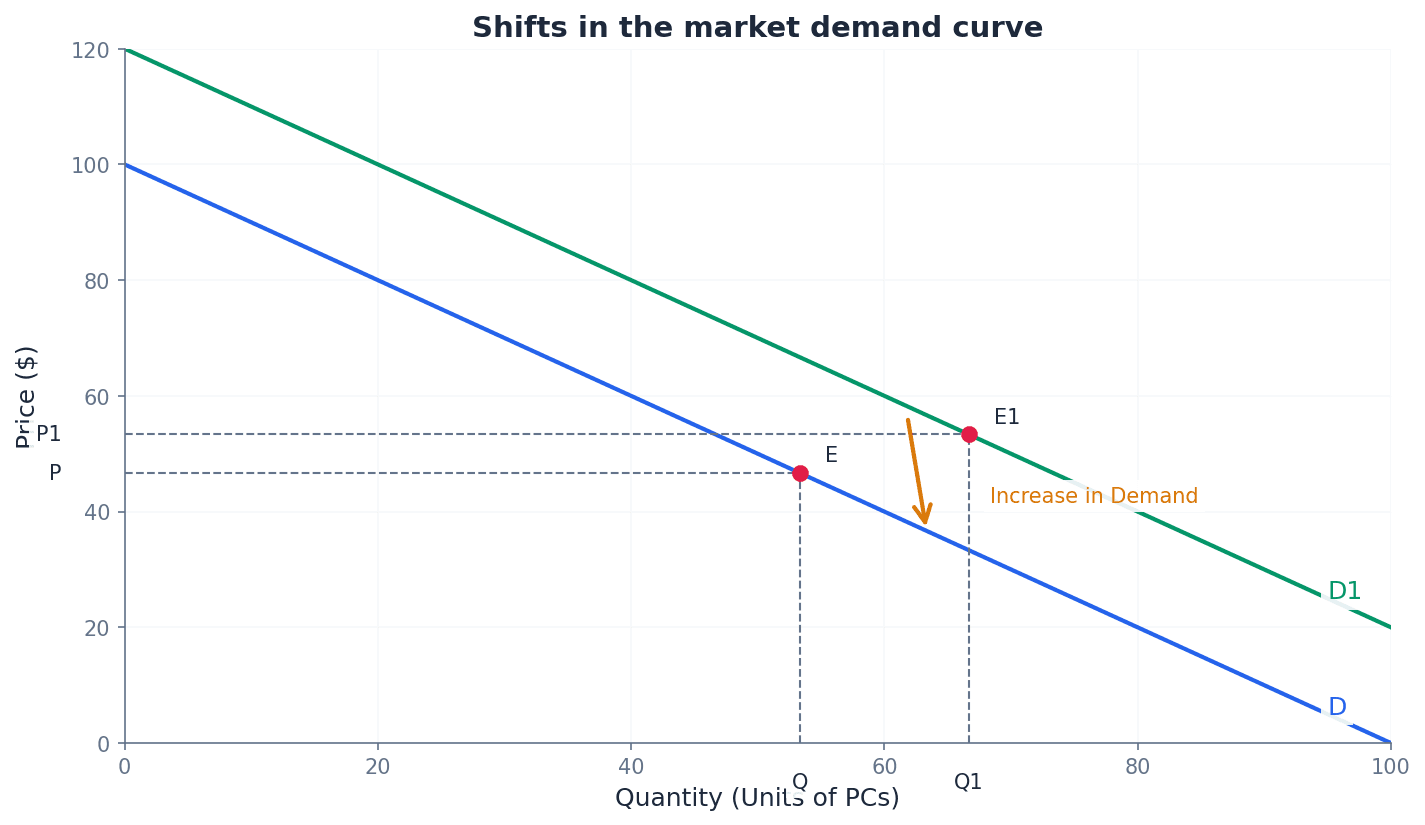

Beyond the product's own price, several non-price factors can influence the overall demand for a good or service, causing the entire demand curve to shift. These include changes in consumer income, the prices of related products, and government policy.

normal goods — Normal goods are goods and services for which there is a positive relationship between income and demand.

As consumers' incomes rise, they tend to buy more of these goods, and conversely, demand falls when income decreases. Most products fall into this category. When you get a pay raise, you might buy more restaurant meals or better quality clothing; these are normal goods.

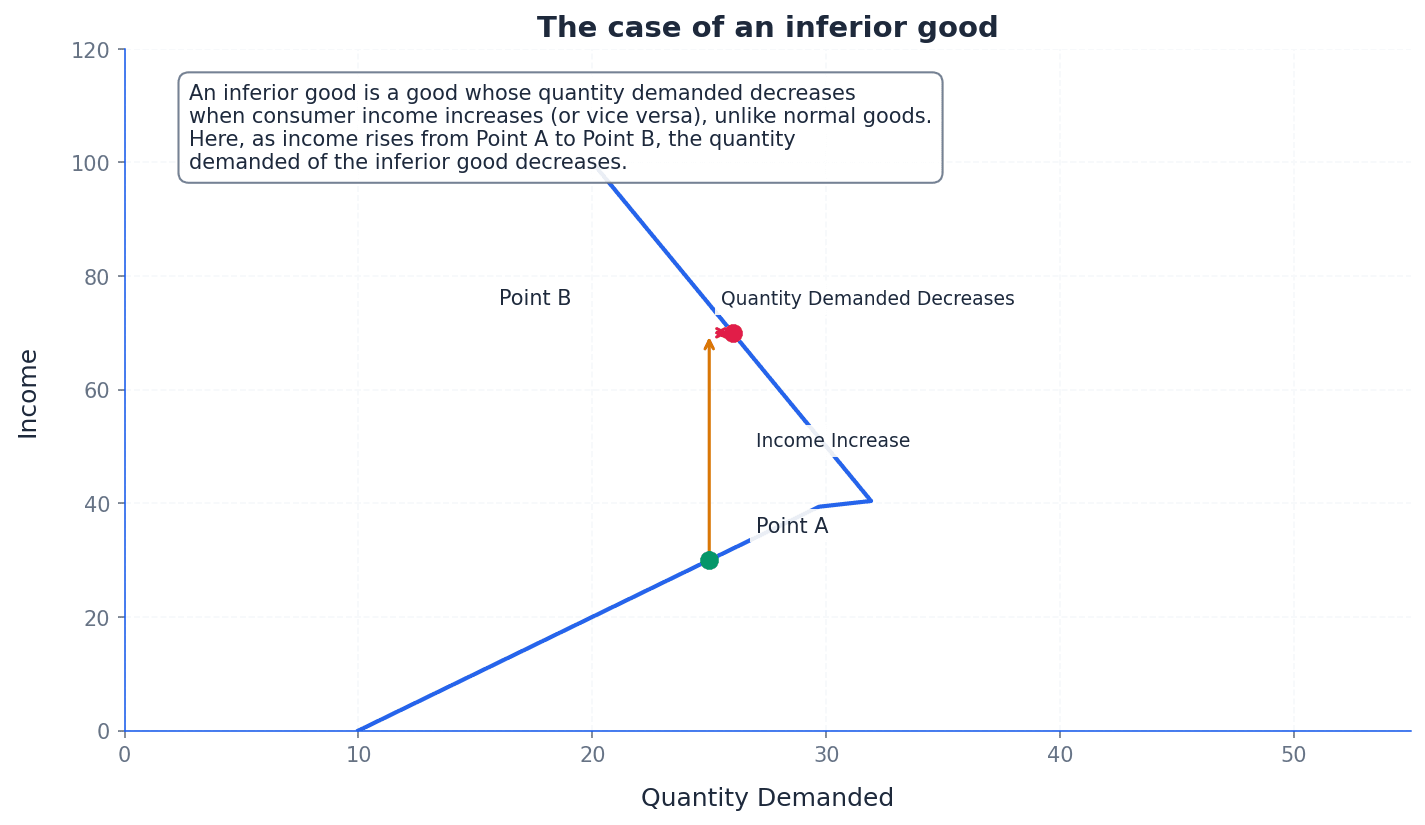

inferior goods — Inferior goods are products for which there is a negative relationship, with less being purchased as income rises.

When income increases, consumers switch away from these goods to higher-quality alternatives. During recessions or income falls, demand for inferior goods tends to increase. If your income increases, you might stop buying cheap packet noodles and instead buy fresh meat and vegetables; the noodles are the inferior good.

Students often think 'inferior' means poor quality, but actually it refers to how demand changes with income, not necessarily the inherent quality.

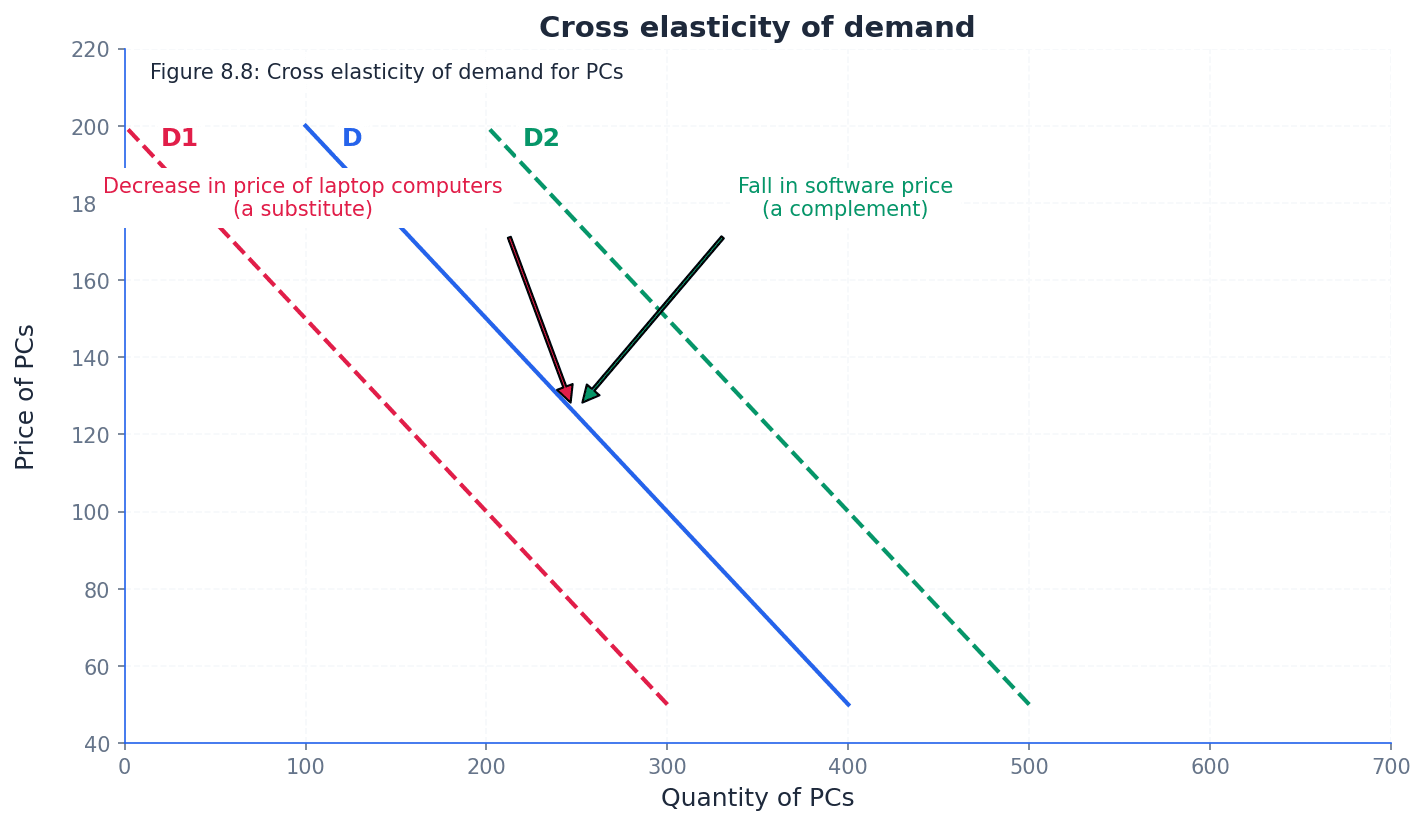

Substitutes — Substitutes are alternative goods that satisfy the same want or need.

A change in the price of one substitute is likely to affect the demand for the other. The closer the substitutes, the greater the impact on demand. If the price of Coca-Cola goes up, some consumers might switch to Pepsi because they both satisfy the same thirst; they are substitutes.

Complements — Complements are goods that have a joint demand as they add to the satisfaction that consumers get from another product.

A change in the price or availability of one complementary good will affect the demand for the other. They are consumed together. Cars and petrol are complements; if the price of petrol rises significantly, people might drive less, reducing the demand for cars.

Students often confuse substitutes with complements, but actually substitutes are alternatives, while complements are used together.

It is crucial to distinguish between a movement along the demand curve and a shift of the entire curve. A change in the product's own price causes a movement along the demand curve, representing a change in the quantity demanded. Conversely, a change in any non-price factor affecting demand causes the entire demand curve to shift.

extension of demand — An extension of demand is an increase in the quantity demanded in response to a change in the price of the product.

This is represented by a downward movement along a stationary demand curve. It occurs when the price of the good falls, leading consumers to buy more. If a shop lowers the price of your favourite chocolate bar, you might buy more of them; this is an extension of demand.

contraction of demand — A contraction of demand is a decrease in the quantity demanded in response to a change in the price of the product.

This is represented by an upward movement along a stationary demand curve. It occurs when the price of the good rises, leading consumers to buy less. If the price of cinema tickets goes up, you might go to the cinema less often; this is a contraction of demand.

Students often confuse a movement along the demand curve with a shift of the demand curve, but actually a movement is due to price change, while a shift is due to non-price factors.

Be precise with your language. Use 'extension' or 'contraction' for movements along a curve, and 'increase' or 'decrease' for shifts of a curve.

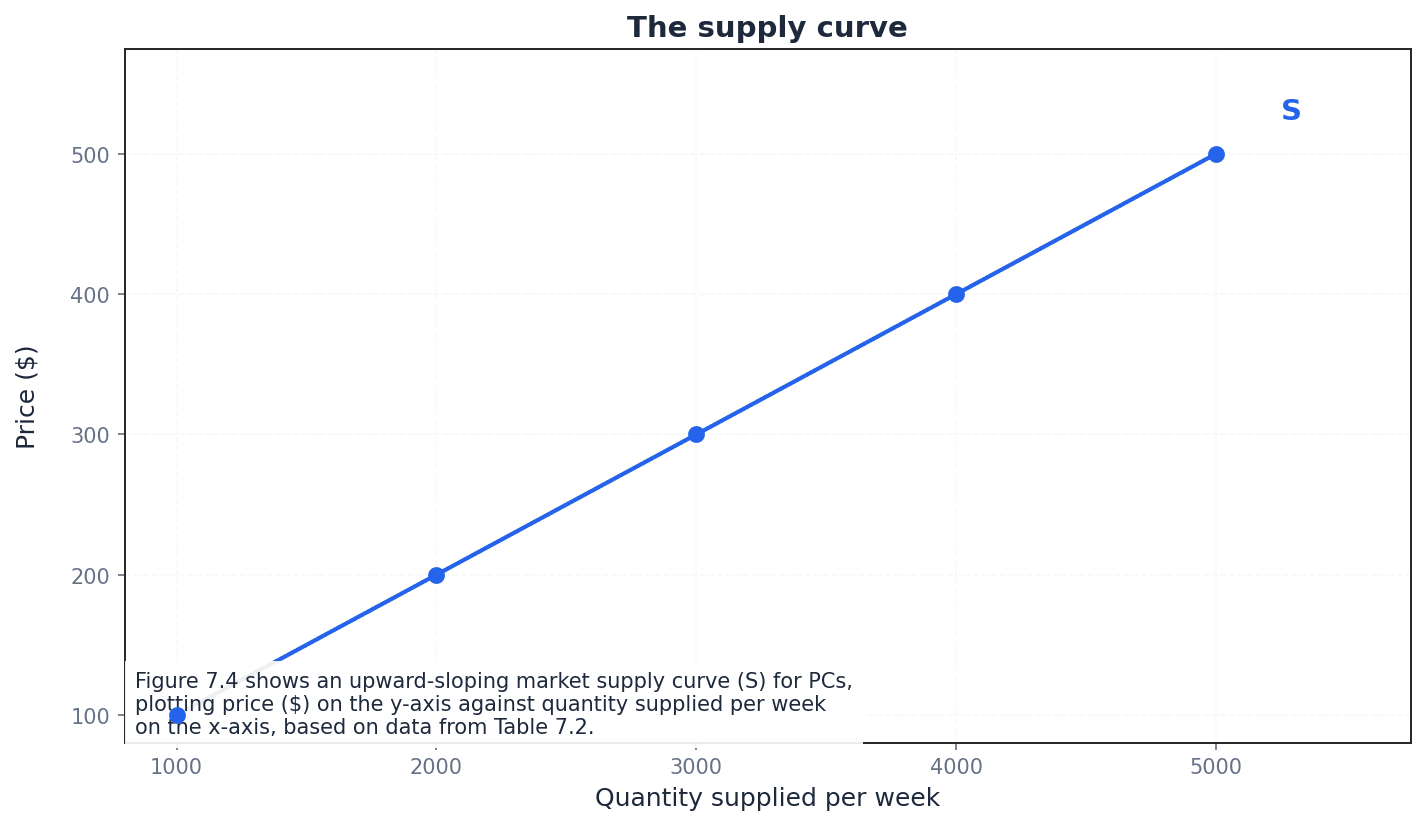

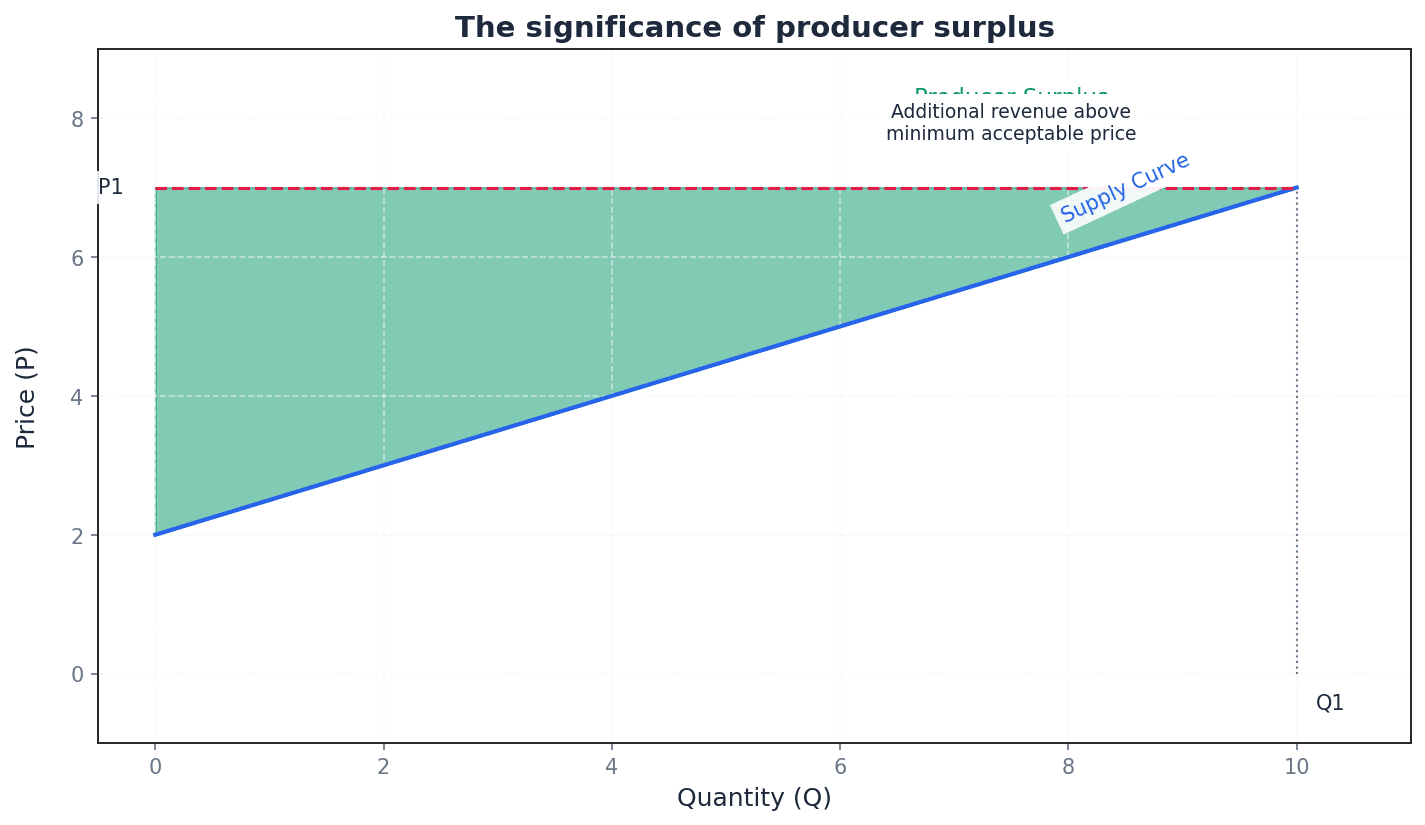

Supply — Supply refers to the quantity of a product that suppliers are willing and able to sell at different prices over a period of time, ceteris paribus or other things equal.

This definition emphasizes that suppliers must be both willing (motivated by profit) and able (have the resources) to sell. It's measured over a specific time period and assumes other factors are constant. A baker is willing and able to supply more bread if the price per loaf increases, as it becomes more profitable for them.

Ensure your definition of supply includes 'willing and able to sell', 'at different prices', and 'over a period of time', along with 'ceteris paribus'.

supply curve — A supply curve (S) is a graphical representation of the quantity of a product that suppliers are willing and able to sell at different prices over a period of time, ceteris paribus.

It typically slopes upwards from left to right, illustrating the positive relationship between price and quantity supplied. It can represent individual firm supply or market supply. Imagine climbing a hill: as the price (height) goes up, producers (quantity supplied) are willing to 'climb higher' or supply more.

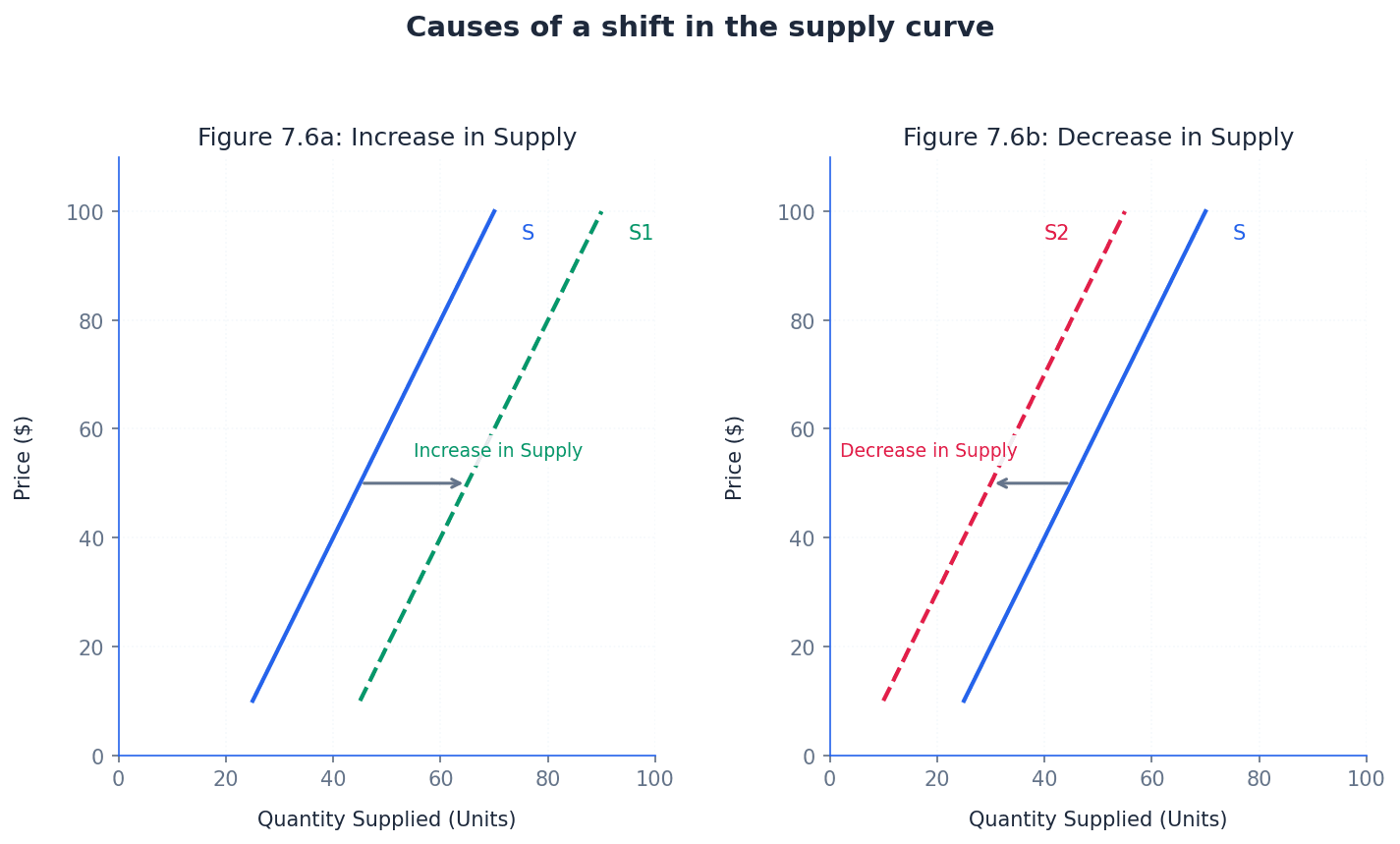

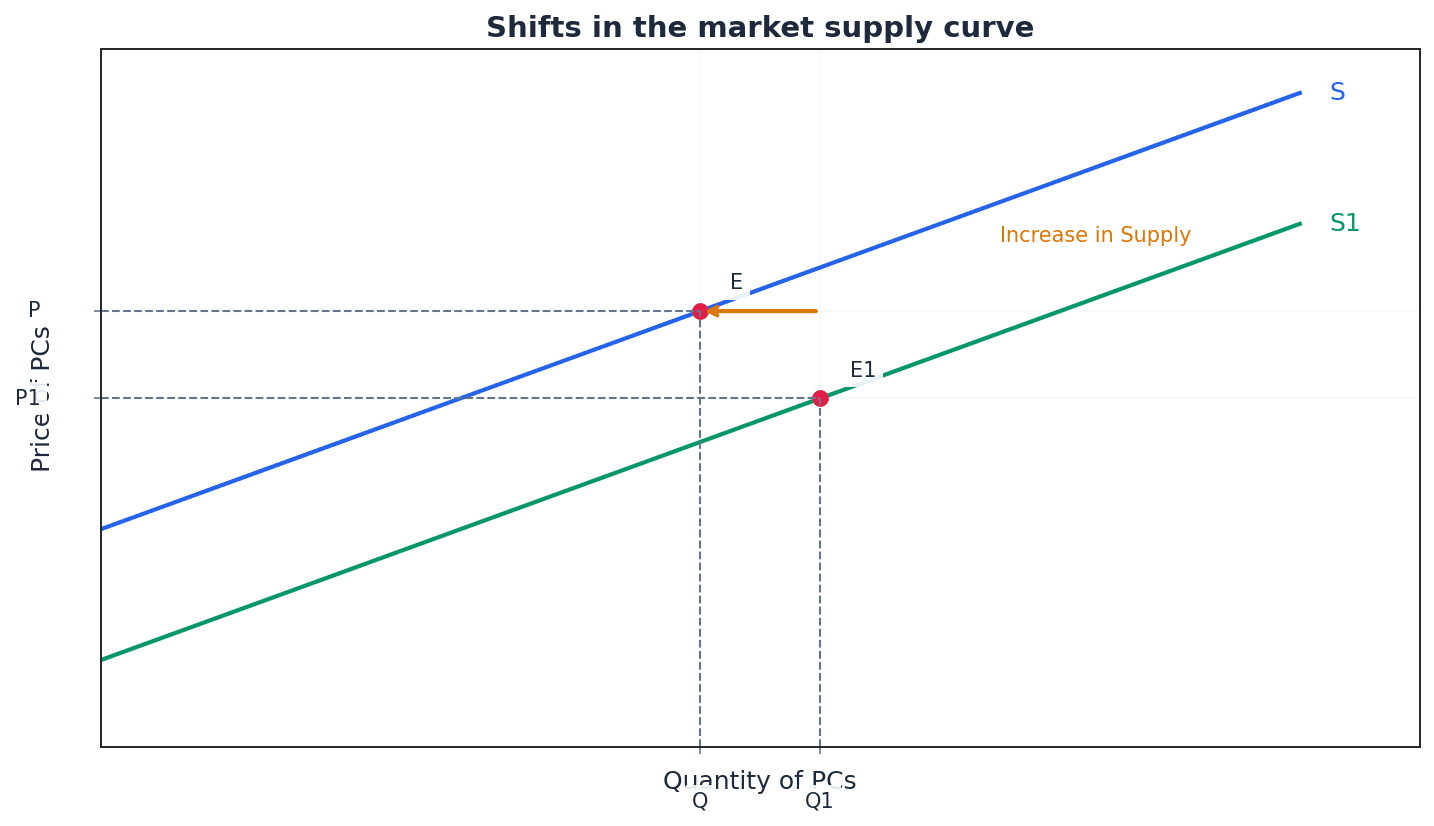

Similar to demand, supply is influenced by factors other than the product's own price. These non-price factors, such as changes in the costs of production or government policy, can cause the entire supply curve to shift, indicating a change in the overall willingness and ability of producers to sell at various prices.

Just as with demand, a change in the product's own price leads to a movement along the supply curve, known as a change in quantity supplied. However, a change in any non-price factor affecting supply will cause the entire supply curve to shift, representing a change in supply.

extension of supply — An extension of supply is an increase in the quantity supplied in response to a change in the price of the product.

This is represented by an upward movement along a stationary supply curve. It occurs when the price of the good rises, incentivizing producers to supply more. If the price farmers get for their corn increases, they might plant more corn next season; this is an extension of supply.

contraction of supply — A contraction of supply is a decrease in the quantity supplied in response to a change in the price of the product.

This is represented by a downward movement along a stationary supply curve. It occurs when the price of the good falls, making it less profitable for producers to supply as much. If the price of milk falls significantly, dairy farmers might reduce their herd size or supply less milk; this is a contraction of supply.

Students often confuse a movement along the supply curve with a shift of the supply curve, but actually a movement is due to price change, while a shift is due to non-price factors.

Clearly label axes (Price, Quantity) and the curve (D or S) when drawing; ensure you understand that a change in price causes a movement along the curve, not a shift.

When drawing a shift, use arrows and label the new curve clearly (e.g., D1 to D2) to show the direction of change.

When explaining a shift, always explicitly state the non-price factor that caused it.

Advantages & Disadvantages

The Price Mechanism

Government Intervention in Markets (e.g., taxes, subsidies)

Evaluation Starters

Essay Structure Guide

Introduction

Begin by defining demand and supply, highlighting the importance of 'effective demand' and 'ceteris paribus'. Briefly state how the price mechanism uses these forces to allocate resources.

Conclusion

Summarise the key role of demand and supply in determining market prices and quantities. Reiterate the importance of understanding the distinction between movements and shifts for economic analysis.

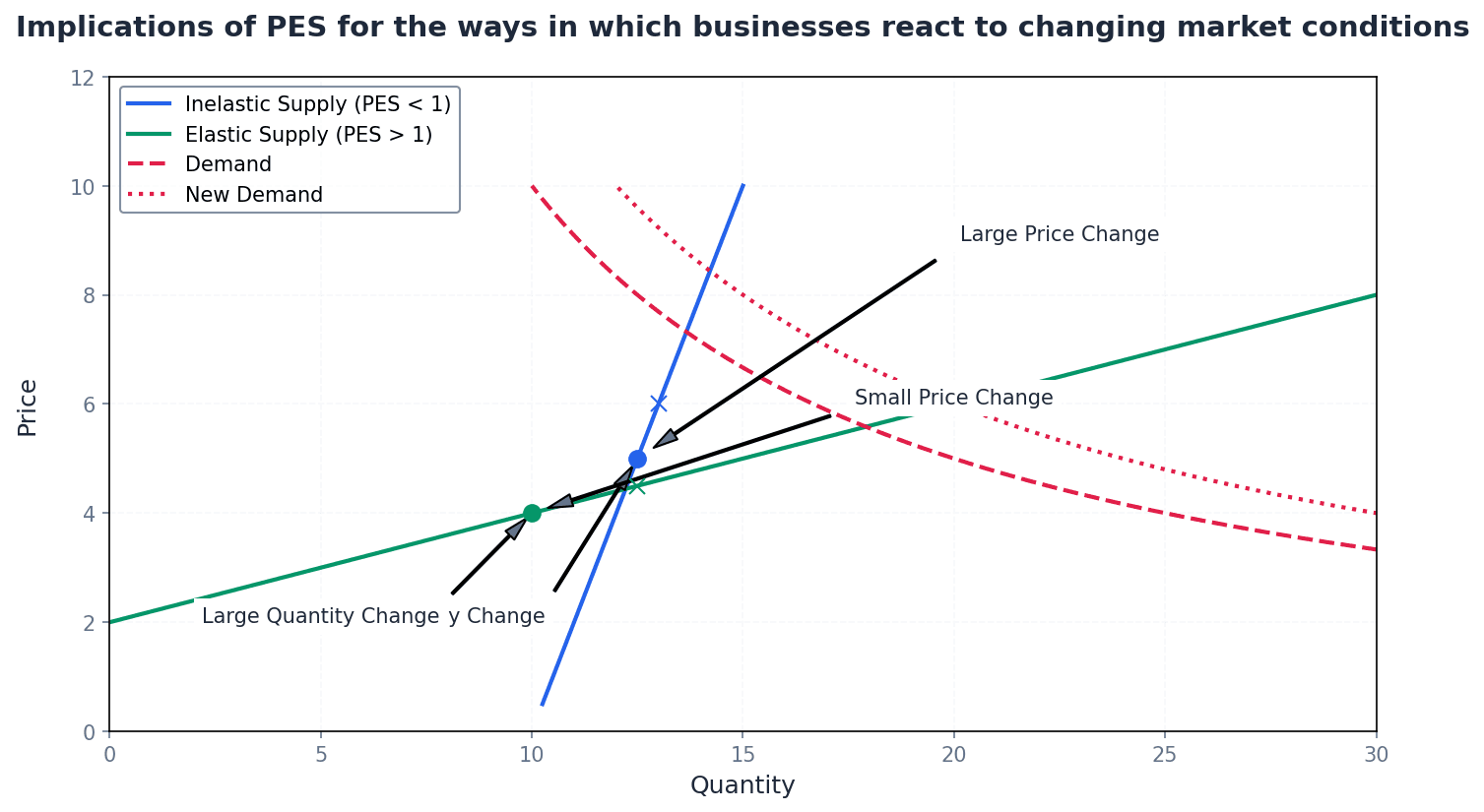

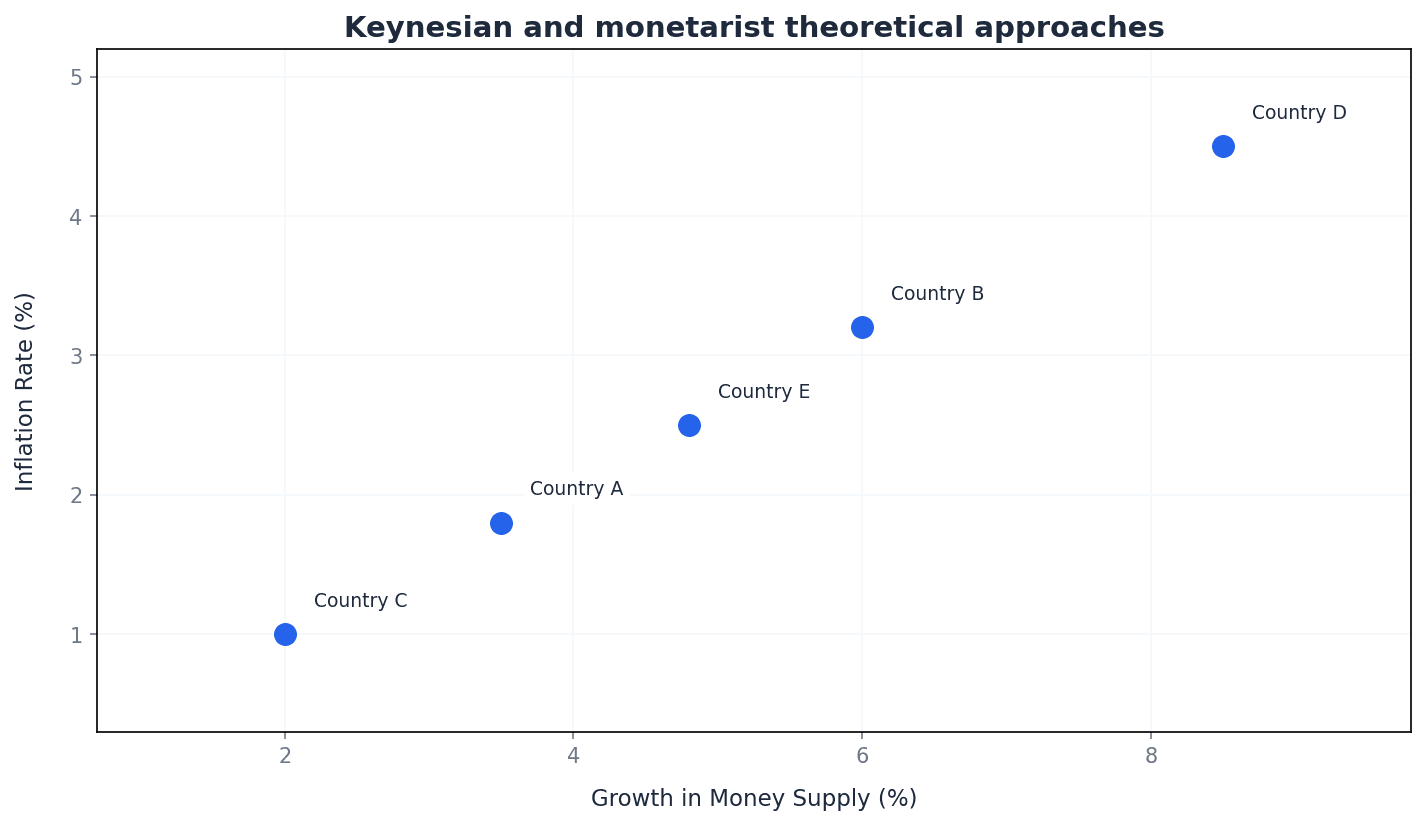

This chapter explores the concept of elasticity, which measures the responsiveness of quantity demanded to changes in price, income, or the price of related goods. It defines and explains Price Elasticity of Demand (PED), Income Elasticity of Demand (YED), and Cross Elasticity of Demand (XED), including their calculation, interpretation, and factors affecting them. Understanding these elasticities is crucial for businesses and governments in making informed decisions regarding pricing, revenue, and policy.

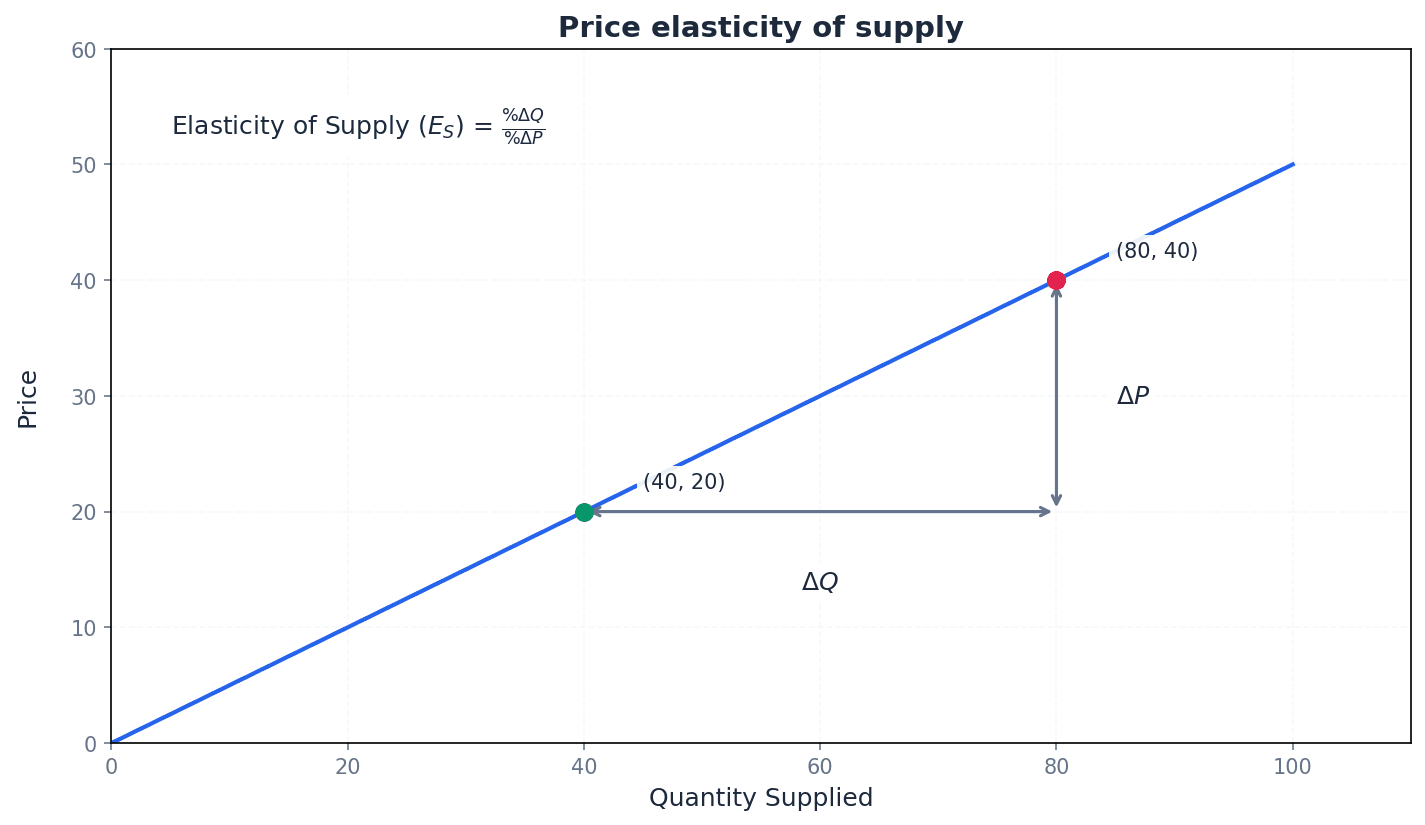

elasticity — Elasticity measures the responsiveness of one variable (such as quantity demanded for a product) after a change in another variable (such as the price of that product), ceteris paribus.

It is a coefficient that quantifies the extent of change. If a small change in price or income produces a bigger change in quantity demanded, the relationship is elastic; if a large change produces a small change, it is inelastic. Think of a rubber band: a very elastic band stretches a lot with a small pull, while an inelastic band barely stretches even with a strong pull. Similarly, elastic demand changes a lot with a small price change, inelastic demand changes little.

Students often think elasticity only refers to price, but it is actually a general concept measuring responsiveness between any two related economic variables.

When defining elasticity, ensure you mention 'responsiveness' and 'ceteris paribus' to achieve full marks. Be precise about which variables are changing.

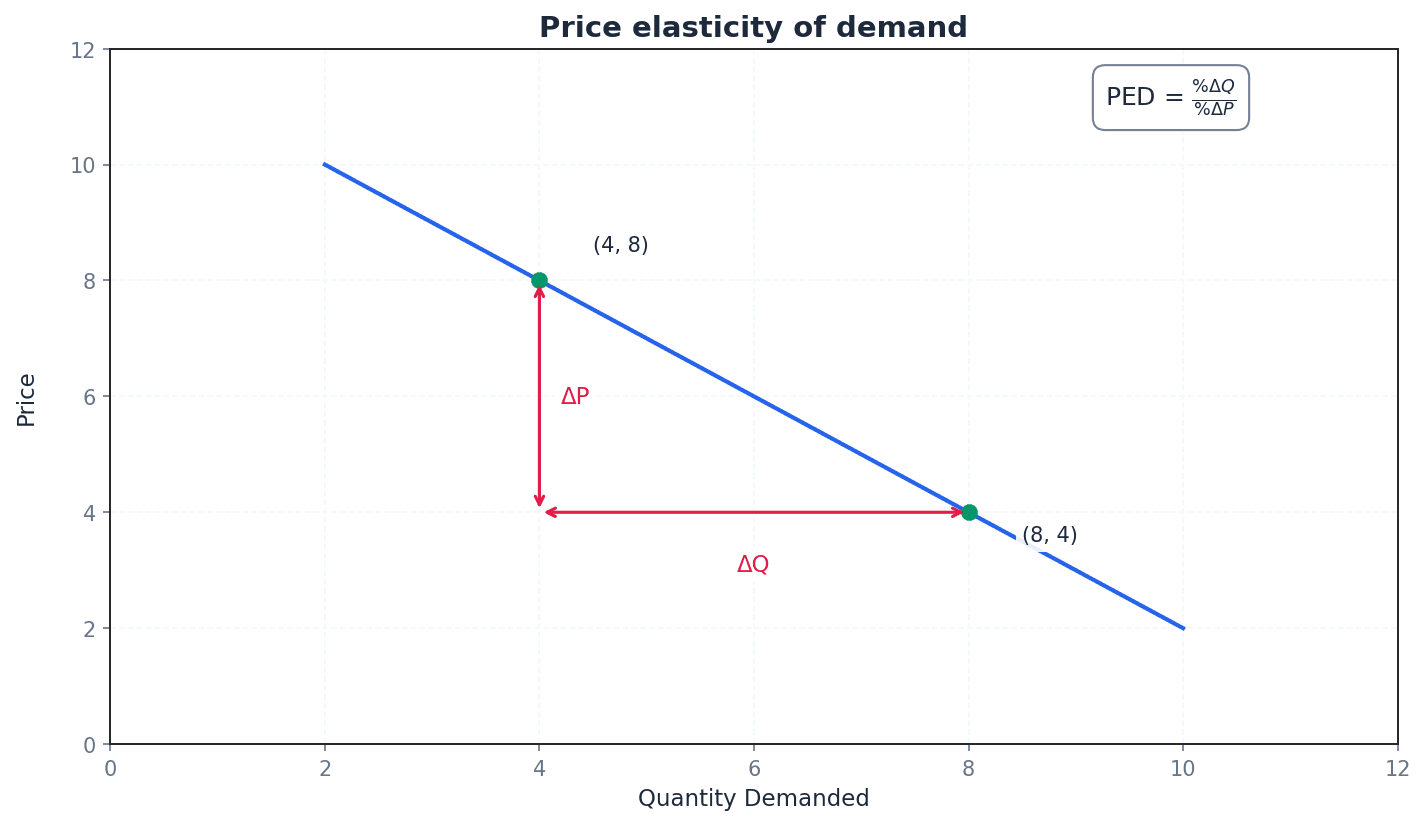

Price elasticity of demand (PED) — Price elasticity of demand (PED) measures the responsiveness of the quantity demanded for a product following a change in the price of the product.

It quantifies how much quantity demanded changes when the product's price changes, assuming all other factors remain constant. A high PED means demand is very sensitive to price changes, while a low PED means it's less sensitive. For example, if a shop raises the price of a common brand of bottled water (high PED), many people will switch to another brand or tap water. If they raise the price of a life-saving medicine (low PED), people will likely still buy it.

Price elasticity of demand (PED)

Used to measure the responsiveness of quantity demanded to a change in the product's own price. Economists usually ignore the negative sign.

Students often think PED is always negative, but economists usually refer to PED in absolute terms by ignoring the negative sign.

Always state the formula for PED and remember to interpret both the size (elastic/inelastic) and the sign (though often ignored for PED) of the coefficient in your analysis.

price inelastic — Demand is price inelastic when the numerical value of PED is less than 1, meaning the quantity demanded is unresponsive to price changes.

In this case, a percentage change in price leads to a smaller percentage change in quantity demanded. For firms, this means a price increase will lead to an increase in total revenue. Imagine needing petrol for your car; even if the price goes up significantly, you still need to buy it, so your demand doesn't change much. This is price inelastic.

Students often think 'inelastic' means no change at all, but it actually means a less than proportionate change.

When explaining price inelastic demand, clearly link it to the concept of total revenue: a price increase will raise total revenue, and a price decrease will lower it.

price elastic — Demand is price elastic when the numerical value of PED is greater than 1, meaning the quantity demanded is responsive to price changes.

Here, a percentage change in price leads to a larger percentage change in quantity demanded. For firms, this implies that a price increase will lead to a decrease in total revenue. For example, if a specific brand of chocolate bar increases its price, many consumers will easily switch to a cheaper alternative, showing elastic demand.

When analysing price elastic demand, ensure you explain the inverse relationship with total revenue: a price decrease will increase total revenue, and a price increase will decrease it.

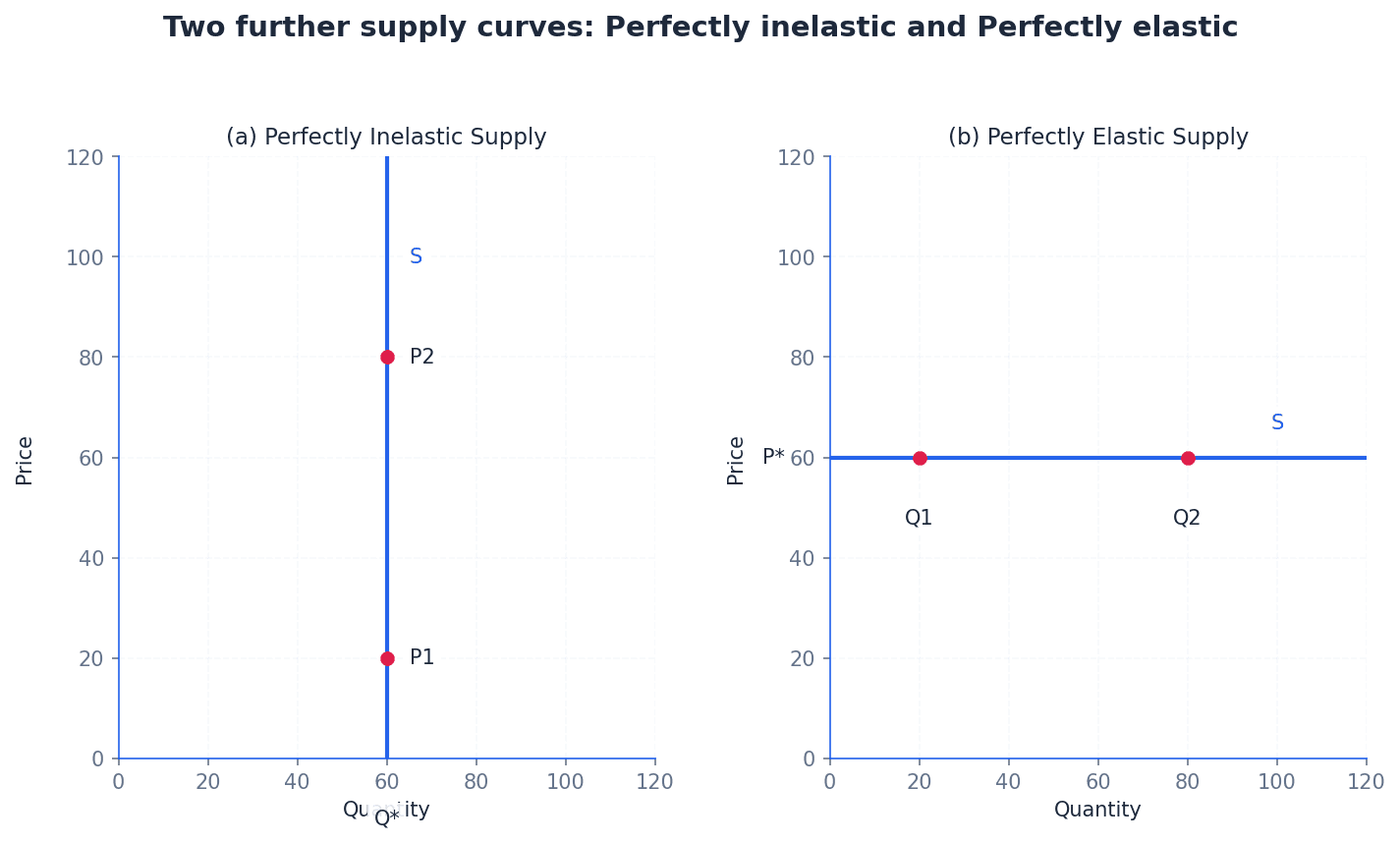

perfectly inelastic — Demand is perfectly inelastic when the PED is 0, meaning it is completely unresponsive to price changes.

Regardless of the price charged, consumers are willing and able to buy the exact same amount. This is represented by a vertical demand curve. A person needing a life-saving drug will buy the same quantity regardless of its price, as there are no substitutes and it's essential.

When drawing a perfectly inelastic demand curve, ensure it is a vertical line to accurately represent a PED of 0.

perfectly elastic — Demand is perfectly elastic when the PED is infinite (∞), meaning consumers will buy all that is available at a specific price, but none at a higher price.

Even a tiny increase in price causes quantity demanded to fall to zero, while a tiny decrease causes quantity demanded to become infinite. This is represented by a horizontal demand curve. In a perfectly competitive market, if a single farmer tries to sell wheat above the market price, they will sell nothing, as buyers can easily get identical wheat from other farmers at the market price.

When drawing a perfectly elastic demand curve, ensure it is a horizontal line to accurately represent an infinite PED.

unit elasticity — Demand has unit elasticity when the PED value is (-)1, meaning the percentage change in price is exactly matched by the percentage fall in quantity demanded.

In this scenario, total expenditure by consumers (and total revenue for firms) remains unchanged when the price changes. The demand curve is typically a rectangular hyperbola. If a 10% price increase leads to a 10% decrease in quantity demanded, the total amount of money spent remains the same, like balancing a seesaw perfectly.

For unit elasticity, remember that total revenue remains constant regardless of price changes. This is a key characteristic to mention in explanations.

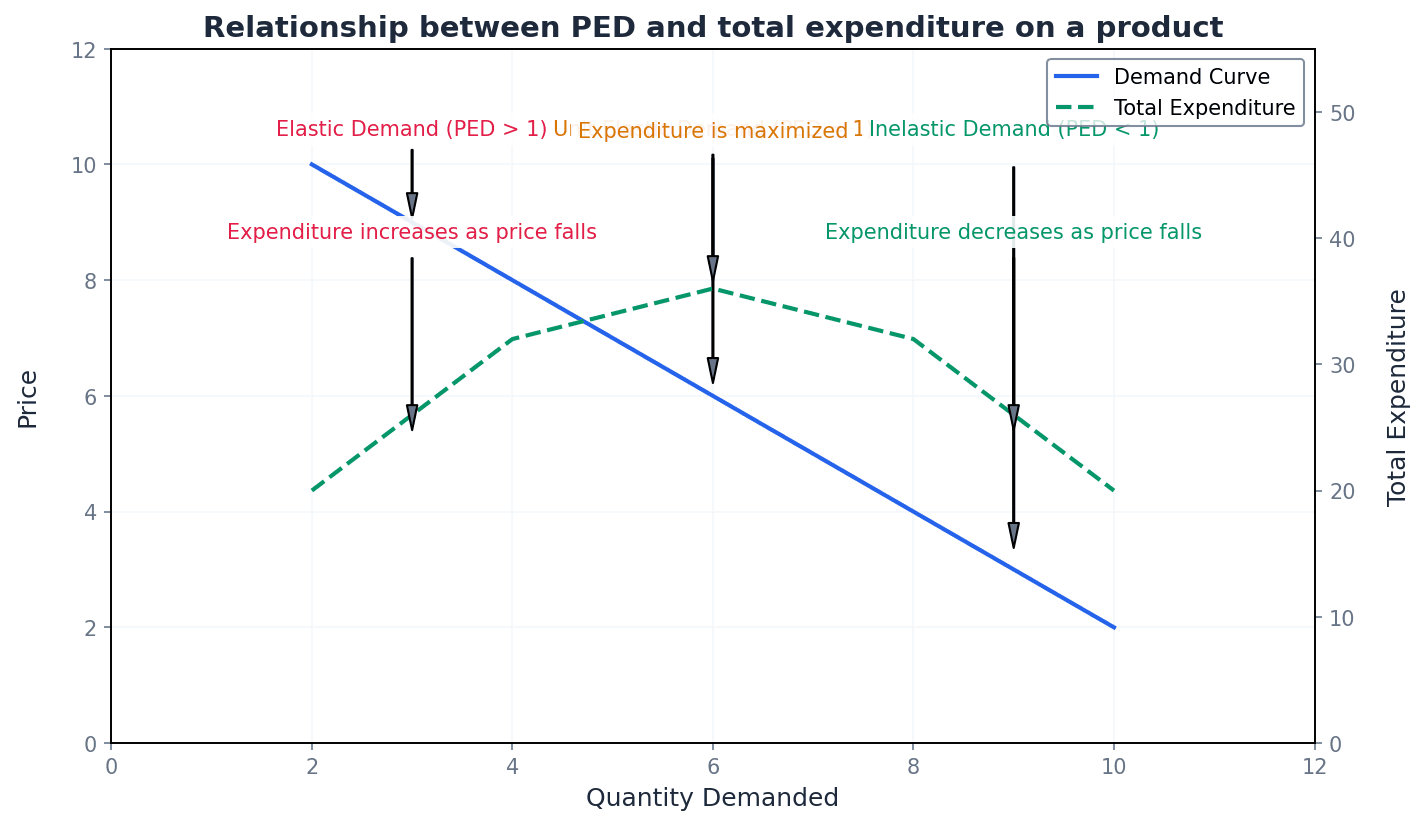

The relationship between Price Elasticity of Demand (PED) and total expenditure (or total revenue for firms) is crucial for decision-making. Total expenditure is calculated as Price (P) multiplied by Quantity (Q). If demand is price elastic (PED > 1), a price decrease will lead to a more than proportionate increase in quantity demanded, thus increasing total revenue. Conversely, a price increase will decrease total revenue. If demand is price inelastic (PED < 1), a price decrease will lead to a less than proportionate increase in quantity demanded, decreasing total revenue. A price increase will increase total revenue. When demand has unit elasticity (PED = 1), total revenue remains constant regardless of price changes.

Total expenditure / Total revenue

Represents the total amount of money consumers spend on a product, which is equal to the total revenue received by a firm.

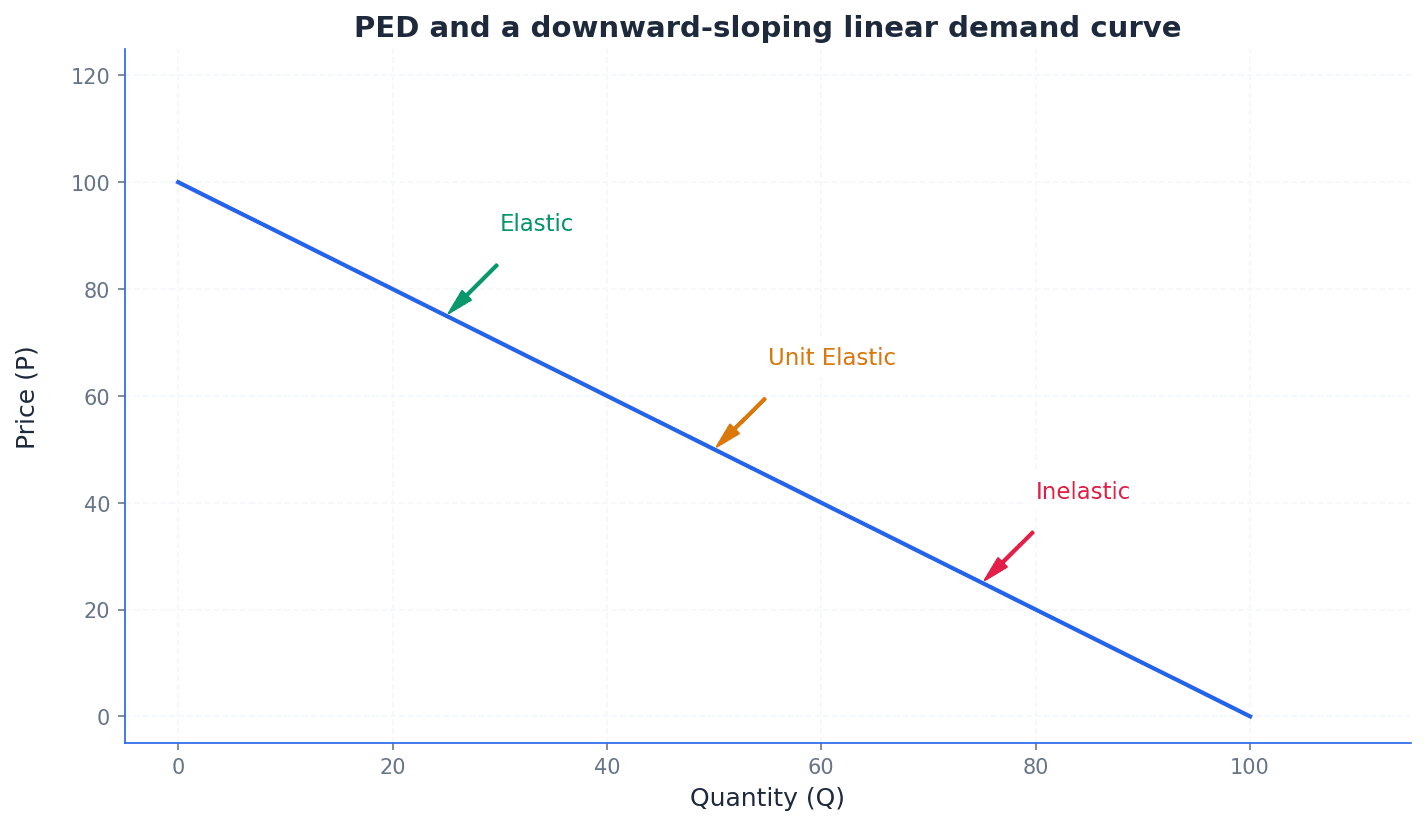

Even along a straight-line, downward-sloping demand curve, the price elasticity of demand is not constant. At higher prices and lower quantities, demand tends to be price elastic. As the price falls and quantity demanded increases, PED moves towards unit elasticity at the midpoint of the demand curve. At lower prices and higher quantities, demand becomes price inelastic. This variation is due to the relative percentage changes in price and quantity along the curve.

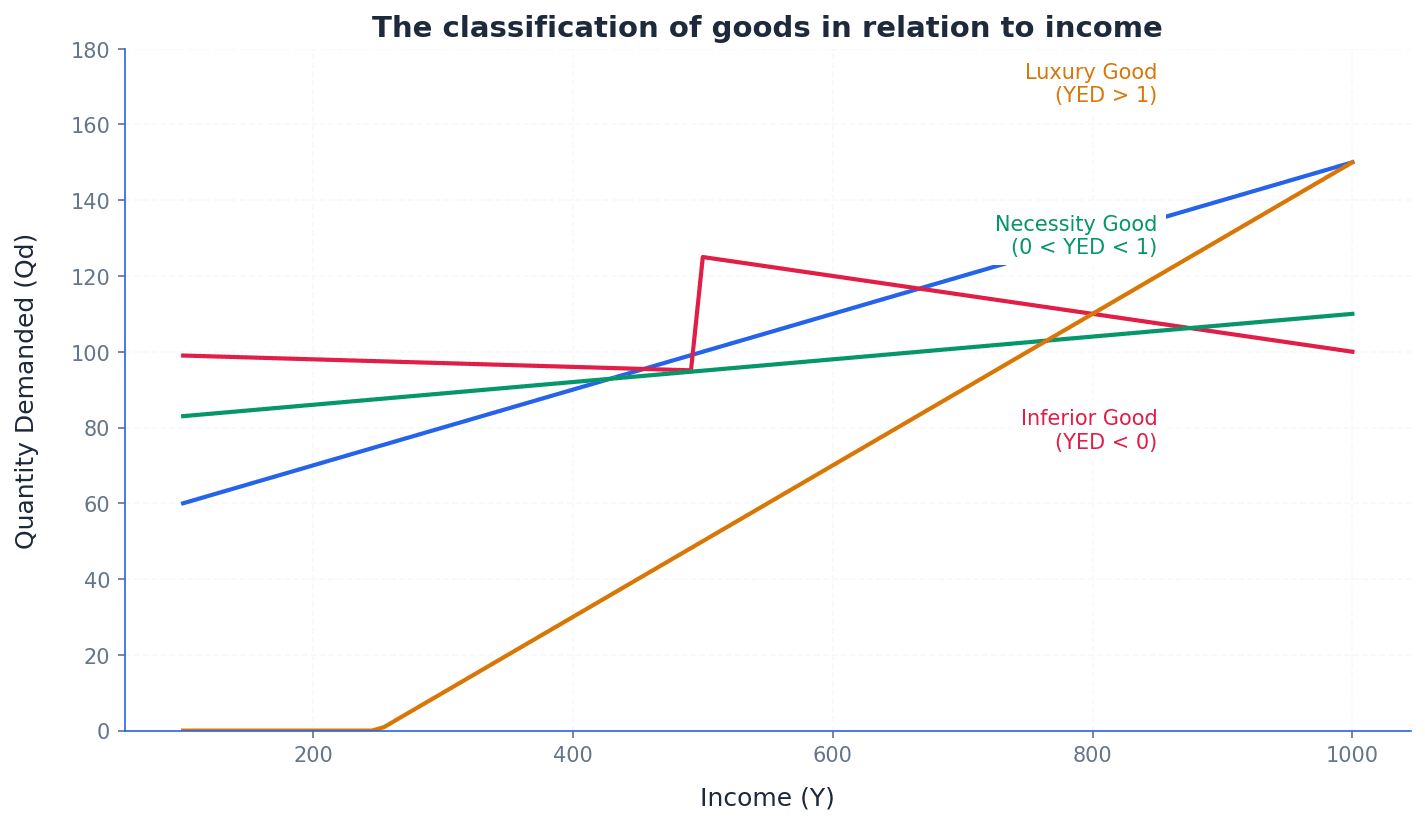

Income elasticity of demand (YED) — Income elasticity of demand (YED) measures the responsiveness of the quantity demanded for a product following a change in income.

It indicates how much the quantity demanded of a good changes when consumers' incomes change, assuming other factors are constant. The sign of YED is crucial for classifying goods. For example, if your income doubles, you might buy more restaurant meals (positive YED) but fewer instant noodles (negative YED).

Income elasticity of demand (YED)

Used to measure the responsiveness of quantity demanded to a change in consumer income. The sign (positive/negative) is important for classifying goods.

Students often forget to consider the sign of YED, but the sign (positive or negative) is essential for classifying goods as normal or inferior.

When discussing YED, always refer to both the size (elastic/inelastic) and the sign (positive/negative) of the coefficient to fully classify the good.

normal good — A normal good is one where the quantity demanded increases as income increases, and its YED is positive and expected to be between 0 and 1.

Most products fall into this category, meaning that as people get richer, they tend to buy more of these goods. Examples include chicken meat in emerging economies or smartphones. As you earn more money, you might buy more clothes or go out to eat more often; these are normal goods.

Students often assume all normal goods have a YED greater than 1, but normal goods can have YED between 0 and 1 (necessities) or greater than 1 (luxuries).

inferior good — An inferior good is one where the quantity demanded decreases as income increases or increases as income falls, and its YED is negative.

Consumers tend to replace inferior goods with better quality substitutes as their income rises. Examples include poor quality rice or packet noodles. When you get a better job, you might stop buying cheap instant coffee and switch to a more expensive, higher-quality brand. The instant coffee is the inferior good.

When identifying inferior goods, explicitly state that the YED is negative and explain the inverse relationship between income and quantity demanded.

Students often think 'inferior' means bad quality, but it actually refers to how demand for the good changes with income, not necessarily its inherent quality.

necessity good — A necessity good is a type of normal good for which the quantity demanded is unlikely to change significantly when income changes, having a positive YED close to zero.

These are staple foodstuffs or essential items that households purchase regularly, and there's a limit to how much more they will buy even with substantial income increases. Examples include rice, flour, and pulses. Even if your income doubles, you won't suddenly buy ten times more bread or milk; you'll still buy roughly the same amount because you only need so much.

Students often confuse necessity goods with inferior goods, but necessity goods have a positive YED (though close to zero), while inferior goods have a negative YED.